This is the first time I am writing about mortgage backed securities (MBS) because I hardly ever consider this aspect of the housing market in my work. But since now even Federal Reserve members are discussing the pros and cons of MBS, this is a good time to give you my take.

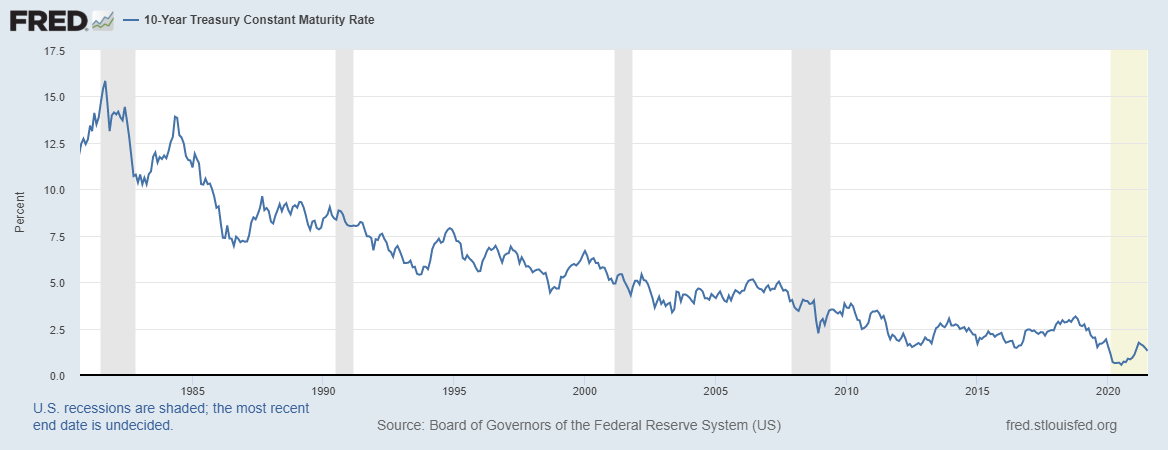

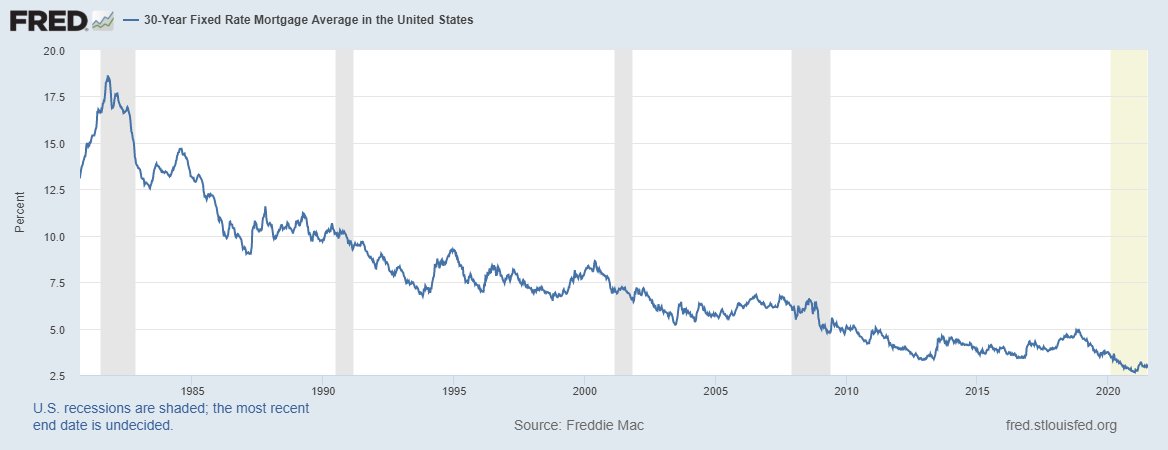

The 10-year yield has been in a downtrend since 1981, and so have mortgage rates, so the MBS market hasn’t ever been a focus of mine. Recently though, I have been reading a lot of speculation that when quantitative easing ends, the U.S. housing market will be in trouble because mortgage rates will skyrocket and cause a crash in sales and prices that would amount to the second coming of the housing bubble.

