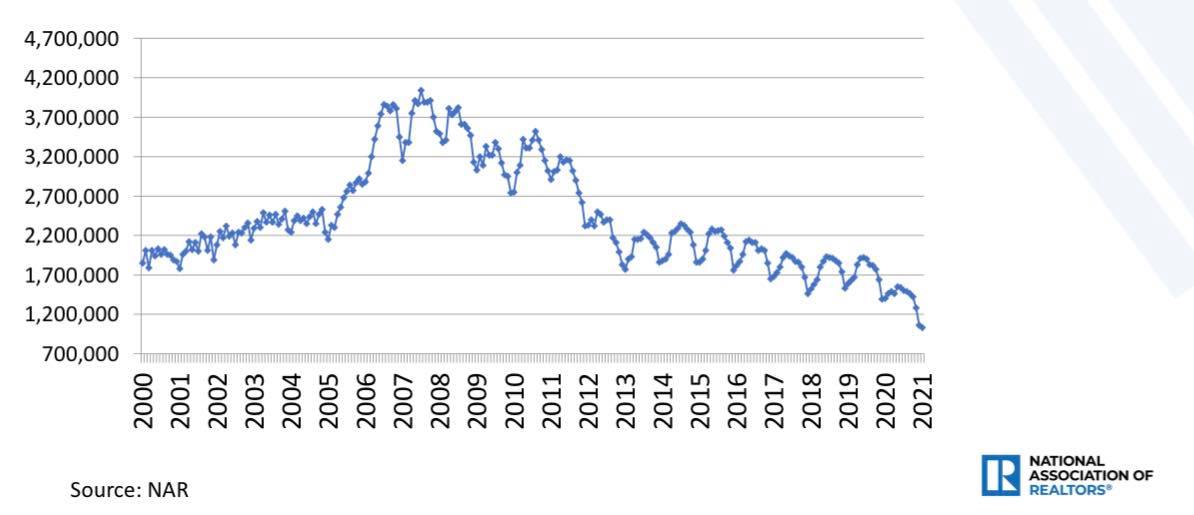

My biggest concern for housing in the years 2020-2024 was that if the demographic push in demand picks up and total home sales get over 6.2 million, we could be at risk of housing inventory falling to such low levels that I would have to categorize this housing market as unhealthy. 2020 and 2021 easily each have over 6.2 million new and existing home sales combined.

