This article is part of our HousingWire 2022 forecast series. After the series wraps early next year, join us on February 8 for the HW+ Virtual 2022 Forecast Event. Bringing together some of the top economists and researchers in housing, the event will provide an in-depth look at the predictions for next year, along with a roundtable discussion on how these insights apply to your business. The event is exclusively for HW+ members, and you can go here to register.

Most of the time, the economy is like a slow-moving ocean liner that changes direction gradually and without much effort. But when a new, powerful variable presents itself, like the worldwide COVID-19 pandemic, the economy can change on a dime. COVID was a veritable iceberg for our ocean liner economy, but the ship did not go down! Even in the extreme conditions of COVID-19, my general premise on housing economics predicted that the two variables with the most influence — demographics and mortgage rates — would hold up the housing market. With those two factors still very much in play, here is my 2022 forecast.

2022 Forecast series

The 10-year yield and mortgage rates

The forecast

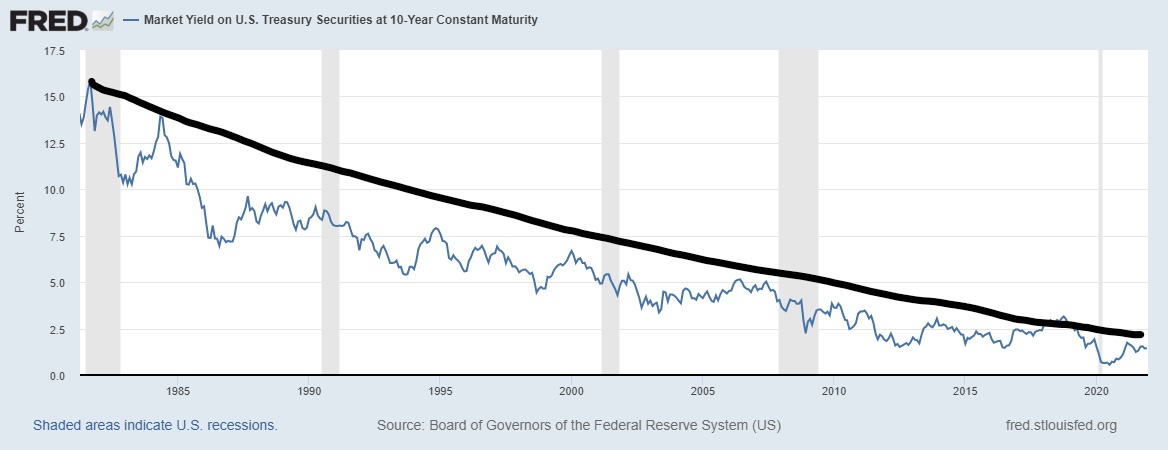

For 2022, my range for the 10-year yield is 0.62%-1.94%, similar to 2021. Accordingly, my upper end range in mortgage rates is 3.375%-3.625% and the lower end range is 2.375%-2.50%. This is very similar to what I have done in the past, paying my respects to the downtrend in bond yields since 1981.

We had a few times in the previous cycle where the 10-year yield was below 1.60% and above 3%. Regarding 4% plus mortgage rates, I can make a case for higher yields, but this would require the world economies functioning all together in a world with no pandemic. For this scenario, Japan and Germany yields need to rise, which would push our 10-year yield toward 2.42% and get mortgage rates over 4%. Current conditions don’t support this.

The backstory

The lifeblood of my economic work depends greatly on the ebbs and flows of the 10-year yield, even more than mortgage rate targeting, which is unusual for a housing analyst.