It is an easy argument to make that during the pandemic, the purchase of MBS by the Federal Reserve was needed to bolster the economy. Today, however, when inflation seems a larger negative talking point than economic sluggishness, it makes less sense that the Federal Reserve is still buying MBS.

However, why hasn’t the bond market blown up higher with solid economic growth, a whisper of when tapering will happen, and hotter than normal trend inflation.

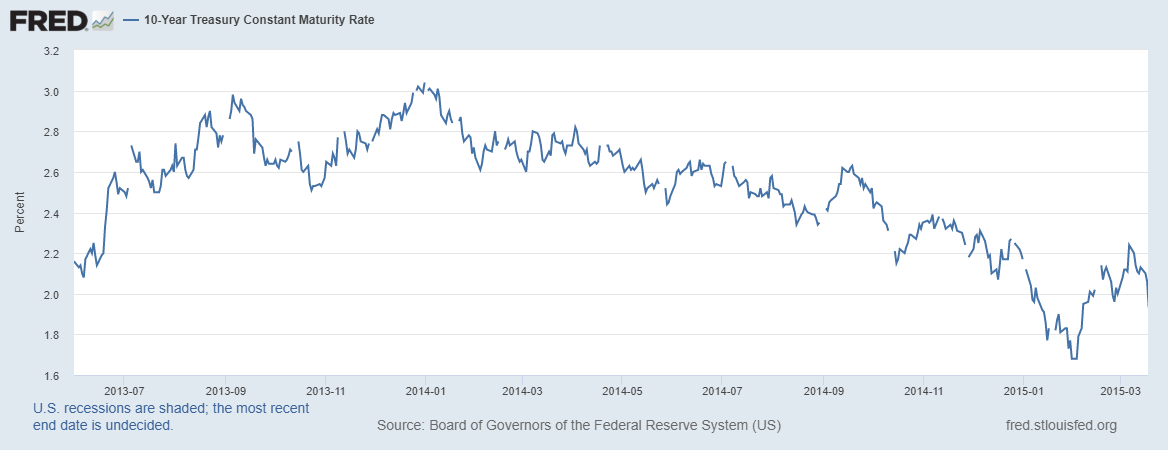

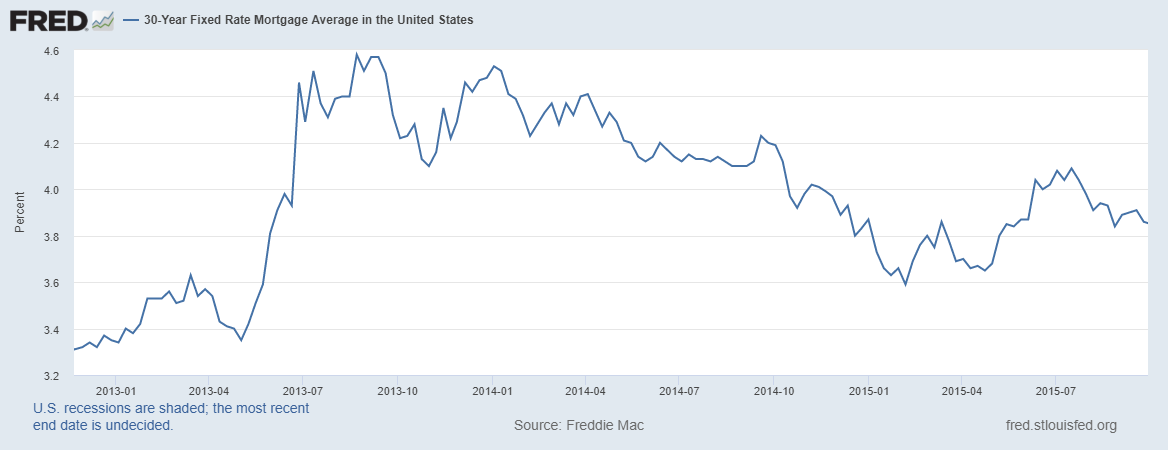

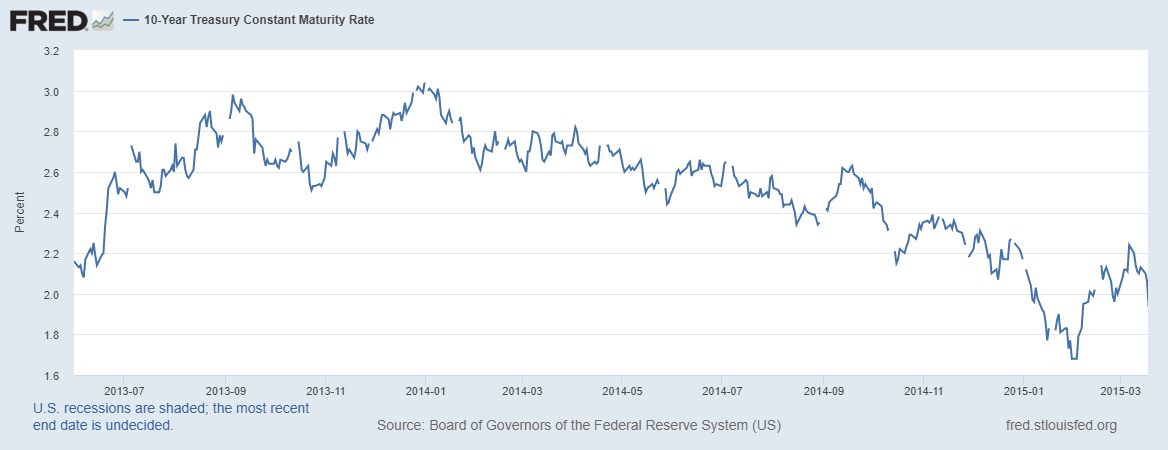

We need only look as far back as 2014 for a precedent on how mortgage rates responded to tapering. When QE 3 came to an end in 2014 and the Federal Reserve started to curtail their purchasing, bond yields fell with mortgage rates. Bond yields fell when QE 2 ended as well. The downtrend in yields with tapering has been consistent and long-standing. In fact, it was only in 2018 when the 10-year yield got above 3% again, to once again fall to below 2% the next year.

It is true that mortgage rates were higher during our COVID-19 crisis than they should have been due to the mortgage market meltdown during this crisis. Before COVID-19 hit our shores, I wrote that if the U.S. were to go into a recession, bond yields would be in a range of -0.21% to 0.62%. I said that if bond yields were to go higher than 0.62%, then that would be a sign that the economy would be in recovery. In a stable, growing economy we should strive for the 10-year yield to be in a range of 1.33% to 1.60%.

This was the core basis of the America Is Back economic model I wrote back in April 7, 2020. “The fact that the 10-year yield is at 0.73% while I am writing this tells me that the markets believe that Q3 and Q4 will be better than Q2, which is using the lowest bar in recent history to work from. An early indicator of recovery would see the 10-year yield above 1% — especially if it got above 1.33%. A range between 1.33% and 1.6% on the 10-year yield is something we should be rooting for, especially if this happens without liquidation selling of bonds.”

This range was not something I pulled out of my hat in magic class; it was based on our economic history with respect to the four-decade downtrend in rates.

I am totally sympathetic with people who are confused on why the 10-year yield is so low with our economic growth and higher inflation data. I really am. However, this downtrend since 1981 on the bond market is some real powerful stuff folks and there is a healthy appetite for our bond market always.

