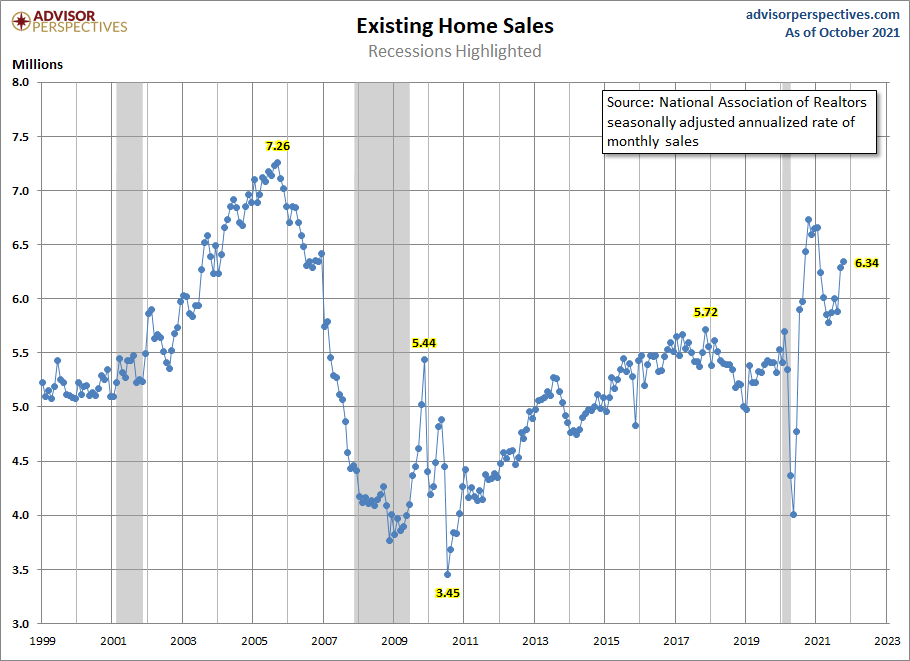

The National Association of Realtors‘ existing home sales report for October came in at a solid beat of estimates at 6.34 million. This number is above my trend sales peak of 6.2 million and that means we have had back-to-back existing home sales prints of over 6.2 million. Early in the year, I had discussed that if existing home sales stay in a range between 5.84 million and 6.2 million, that would mean it’s a good year for housing demand.

A big part of my work since the end of 2020 is explaining to people that housing data was going to moderate because the make-up demand from COVID created a surge in sales that is very abnormal. This meant that I had anticipated home sales to fall to a more reasonable range. However, the key was to not overreact to that moderation and say that housing was crashing. This was very common in the previous expansion when any weaker data line trend was interpreted by some people as a housing crash.

As I wrote in my blog in 2020: “The rule of thumb I am using for 2021 is that existing home sales if they’re doing good, should be trending between 5,840,000-6,200,000. This, to me, would be considered a good year for housing.”

I had anticipated a few prints under 5.84 million and so far we have only gotten one print this year below that level. This means with only two more reports left so far in 2021 every single existing home sales print has been higher than the total closing level of 5.64 million in 2020. Not bad considering the low inventory and all that unhealthy home price growth we have seen since the start of 2020.

If home sales moderate from these levels, that would be perfectly normal to me because clearly now the existing home sales market is outperforming my expectations with these last two sale prints. So much for the 2021 forbearance crash bros — the second half of 2021 housing crash YouTube fanatics. Mother demographics and low mortgage rates can crush a lot of American bear’s hearts as they did in 2020 and 2021.

The main reason why housing has done better in the years 2020 and 2021 is that we just got a boost in demand from the most significant housing demographic patch ever in history, as ages 27-33 are the biggest group ever. Then when you add move-up, move-down, cash, and investor buyers together, we should be able to always have total home sales — both new and existing — at 6.2 million or higher. This is something that couldn’t happen in the years 2008-2019. We are well above my 6.2 million total sales numbers and that means both years have been a noticeable beat in my eyes.