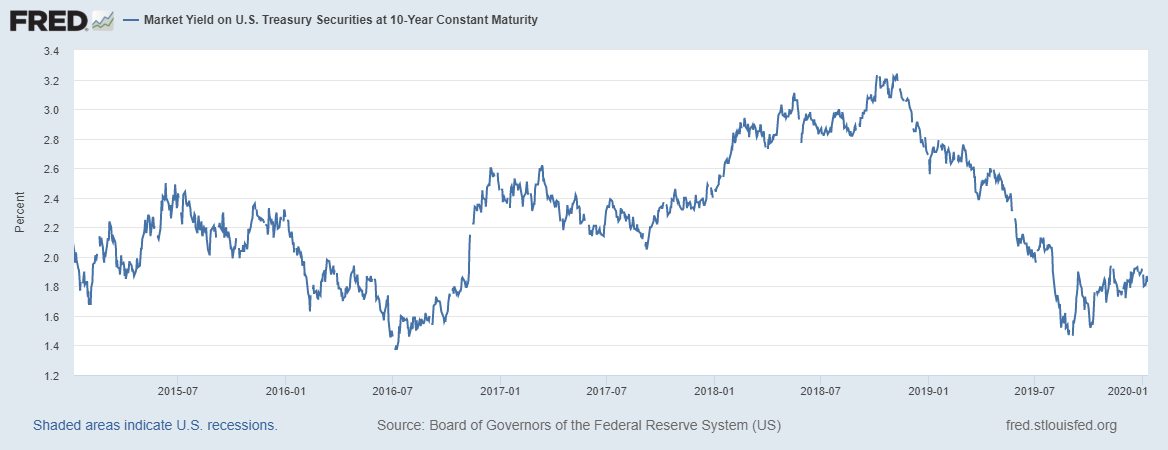

When I first dipped into 10-year yield and mortgage rate forecasting in 2015, during the previous expansion, I said the 10-year yield will remain in a channel between 1.60%-3%. I’ve stuck to that channel forecast every year since — and for the most part that 10-year yield channel stuck. That range dictated that mortgage rates would roughly stay between 3.5%-4.75%.

When COVID-19 was about to hit our economy, I forecasted that the 10-year yield recessionary yields should be in a range between -0.21%-0.62%. We got to as low as 0.32% on that Monday morning in March when the crisis was hitting the markets the hardest. About a month later, I published my AB (America is Back) recovery model, which said that the 10-year yield should get back toward 1%. We got there in December of 2020 so I was able to retire my America is Back recovery model.

I said that when the economy was beginning the new expansion, the 10-year yield would create a range between 1.33%-1.60%. This couldn’t happen in 2020 but should happen in 2021. Even with the hot economic growth, the hottest inflation data in decades, and the Fed rate hike discussion picking up, this range of 1.33%-1.60% has held up nicely for most of 2021, meaning mortgage rates were going to be low in 2021.

My forecast for the 10-year yield range in 2021 was 0.62%-1.94% which translates to a bottom-end range in mortgage rates of 2.375%-2.5%, and an upper-end of 3.375%-3.625%. Single mortgage rate target forecasts have not fared well over the decades because these forecasters did not respect the downtrend in bond yields since 1981.

