On Wednesday the Federal Reserve hiked interest rates 0.25%, which has forced me to raise my second recession red flag on this historic economic recovery and expansion.

From the Federal Reserve: Indicators of economic activity and employment have continued to strengthen. Job gains have been strong in recent months, and the unemployment rate has declined substantially. Inflation remains elevated, reflecting supply and demand imbalances related to the pandemic, higher energy prices, and broader price pressures.

The invasion of Ukraine by Russia is causing tremendous human and economic hardship. The implications for the U.S. economy are highly uncertain, but in the near term the invasion and related events are likely to create additional upward pressure on inflation and weigh on economic activity.

The first Fed rate hike isn’t going to take us into a recession, it just raises the second of the six flags we would need to go into a recession. But looking forward, the Federal Reserve has now started to pull back from their accommodative stance because they believe the economy is too strong and the concern right now is to fight inflation with rate hikes.

From the Fed: The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. With appropriate firming in the stance of monetary policy, the Committee expects inflation to return to its 2 percent objective and the labor market to remain strong. In support of these goals, the Committee decided to raise the target range for the federal funds rate to 1/4 to 1/2 percent and anticipates that ongoing increases in the target range will be appropriate. In addition, the Committee expects to begin reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities at a coming meeting.

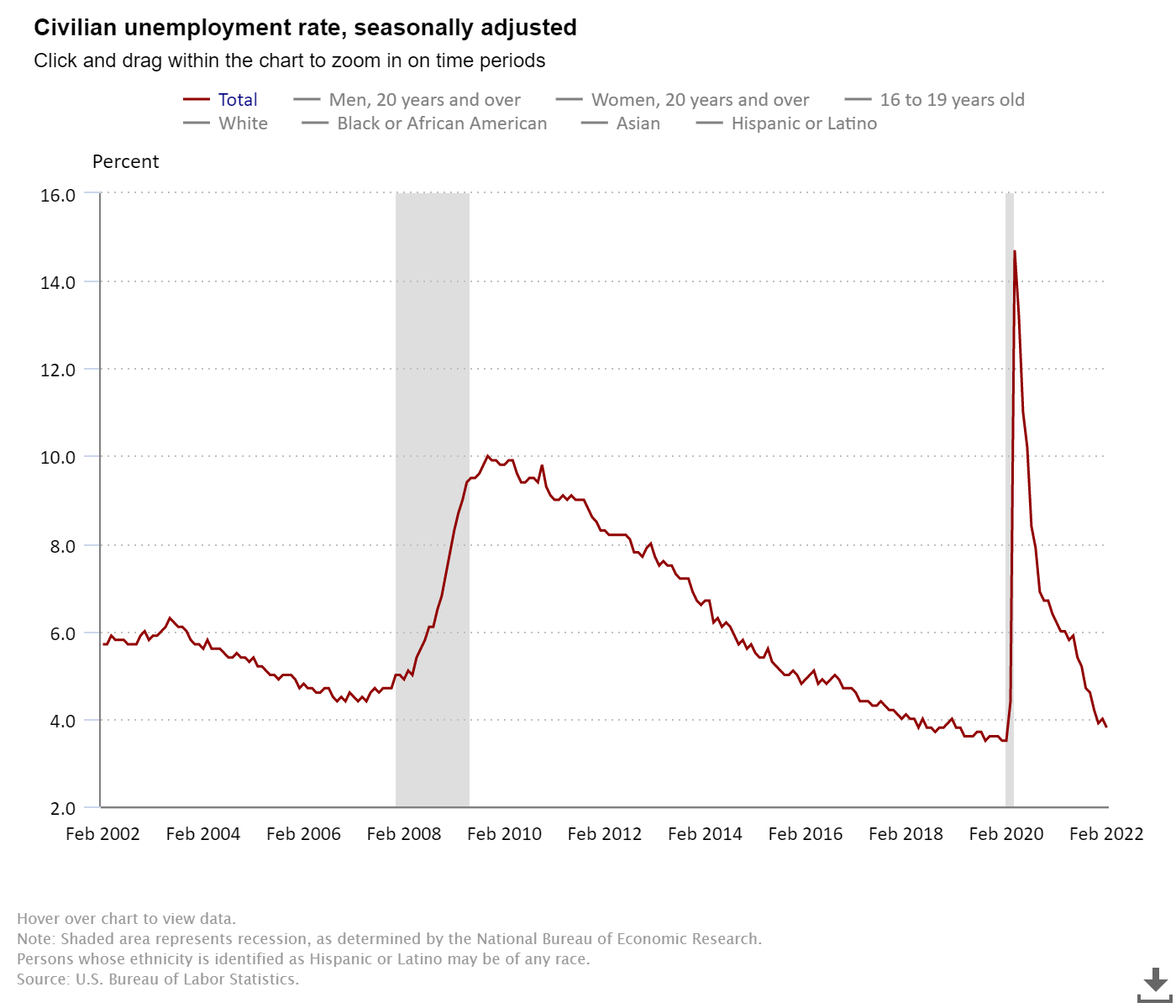

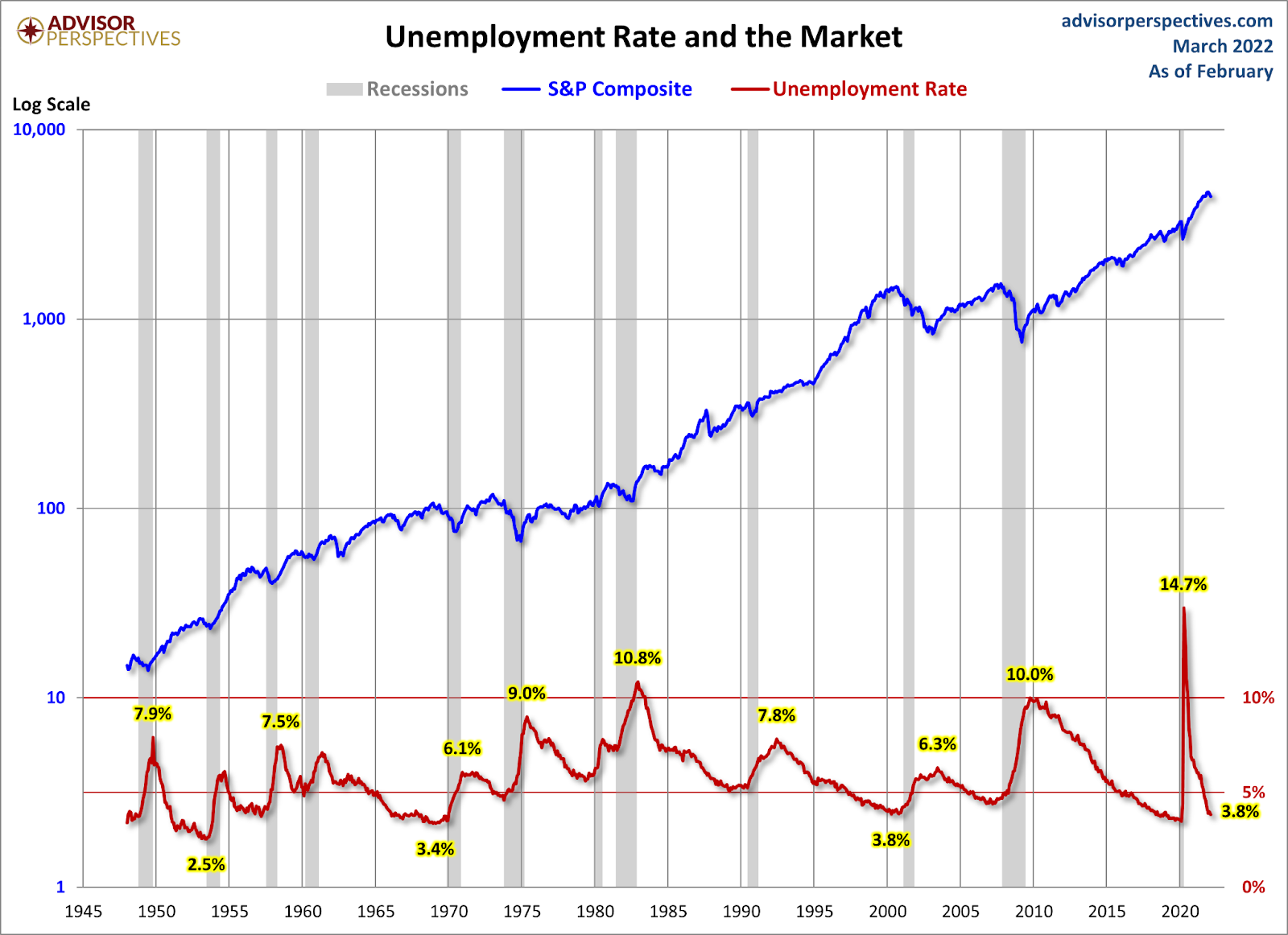

I raised the first recession red flag when the unemployment rate got to 4% and the two-year yield got over 0.56%. Again, this red flag showed the progression of an economic expansion, and the recovery was so extreme that the unemployment rate fell very fast.

The low unemployment rate isn’t a recession factor, but all expansions end when the unemployment rate is at the lowest level. I am trying to show you the stages of an economic expansion into a recession, which is why I believe in the red-flag model.