For every positive, there is a risk of a negative and we have seen that risk play out in home-price growth. My single biggest concern for the years 2020-2024 was that home-price growth could overheat and we have seen that take place, which is why I keep on saying this is the most unhealthy housing market post-2010. Not because of a credit housing bubble boom but because days on market are still too low, creating a bidding war frenzy that doesn’t do anyone any good.

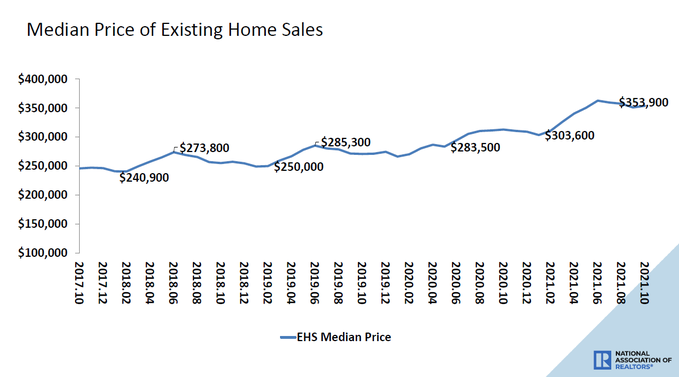

From NAR: The median existing-home price for all housing types in October was $353,900, up 13.1% from October 2020 ($313,000), as prices climbed in each region.

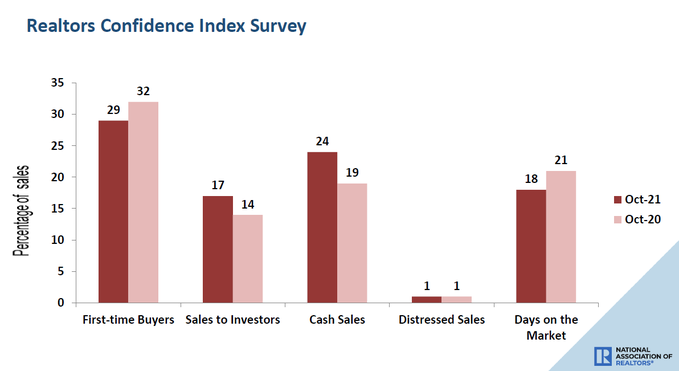

One data set I like to keep an eye on regarding progress for what I want to see in the B&B housing market (boring and balanced) is for days on market to grow. Now we have some good news, the days on market grew one day from the last month’s report, from 17 to 18 days. I know it might not sound like much, but still, progress is progress. I would love to see days on market get to 30 days, so we still have a ways to go for that to happen.

NAR: In October, first-time buyers were responsible for 29% of sales; Individual investors purchased 17% of homes; All-cash sales accounted for 24% of transactions; Distressed sales represented less than 1% of sales; Properties typically remained on the market for 18 days.