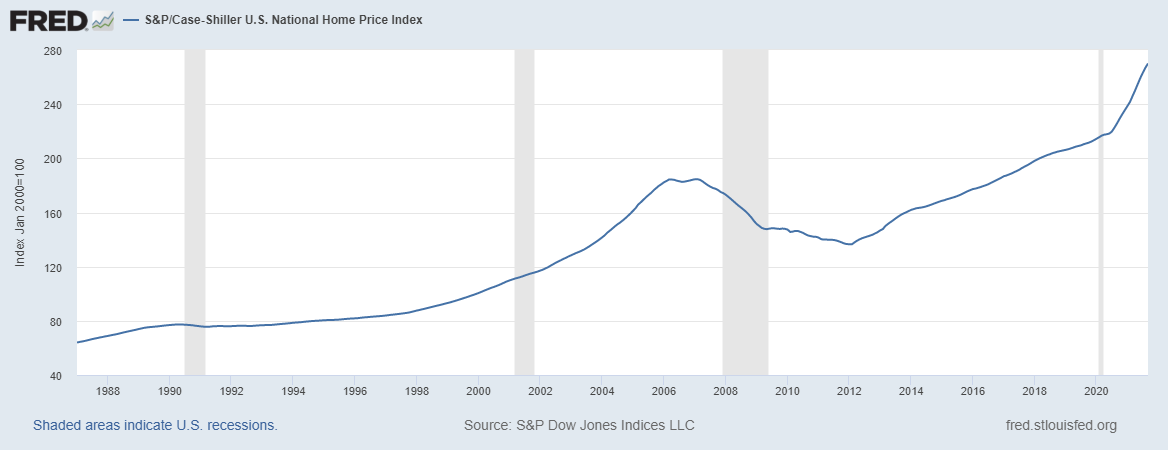

This type of sales growth — which couldn’t happen from 2008-2019, as I have often stated — is coming with a hefty price tag. We can see that inventory falling to such low levels has created unhealthy home-price growth in both 2020 and 2021. While the rate of growth of home prices is cooling off (the S&P CoreLogic Case-Shiller Home Price Index typically lags), it’s still at a very unhealthy level for me. This is all about housing inventory collapsing to all-time lows in 2020-2021.

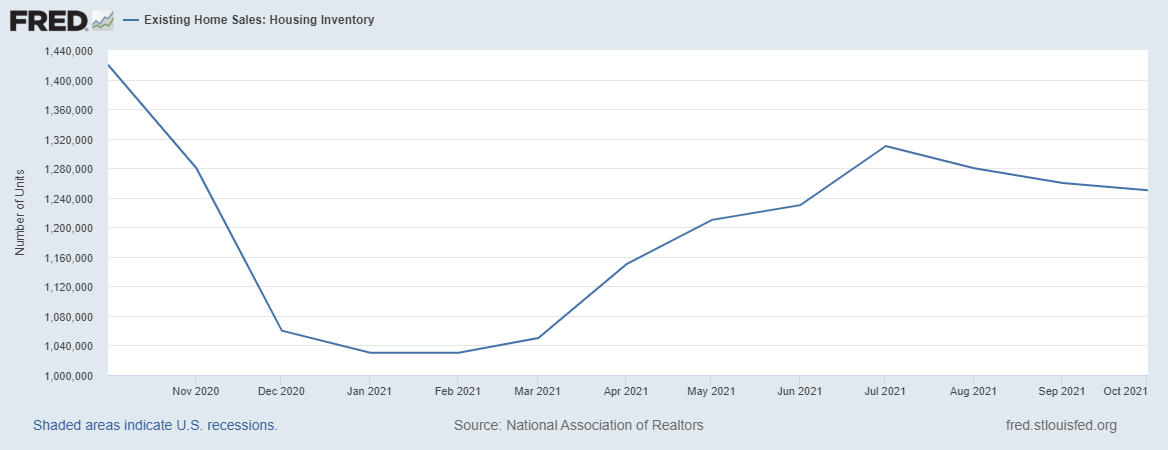

While I didn’t believe we could start 2022 at a new all-time low for housing inventory, this can’t be ruled out any longer. I honestly believed this would not be the case in 2022, but I am getting nervous. A few months ago, I wrote that falling inventory was one of the biggest risks to the housing market.

The seasonality of inventory has always been very evident, especially after 2014. Inventory fades in the fall and winter and picks up in summer and spring. Since 2014, inventory levels have fallen while purchase application data has risen. Not even 5% mortgage rates in 2018 budged this data line too much. Going into 2021, it didn’t look great for the inventory levels, and we paid the price with highly unhealthy home-price growth as demand was simply too strong.