The Russian Invasion of Ukraine is a brand new variable shock to the global economy that needs to be monitored daily. Unlike COVID-19, there is no fiscal disaster relief and no rate cuts coming. The Federal Reserve’s job is to cool down this hot economy, so the economy now has pressures on two fronts.

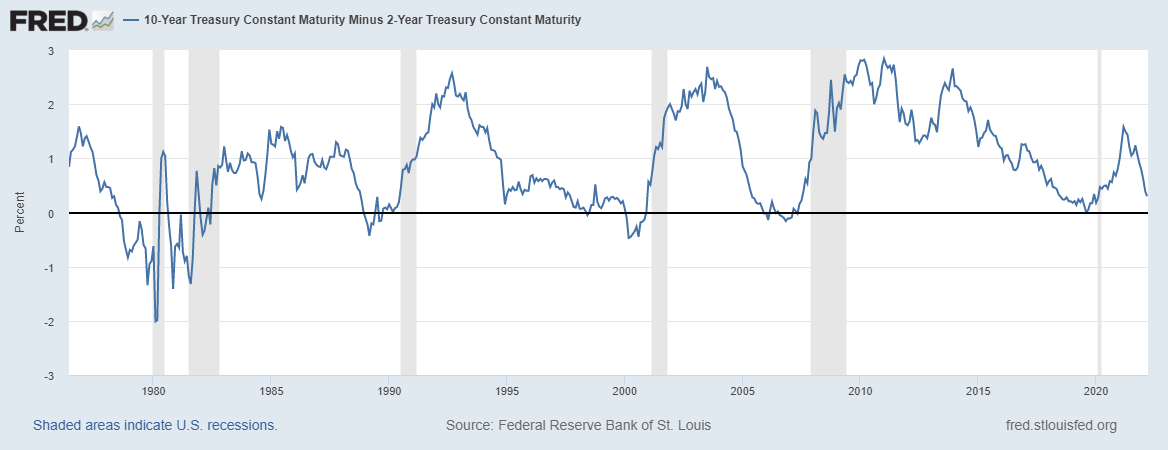

Recession red flag No. 3: The inverted yield curve

As I am writing this article, the 10-year yield is 2.17% and the two-year yield is 1.94% which means the inversion spread is now 0.23%. Historically speaking, when the 10-year yield and the two-year yield meet to say hello and shake hands (the inversion), the recession isn’t too far off. In the chart below, the grey shaded bars show when the economy is in a recession and the black in the middle is when the 10-year and 2-year yields shake hands.

How we get to higher yields

I am big fan of higher yields to create balance in the housing market. However, in 2021 I did not believe we had the capacity for the 10-year yield to break over 1.94%, which would get us to 4% plus mortgage rates. However, part of my 2022 forecast was that if global yields rise, especially in Japan and Germany, the 10-year can get up to 2.42% this year, which means 4% plus mortgage rates.

From the forecast: “We had a few times in the previous cycle where the 10-year yield was below 1.60% and above 3%. Regarding 4% plus mortgage rates, I can make a case for higher yields, but this would require the world economies functioning all together in a world with no pandemic. For this scenario, Japan and Germany yields need to rise, which would push our 10-year yield toward 2.42% and get mortgage rates over 4%. Current conditions don’t support this.”

The economy has been on fire for some time now, but only recently has the 10-year yield been able to breach over 1.94%. This is mainly due to global yields rising not so much of the U.S. We have the hottest economic and inflation data in decades and the 10-year yield is only at 2.17%. Now the tug of war begins: Can the U.S economic data can stay firm with all this inflation and higher rates, or will the weakening economy send yields lower again?

As someone who has been rooting for higher rates because the housing market is savagely unhealthy, I hope it can create some balance. If economic data gets weaker, I am concerned rates will go back down again. We lose our only variable that can create balance in the housing market.

I believe in economic models as they keep us in line. In this day and age of boom and bust 24/7 marketing for clicks, I understand that boring economic models might not be so sexy. However, economics isn’t supposed to be a hot summer flick. I always want to be the detective and not the troll. The main reason I continued writing after 2015 wasn’t because of the housing market work I have done — I wanted to be a source of information for the economic expansion and recession that wasn’t predicated on extreme ideological or stock trader takes. This is why I wrote the America Is Back Recovery Model on April 7, 2020.

So to wrap it all up, the second recession red flag is up, and I am keeping an eye out on the third one. Once that bridge is crossed, I will update the model accordingly. We will hold hands together as we continue this slow dance of information, and when something meaningful pops up, I will let you know about it. Buckle up for the rest of the year and root for more housing inventory; we need to get back to 1.52 – 1.93 million!

An interesting take, thank you!