The X factor

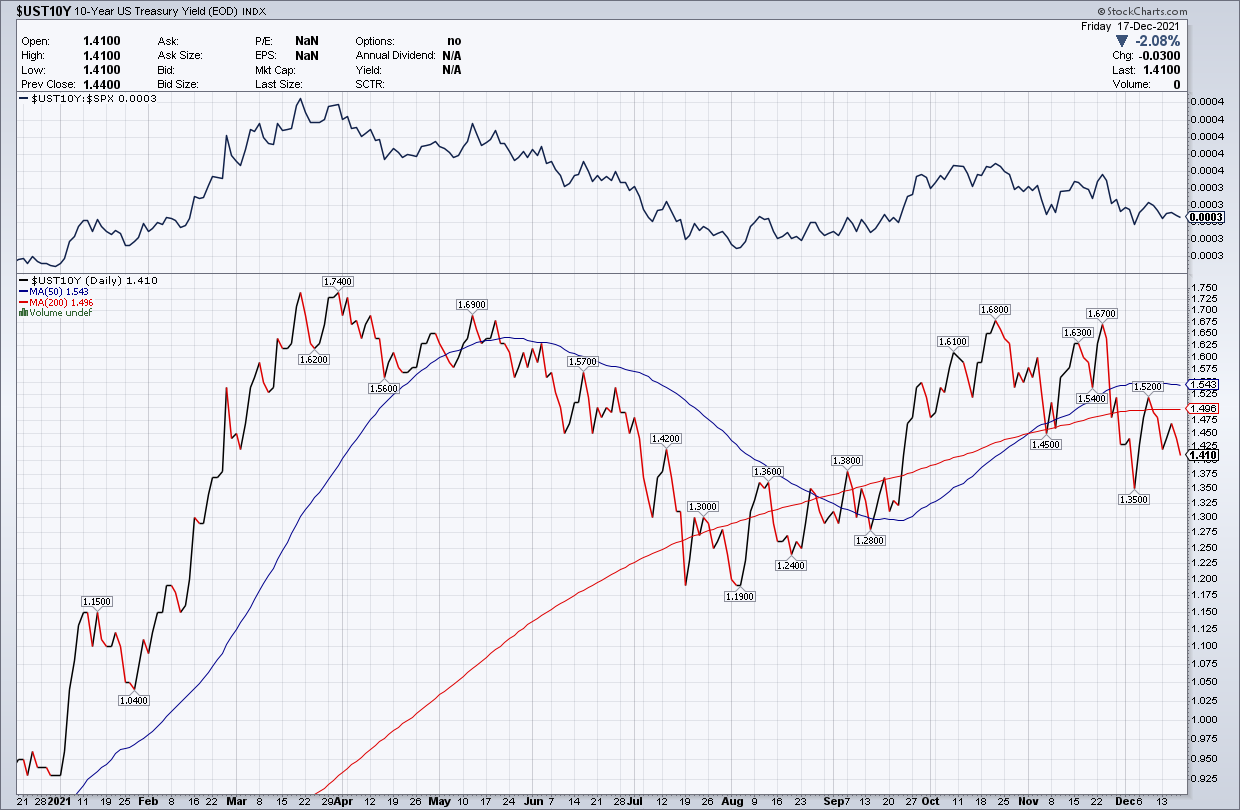

Can there be a bond market sell out short term, sending yields above 1.94%, like what we saw early in the COVID-19 crisis? Yes, but if the markets do overreact for any reason, typically bond yields would fall back. Why do I not believe bond yields will push higher aggressively? The economic rate of growth peaked in 2021. The economy was on fire this year, and inflation data was super-hot. Even so, the highest the 10-year yield got was 1.75%. The economic disaster relief that boosted the recovery in 2020 and 2021 has been drawn down.

Government spending plans have also been watered down and new legislation might not even pass at all. Economic growth peaked in 2021 and some of the hotter inflation data has the potential to fall next year. The Federal Reserve wants to hike rates to cool the economy. Typically what happens before the first Fed rate hike is that the U.S. dollar has its biggest percent move higher ,which tends to hurt commodity prices and world growth. This is something to watch for next year as it could slow down world growth.

The economy won’t be as hot in 2022 as it was in 2021, but it will remain in expansionary mode. This type of backdrop will make it challenging for rates to rise in a big way and stay higher. The key with all my 10-year yield channel work is how long the 10-year stays in that channel during the calendar year. I have always believed this type of forecast is more useful than targeting a mortgage rate.