I knew that this downtrend would be sustained in 2021 and that is why my forecast for bond yields for this year was between 0.62% to 1.94%, even though I was probably the most bullish person on the U.S. economy in 2020 going into 2021. In fact, I even retired my America is back economic model on December 9, 2020.

Low bond yields, and thus low mortgage rates, are contributing to what I have been calling the unhealthiest housing market post-2008. Low mortgage rates, plus strong housing demographics, plus low inventory means unhealthy price growth.

I have been writing about my concern regarding home-price growth for a while now. From my perspective, home prices hinge on two things, the bond market first, (i.e. mortgage rates), then the economics of housing driven by demographics.

I have written in the past that the housing market should cool down when the 10-year yield gets above 1.94%, but this is not something to expect for 2021. I hope I am wrong about this because I am cheering for higher yields to cool our unhealthy market. The U.S. economy led the world out of the recession, and it was the most significant economic comeback in history. Even with that, however, I couldn’t bring myself to forecast that 10-year yields will go higher than 1.94% for 2021

“For the housing market in 2021, the range in the 10-year yield will be between 0.62% and 1.94%, but consider these caveats…For the 2021 housing market, I would like to see the 10-year yield in the range of 1.33% to 1.60%. If we accelerate vaccinations and provide disaster relief as part of a year-long economic recovery plan, then getting to 1.33% and higher is achievable. I would be terribly disappointed if we didn’t see 1.33% on the 10-year yield in 2021.”

Notice, I have not said a peep about the MBS market when it comes to home prices. I have not discounted the value this market has to promote a less volatile mortgage market — it is just not a component that needs to be considered when talking about the long-term down trend in mortgage rates.

What about inflation, growth, and federal debt?

Since I was about five years old I’ve been hearing from grandpa that the massive federal debt that was being accumulated during my lifetime would haunt me in my adult life. “We’re leaving all this federal debt to our grandkids – they will be paying enormous taxes to pay off our egregious spending”, was the sorrowful lament I heard all the freaking time. It could make a kid mad.

So, decades go by, Grandpa has passed, and as he prophesied, the federal debt has been rising. But despite this, in 2021 my federal tax rate has never been lower. The truth is the bond market doesn’t give a hot potato about federal debt. Mortgage rates of course followed the 10-year yield trend as well.

In fact, back in 2019, I wrote about how we should see $71 trillion in federal debt by 2060 and that is a conservative take on federal debt too.

When we think about MBS, it’s the historical downtrend in bond yields that matters, not federal debt and not tapering. To break this downtrend, we would need spending and wage inflation to take off and a lot of economic growth for several years. Next year we will likely see a watered-down fiscal spending plan, plus the world economies will be further along in their recovery from the COVID-crisis.

This environment will be more conducive to getting bond yields over 2%. And if that happens, mortgage rates will also go up. However, the notion that mortgage rates can blow up higher with the 10-year yield still below 2% seems like an urban legend.

July 4th is now in the rearview mirror, and we can safely speculate that we will have slightly more total home sales than what we saw last year. In the next couple of years, 2022-2023, housing will have the best demographic for first-time home buying, ever. Hopefully, inventory levels have bottomed, so we will see inventory move back to 1,520,000. This is something I talked about recently on HousingWire.

I’m hoping for increasing inventory because the current market housing market has price inflation that is moving so fast that the price growth I expected in five years has already happened in two years. I would like to see a more balanced market because most Americans buy homes as shelter, and they deserve to have choices.

The price inflation in the new home sales market is even more concerning because that sector is more critical to the economy than the existing home sales marketplace because of construction jobs, housing starts, and purchasing of new big-ticket items.

If I am wrong about expanding inventory, then that means our strong housing demographics plus our move up, move down, cash and investor buyers simply are too big to allow inventory to get back to 1,520,000, which is still historically low. However, when we talk about rates, don’t put all your eggs in the MBS basket — look instead to the bond market.