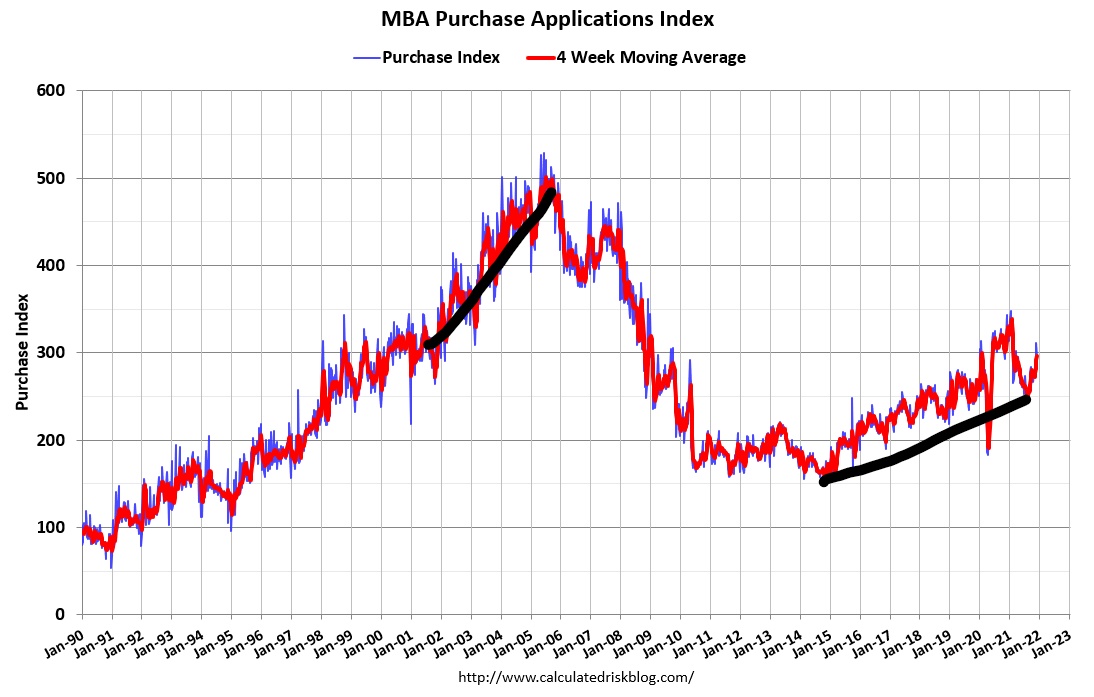

As I have recently noted in a previous article, while everyone focused on iBuyers, who don’t even make up 1% of total home sales, the MBA purchase application data has had a nice run for the last 13 weeks. The year-over-year data has shown double-digit better trends while still being negative year over year. This explains the better existing and pending home sales data as this data line looks out 30-90 days.

A lot of housing bears didn’t make COVID-19 adjustments to the purchase application data and truly believed housing was crashing because of the negative year-over-year data trends. This was a terrible rookie mistake and if you know anyone who was pushing this, my best advice is to run away from that hot mess.

In the midst of seasonality factors and as demand has picked up, I can say that 2021 has outperformed my expectations. Now we must consider the possibility that total housing inventory levels might start from a fresh all-time low going into spring of 2022. The next few existing home sales reports will be critical as we are in the period when inventory really falls due to seasonality. I had been hoping that this wouldn’t be the case, that inventory couldn’t break to new all-time lows. While we have solid and stable demand, we aren’t experiencing the credit boom action from 2002-2005. However, it is good enough to drive inventory lower again, and we need to rethink this problem. So, let’s bring some reality into this discussion.