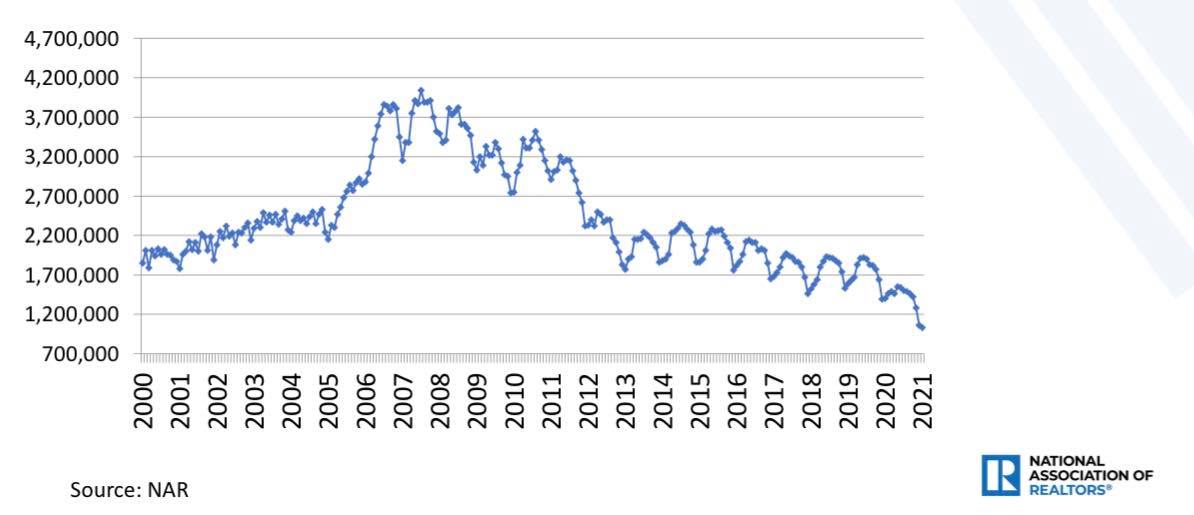

Existing-home sales

The forecast

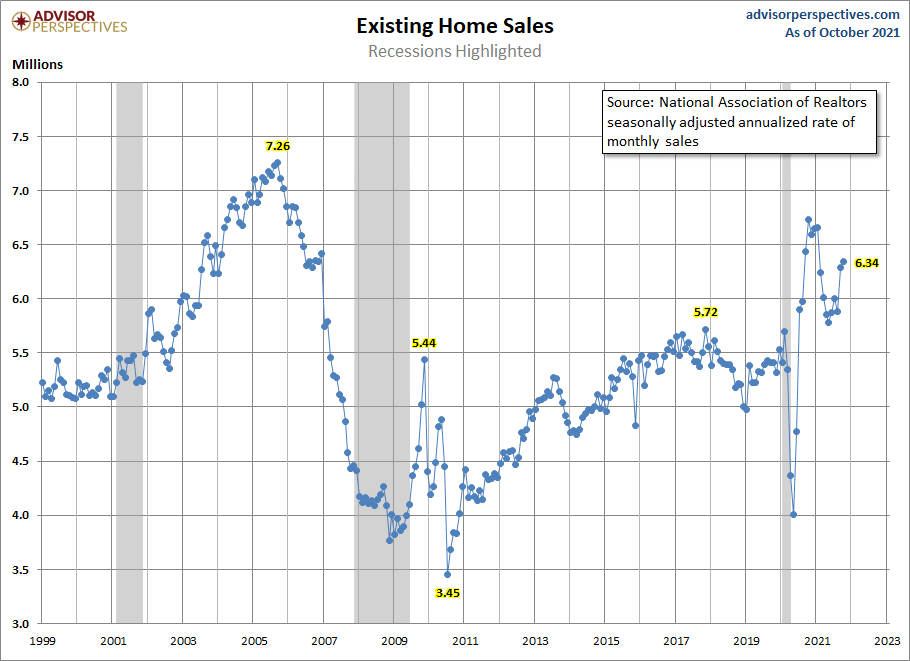

For 2022, I am forecasting the same sales trend range as 2021 of about 5.74 million to 6.16 million. If monthly sales prints are above 6.16 million for existing homes, then I would consider the market more robust than expected. If sales trend toward 5.3 million then we will be back to 2019 levels. This would still be healthy sales considering the post-1996 trend, but it will mean housing demand has gotten softer.

This has happened before when higher rates have impacted demand. This is why since the summer of 2020 I have written about how if the 10-year yield can get above 1.94%, then things should cool down. However, as you can see it’s been hard to bond yields over that level and thus mortgage rates above 3.75%.

The backstory

If the last two reports of the year on existing home sales are above 6.2 million, I will admit that sales have slightly outperformed what I predicted for 2021. Early in 2021, I wrote that home sales would moderate after the peaks caused by the COVID-19 shutdown make-up demand and that readers should not overreact to this slowing. I wrote that sales would range between 5.84 million and 6.2 million, and that we could anticipate a few prints under 5.84 million — but sales would consistently be above the closing level of 2020 of 5.64 million. We got one print below 5.84 million and a few recent prints over 6.2 million, with two more reports. Mortgage demand was solid all year long and has picked up in the last 15 weeks.

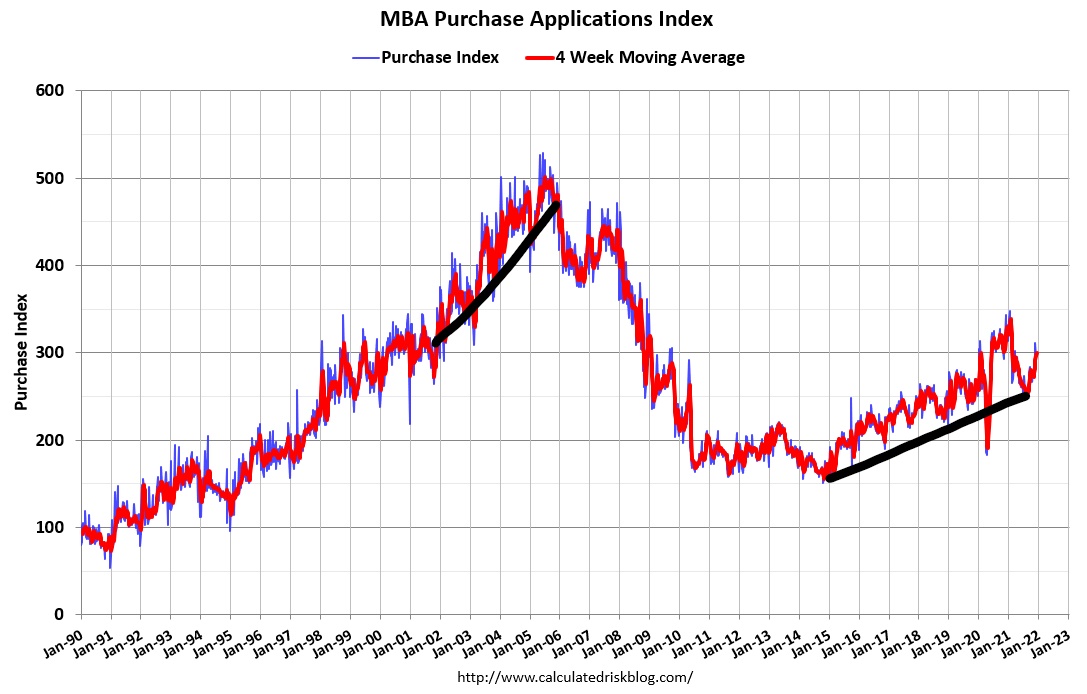

One of my longer-term forecasts in the previous expansion was that the MBA Index would not reach 300 until 2020-2024. We got there in the early part of 2020, then the Index got hit by the COVID-19 delays in home buying to only have a V-shaped recovery that led to the make-up demand surge, moderation down and back to 300.

As you can see, it’s been like Mr. Toad’s wild ride here. We will still have some COVID-19 year-over-year comps to deal with up until mid February and then we can get back to normal. However, one thing is for sure: demand has been solid and stable in 2020 and 2021. Also, the market we have today doesn’t look like the credit boom we saw from 2002-2005.