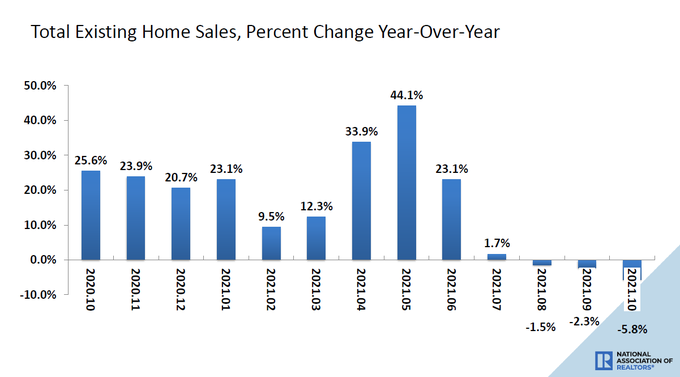

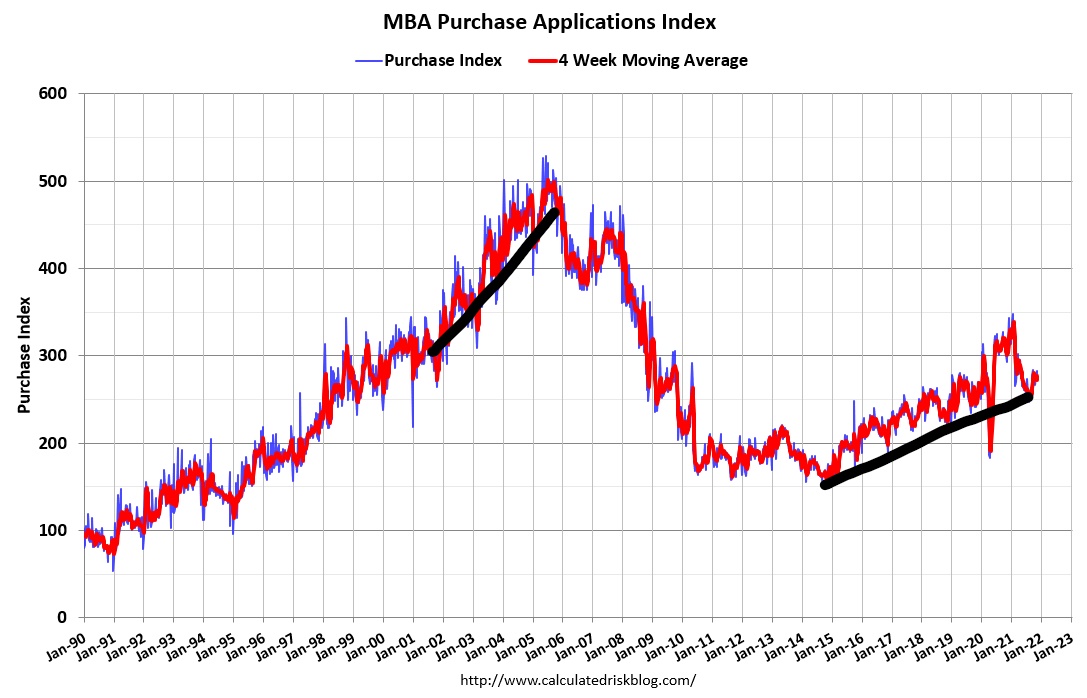

Another theme of mine earlier this year was to expect negative year-over-year data in the MBA purchase applications in the second half of 2021. This is only due to the high comps that we had in the second half of 2020 — all due to the make-up demand from COVID-19. I saw a lot of rookie housing bears try to push this as a reason for housing to fall hard in the second half of 2021. This is a terrible rookie mistake made by people who lack the experience of tracking housing data properly. So, the negative year-over-year data in home sales should not be a shock anymore.

NAR: Sales fell 5.8% from a year ago (6.73 million in October 2020).

There has been a lot of hype that this entire housing market is driven by investors. Dear lord, this Micky Mouse act happens often, but the real driver of housing is mortgage buyers. When mortgage buyers fade — and they will at some point if mortgage rates go higher — so will home sales. We don’t have a Wall Street moat around housing. The MBA purchase application data had been firming up since 11 weeks ago and nobody really cared to notice.

It’s sexier to say that investors are driving home prices higher instead of all those pesky mortgage buyers, which is by far the biggest portion of housing demand. It just doesn’t sell well to say that millennial mortgage buyers are driving home prices to all-time highs. Yellow journalism, gloom-and-doom clickbait sites, and ideological extreme left and right-wing takes get a lot of play, but that doesn’t mean they are right.

Since the summer of 2020, I had have said housing will slow but it needs mortgage rates above 3.75%, which means the 10-year yield has to get over 1.94%. My 2021 forecast didn’t have that reality in play. In fact, the AB recovery model range of 1.33%-1.60% held its ground for a portion of 2021. Everything remarkably looks right with the bond market for me. As I write this article, the 10-year yield is at 1.60%. Priceless, isn’t it?

For the rest of the year, I am really watching one thing: I would love to see inventory hold up better than it did last winter. I do not want to see Inventory collapse like it did last year and start the spring of 2022 at those levels. So, that is my focus for the last two reports and the weekly tracking of inventory.