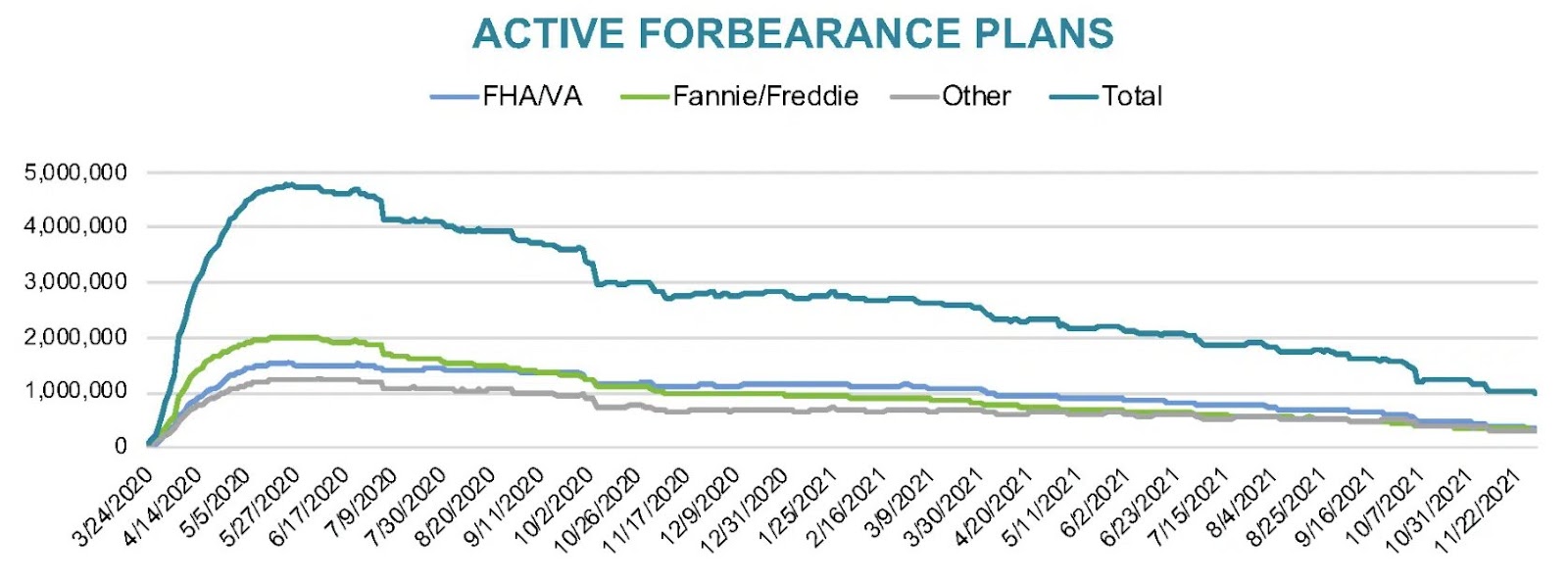

Forbearance hasn’t supplied the market with a vast amount of inventory.

One thing has been very evident in 2021: The premise that forbearance was going to crash the housing market has been just as flawed as the people that assumed COVID-19 was going to hit housing in 2020. Those of you who have followed my work on HousingWire know that I created the term forbearance crash bros in 2020 because the professional grifting of doomsday housing calls went into overdrive that year. Once they realized their dream of housing was not collapsing, they moved the goal post to 2021. They have moved the goal post so much over the last 10 years that it’s not even in the stadium anymore, which is why I call this idea “the lost decade.”

Getting ahead of this flawed premise, I wrote a series of articles that point out that this isn’t the credit bubble of 2002-2005, and the loans post-2010 were good. So, naturally, when the jobs came, people would get off forbearance independently.

We have gone from near 5 million loans in forbearance to finally breaking under 1 million recently. In one of the most significant economic victories against the radical bearish American crew, this was just beautiful to watch the people of this country come out on top.

From Black Knight:

Now, this doesn’t mean everyone gets off the forbearance program. We have had people on forbearance already sell their homes and move onto the next stage of their life in a new home. However, the fears of 10 million to 15 million homes going into forbearance and the concerns of an economic depression due to COVID-19 were wildly overblown in March and April 2020. America came back strong, and we left this crew in the dust.

Still, I believe we will see more inventory come onto the market as we are winding down the last 994,000 loans in forbearance. Will it be enough to prevent housing inventory from getting to new all-time lows? Only time will tell over the next few months. I am still in the camp that we won’t break to all-time lows, but my premise is being challenged with the recent pick-up in demand.

Higher mortgage rates haven’t materialized as expected

Back in the summer of 2020, I believed that if mortgage rates could get over 3.75%, the days on the market would grow, which I think even to this day would be the most welcome healthy event for housing. For this unique five-year period in housing, I believed as long as the cumulative price growth was just 23% on a nominal basis, we would be OK, and housing affordability wouldn’t get hit too hard since wages are constantly growing each year.