I didn’t believe total home sales could get to 6.2 million in the years 2008-2019, this is new and existing home sales combined. We simply didn’t have the type of demographics in the previous expansion. We are in different times.

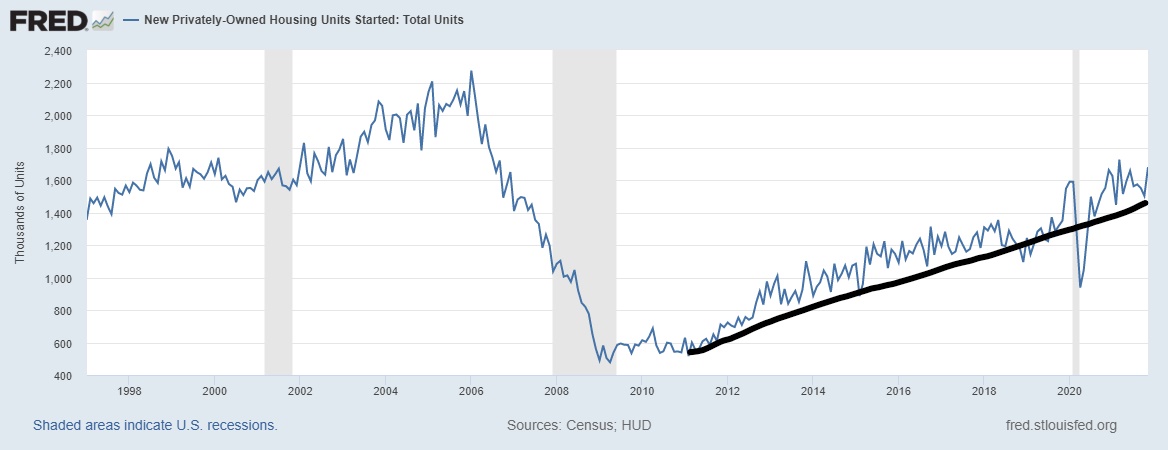

New home sales and housing starts

The forecast

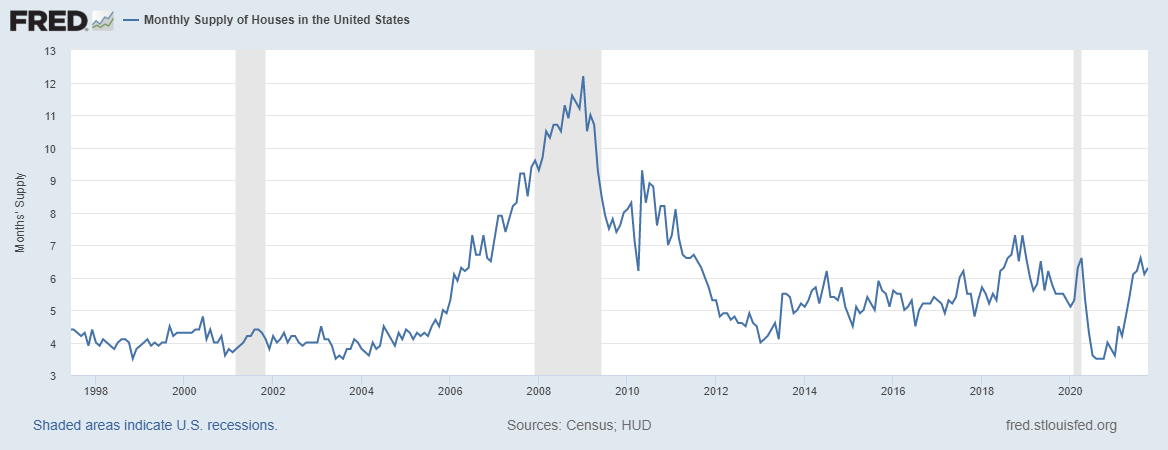

My long-term call from the previous expansion has been that we won’t start a year at 1.5 million total housing starts until the years 2020-2024 and we have finally gotten here much like the 300 level in the MBA index. My rule of thumb has always been to follow the monthly supply data for new homes, and as long as monthly supply is below 6.5 months on a three-month average, they will build.

The backstory

Housing starts, permits and builders confidence are ending the year on a good note. Even though new home sales aren’t booming this year, it’s good enough to keep the builders building more homes even with all the drama of labor shortages, material cost and delays in finishing homes.

As you can see below, the uptrend has been intact even with the slowdown in 2018 and the brief pause from COVID-19.

The new home sales sector gets impacted by rates much more than the existing home sales marketplace. The last time this sector saw some stress from mortgage rates was in 2018 when rates were at 5%. Today’s 3% mortgage rates are good enough to keep things going. We should see slow growth in new home sales and housing starts as long as the monthly supply of new homes is below 6.5 months on a 3-month average. This sector has legs to walk forward slowly. I have never believed in the housing construction boom premise as mature economies don’t have construction booms with slowing population growth. More on that here.