All in all, I would say existing home sales, for now, are outperforming and if sales levels hold above 6.2 million I will be very impressed. If sales trends come down a bit in the next few months, that would fall in line with my sales trend levels. However, the main story for 2021 is that home sales demand is going to end higher than it did in 2020 led by American mortgage home buyers.

I have a question for Logan. I am a new home builder and although I like to see the statistics of “active listings” as an indication of inventory, I always feel that to a very large extent, this is not really inventory, but rather a slice of the “housing stock” where buyers want to move to another home.

Now assuming that most of the Buyers are not moving out of state, and for that matter, since this is a national statistic, I would expand that assumption to assume they are not moving out of the country. If that is the case, then the active listing and existing home sales are really just existing buyers trading places. I call that a zero sum game of housing. People rarely are selling their home and moving in with someone else. That may be interesting during a downturn, but today, that would not be the case.

What’s really more important is the additions to the housing stock vis a vis New Permits or new home starts against the increase in new jobs. ie. permit to employment ratio. I am assuming that all of the existing homes are fairly occupied. In fact the vacancy of housing has been about the same number for over 30 to 40 years. Therefore, the important number is the absorption of new homes into the market.

New homes versus new Buyers. New Buyers will be anyone “undoubling” ie divorces, people moving out of someone’s home or basement, and new Buyers entering the market from say entering the workforce.

Therefore, I don’t get too excited about Existing Home Sales, since all that tells you is whether the brokers are making commissions. It’s just a measurement of velocity in the market. I don’t think it tells enough for as much press it receives. Its simply the churn rate of the existing housing stock.

Jay B Scolnick

Premier Community Homes, Ltd.

New home sales matter more to the economy because of construction jobs, big-ticket items purchases. In contrast, the existing home sales market is more of transfer of commissions, moving trucks, and remodeling projects.

The extreme housing bears in America only care about existing home prices and believe that if home prices collapse, so will the United States of America. Their trolling of America since 2012 is predicated on the fact that nominal home prices increasing is some deviate action by the federal reserve and that American’s buying homes to live in is an absurd premise. These are primarily anti central bank fanatics or the Housing Bubble Boys 2.0 crew since 2012.

Regarding total inventory levels, 1 250,000 existing homes are on the market currently. However, the new home sales market is an entirely different beast altogether.

This last article on housing starts will give you more perspective on why I always like to separate these two housing sectors. I would label the new home sales sector as just ok currently.

https://www.housingwire.com/articles/housing-permits-reflect-rising-builder-confidence/

Also, this article will give you an idea of when I believe the housing sector will tell you that things are getting weaker to go along with economic weakness

https://www.housingwire.com/articles/when-will-we-see-the-next-housing-recession/

Thank you for the very insightful article Logan! When discussing mortgage rates could you please briefly discuss the difference between the 10 Year Treasury Yield in comparison to the Mortgage Bond Market? I hear a lot of talk about the Mortgage Bond markets impact on mortgage rates and the Fed’s decision to start tapering their bond purchases in that market, and would like to try and understand the difference a little better than I currently do. Thank you.

Scott, historically the 10-year yield and 30-year fix mortgage rate has had a solid correlation. In 2020 pricing for mortgages wasn’t fluid with the Mortgage Market Meltdown that started on March 9th. However, historically mortgage rates trend with the 10-year yield, on your question about the Fed tapering and rates. Many people believe that when QE ends, mortgage rates have to rise, or when tapering happens, that should occur. Using the previous expansion as an example, that is an invalided theory as bond yields have gone lower with QE ends, and even when some tapering happens, rates have gone down in the past. So to address your question with details, these two articles can give you more insights with charts. Just know that mortgage rates really can’t rise too much if the 10-year yield doesn’t go higher.

These articles I wrote for HousingWire will address some of your questions in detail with charts.

https://www.housingwire.com/articles/when-will-mortgage-rates-get-over-4/

https://www.housingwire.com/articles/for-housing-look-at-bonds-over-mbs-or-federal-debt/