Well, If home prices end 2021 with 13% total growth, this means my five-year growth model has been reached in just two years. My concern for 2021 was very noticeable in many interviews early in the year because my 10-year yield forecast peaks at 1.94%, which means mortgage rates at best can only reach 3.375% – 3.625%. Higher rates would create more days on the market, which I would love to see. However, it’s not happening.

Even with the hottest economic and inflation rate of growth in decades, the 10-year yield hasn’t been close to even testing my high-level range, and I am not in the camp that rates are a sure lock to go higher in 2022. Can you feel the stress? I am now thinking about lower rates and starting 2022 with all-time lows in housing inventory.

Panic selling Is a marketing gimmick

As I have said many times, the housing crash bears are simply very good professional grifters: the amount of bull they have produced for 10 years is worthy of legendary status. Recently, I have noticed a few people bring up the notion of panic selling.

This idea is that American citizens who are financially sound, have great cash flow, a vast amount of nested equity built-in, and live in a nice home will all of a sudden sell their homes at a major discount to the market bid in an attempt to get out at any cost. Really? I mean if they didn’t do that during the first two months of COVID-19, you think in a booming economy with rates under 4% that this is a possibility?

Part of the major problem with housing is that American households who own homes are in great financial shape. They have a fixed low debt cost and their wages have been rising for many years.

Their cash flow is so great that their FICO score is off the charts. Remember that housing tenure from 1985-2007 was running at five years and then from 2008-2021 it’s well over 10 years. So the American homeowner is in much better shape than anyone gives them credit for. You can clearly see why I am worried about housing inventory levels during the years 2020-2024 as demand has picked up so much.

Recently, I wrote an article saying Americans’ mortgage debt is great again. This is also a downside to the housing inventory story as forced selling or the notion that these Americans are panic stock traders getting a margin call at 12:05 PM so they need to sell at any price is just silly. Panic selling is different than distress selling when you’re in a foreclosure or short sale. Knowing the difference is the key.