The X factor

The one concern I have for this sector in 2022 is if the builders keep pushing the limits of home price growth to make their margins look better. When rates are low, they have the pricing power to do this. This is why the sector has done so well in 2021. If I am wrong about mortgage rates staying low in 2022, and rates go above 3.75% with duration, then demand for new homes should get hit. The longer-term concern for this sector is price growth because if demand slows down, this means a slowdown in construction and the builders really maximized their pricing power in 2020 and 2021.

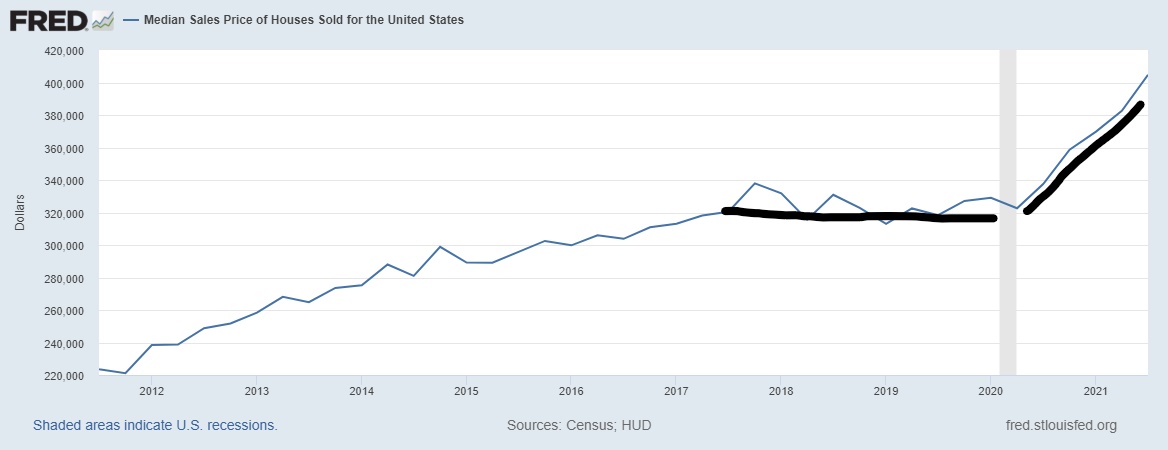

Home prices

The forecast

I am looking for total home-price growth to be between 5.2% and 6.7% for 2022. This would be a meaningful cool down in price growth but would still be a third year straight of too much price growth for my taste.

The backstory

My biggest fear for the housing market during the years 2020 to 2024 was that real home-price growth can be unhealthy. When you have the best housing demographic patch ever recorded in history occurring at the same time as the lowest mortgage rates ever, with housing tenure doubling as it has in the last 12 years, it’s the perfect storm for unhealthy price growth.

Housing inventory has been falling since 2014 and mortgage purchase applications have been rising since then. As you can see below, 2021 wasn’t looking good for me regarding my fear for home prices rising too much.

The X factor

When I talk about real home-price growth being too hot, I mean that nominal home price growth is above 4.6% each year during the five-year period of 2020 to 2024, for a cumulative 23% growth. This would not be a positive for the housing market. If we end 2021 with 13% home price growth, (and it looks like we will do that or higher), then we have already achieved 23% of the price growth that I am comfortable with in just two years.