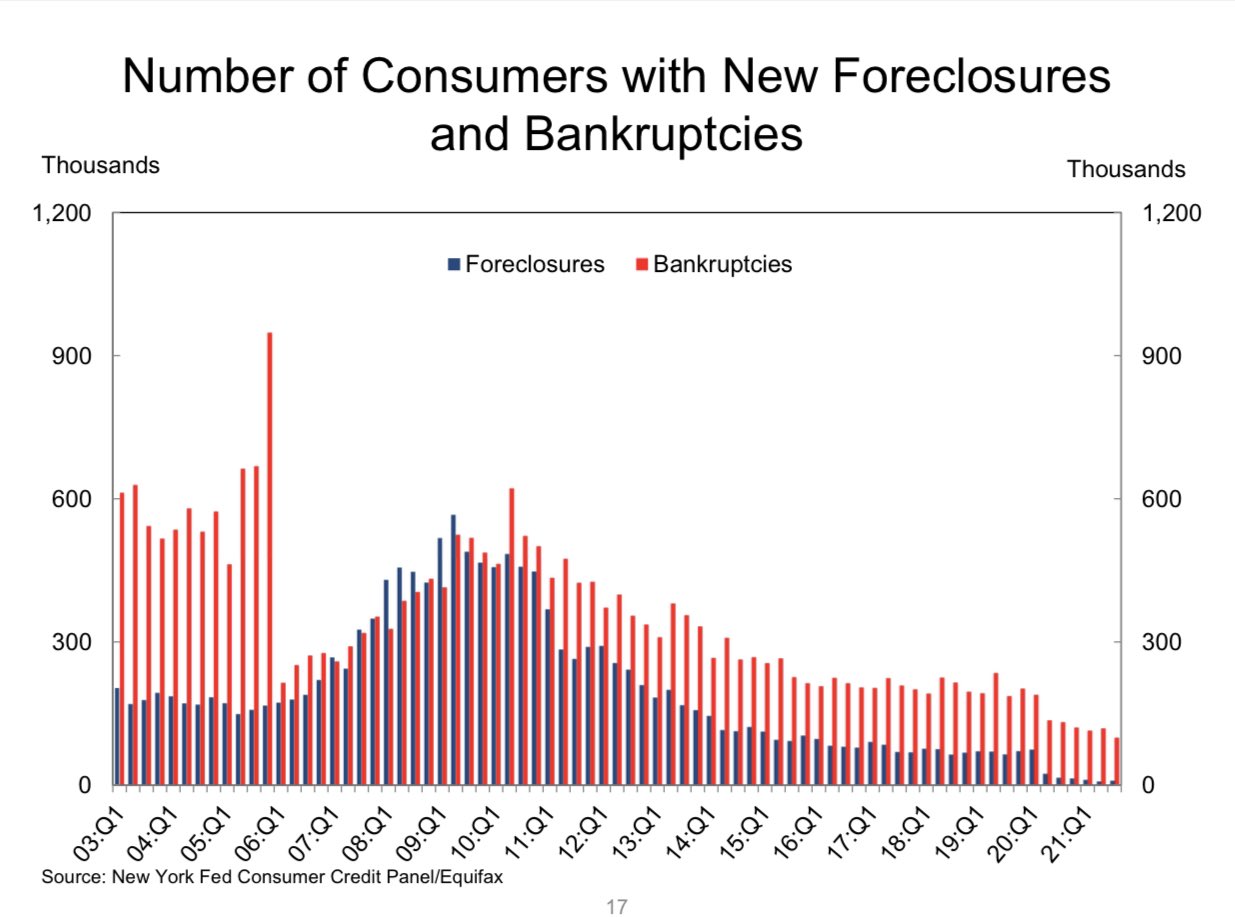

As you can see below, foreclosures and bankruptcy were rising into the 2008 recession from 2005-2008, then the great financial recession occurred.

With only a few months left before the spring selling season, it’s critical to keep an eye out on total inventory levels. The seasonality impact is currently in full force, but we can only hope it doesn’t break to all-time lows before the reversal of seasonality happens in 2022 and inventory increases again.

I am hoping and rooting for inventory levels to break above 1.52 million at some point — that has been my target level for some time to break away from this unhealthy housing market and create more balance. Historically speaking, that is a low total housing inventory level, however, total inventory between 1.52 million and 1.93 million will make this a B&B housing market: boring and balanced. However, as you can see, it’s not looking great currently and the clock is ticking for spring 2022.

Understanding all this pertinent and valuable info and analysis is crucial. However, I don’t see the Fed raising rates very much because every 1/4 pt increase raises our interest payments 75 billion per month. How can the U.S. sustain itself? It really can’t and I believe the game is over and we are in checkmate on the precipe of a failing currency and that is why Bitcoin on other cryptocurrencies will cause a change in our monetary system as a way to save one’s wealth as a hedge against our inflationary environment and the crazy devaluation of the dollar. At 0% interest rates, the Fed can’t do what the EU is doing where you are paying back 1.5% less than you borrow. The writing is on the wall and my fear is for so many that are in cash and not in hard assets, real estate, crypto, certain stocks, etc. There is real underlying fear out there and China is at our doorstep as I believe there in a neck and neck race or probably already kicking us in the ass. The average life expectancy of an Empire is roughly 250 yrs and we have 4.5 years left to somehow figure out what to do to get the U.S. on a more stable financial trajectory. Two answers are to get back on a Gold Standard to keep the Fed from continuing their crazy and insane printing of dollars backed by nothing and also to force reduced spending as much as possible, especially Military and wherever else so they don’t have to increase income taxes to keep paying for their willy-nilly free for all spending without any checks and balances. You can’t continue spending more than you take in as a basic concept of business and the government isn’t following any business-based logic as common sense is no longer common and more important, critical thinking is no longer critical!