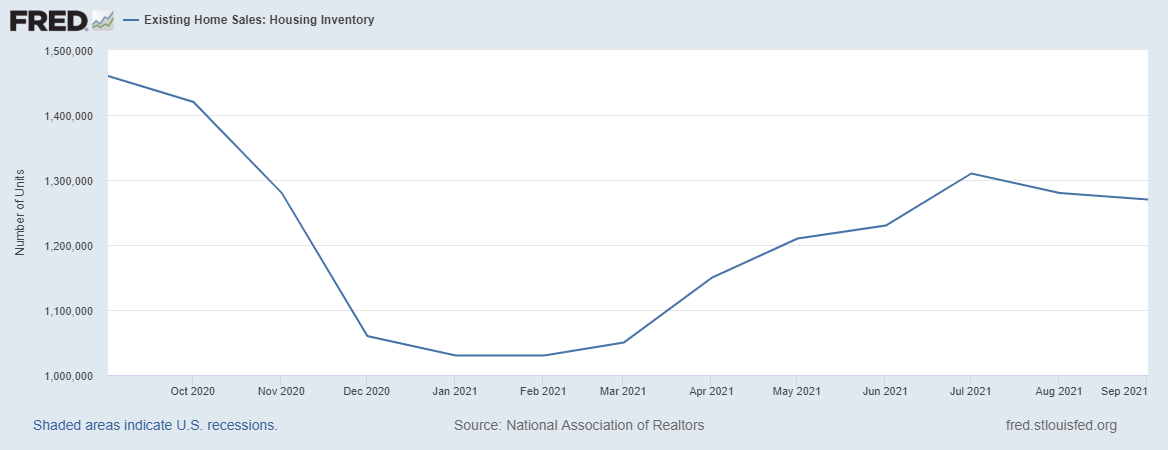

While I do believe home-price growth is cooling from the extreme high rate of growth we had earlier in the year, I would very much like to see prices get back in line with my model for a healthy market. In order for this to happen, we would need to have no increase in home prices for the next three years. Because inventory levels are falling again, and we are at risk of starting the 2022 spring season at fresh new all-time lows, this outcome is very unlikely.

Early in 2021, I had raised concerns that prices overheating should be the main concern, not forbearance crashing the market. When demand is stable, it’s extremely rare for inventory to skyrocket and American homeowners have never looked better on paper. In fact, a few months ago I talked about inventory falling again should be the concern going out.

Housing demand

The forecast

Everyone is talking about rates going higher and no one, it seems, is talking about the possibility that mortgage rates could go under 3% in 2022, except me. This is front and center in my mind. I want to see a B&B housing market: boring and balanced. In a B&B market, buyers have choices, sales move at a reasonable pace without bidding wars, and the whole home-buying experience is less stressful and more sane. I would like to see inventory get toward 1.52 – 1.93 million, (which is still historically low). However, this will be a more stable housing market.

The backstory

Millions of people buy homes each year. The only thing that cooled demand for housing in the previous expansion was mortgage rates going over 4% with duration. The increase in rates didn’t crash the market or even facilitated negative year-over-year home price declines; but it did increase the number of days homes stayed on the market.

Currently the biggest demographic patch ever recorded in U.S. history are ages 28-34, the first-time homebuyer median age is 33. When you add move-up, move-down, cash and investor demand together, demand will be stable and hard to break under the post-1996 trend of 4 million plus total sales every year in the years 2020-2024.

The X factor

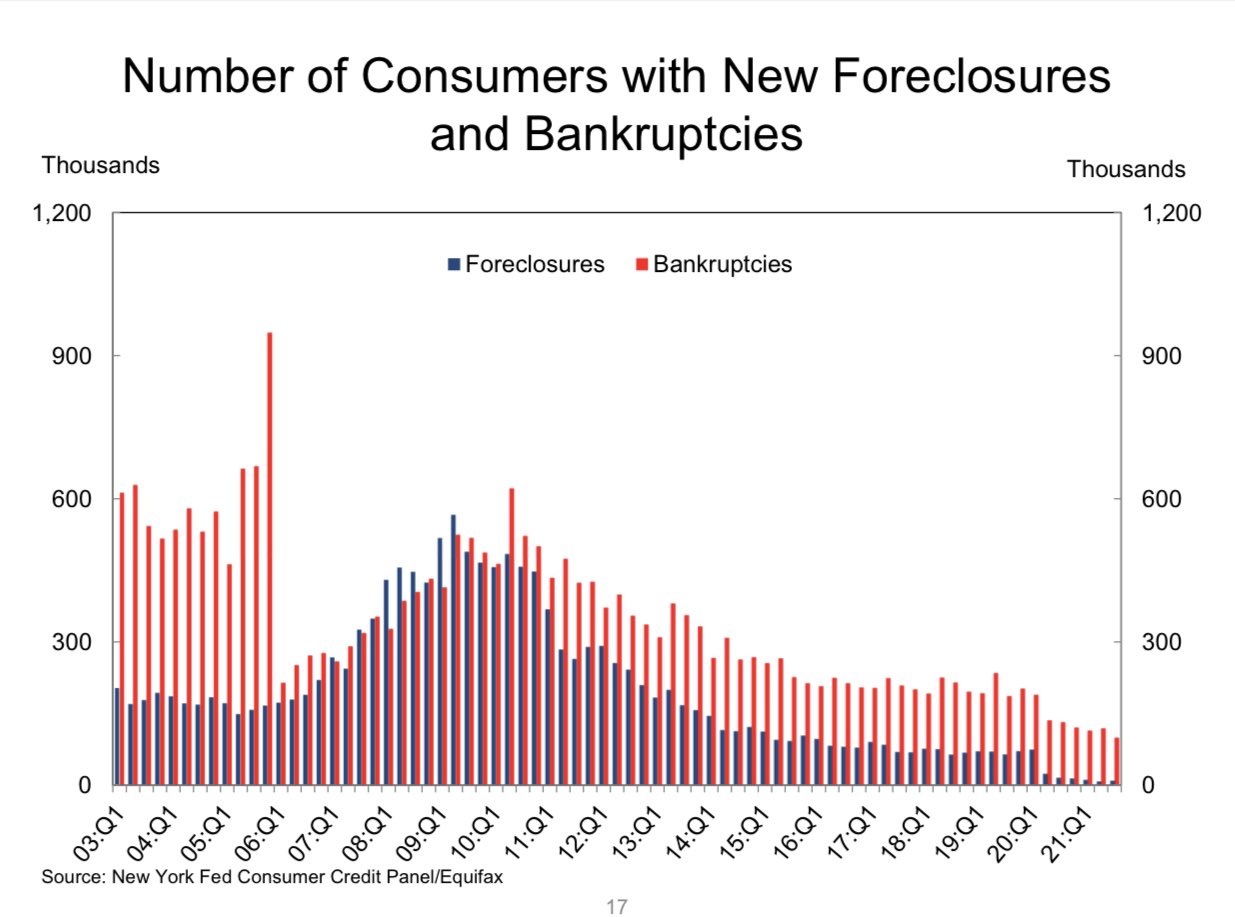

Frankly, I’m getting tired of calling this market the unhealthiest since 2010. This is not due to a massive credit boom or exotic loan products contaminating the market with excess risk — it’s the lack of choice for buyers. If mortgage rates go under 3%, which I believe they can, it just keeps the low inventory story going on. The Federal Reserves wants to cool down the economy, the government is no longer providing disaster relief anymore and the world economies should get hit if the U.S. dollar gets too strong. So, my concern is about rates falling in year three of my 2020-2024 period. This is also a first-world problem to have and we aren’t dealing with the housing market of 2005-2008 when sales were declining and the U.S. consumer was already filing for bankruptcy and having foreclosures before the great recession started in 2008. This is to give you some perspectives here with my thinking.

The economy

The forecast

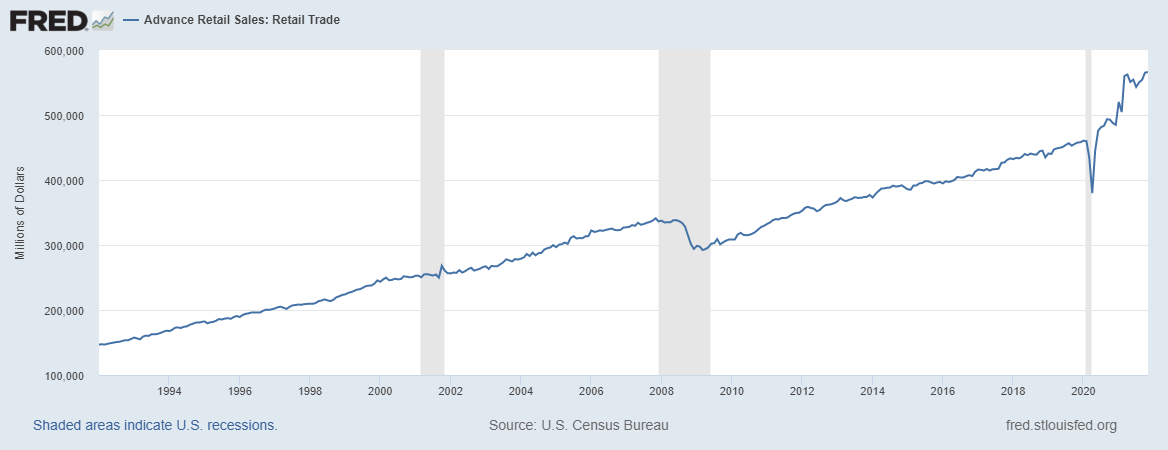

I expect the rate of change to slow in 2022 but the economy will still be expansionary. Retail sales have been off the charts, and this data line, which I expected to moderate, still hasn’t. The rate of growth will cool. Replicating the growth we saw in 2021 will be nearly impossible. As the excess savings have been drawn down and the additional checks that people got are no longer coming, this data line will find a more suitable and sustainable trend in 2022. Still I am shocked that moderation hasn’t happened already and I was the year 2020-2024 household formation spending guy, too.

The backstory

The U.S. economy has been on fire this year. Even with the excess savings, good demographics, and low rates, not even I thought we would see economic growth like we did in 2021. However, like all things in life, despite the peaks and valleys, the overall trend will prevail.

The X factor

I recently raised one of my six recession red flags after the most recent jobs report as the unemployment rate got to a key level for myself. These red flags are more of a progress checklist in the economic expansion, and when all six of my flags are raised, I go into recession watch. The economy is in a more mature phase of expansion since the recovery was so fast. Like everything with me, it’s a process to show you the path of this expansion to the next recession.

For housing, a strong labor market means more people are getting off forbearance, which is already under 1 million, much smaller than the nearly 5 million we had early in the crisis. I want to wish a Merry Christmas to all my forbearance crash bros who promised a housing crash in 2020 and 2021. You guys are the best trolling grifters ever!

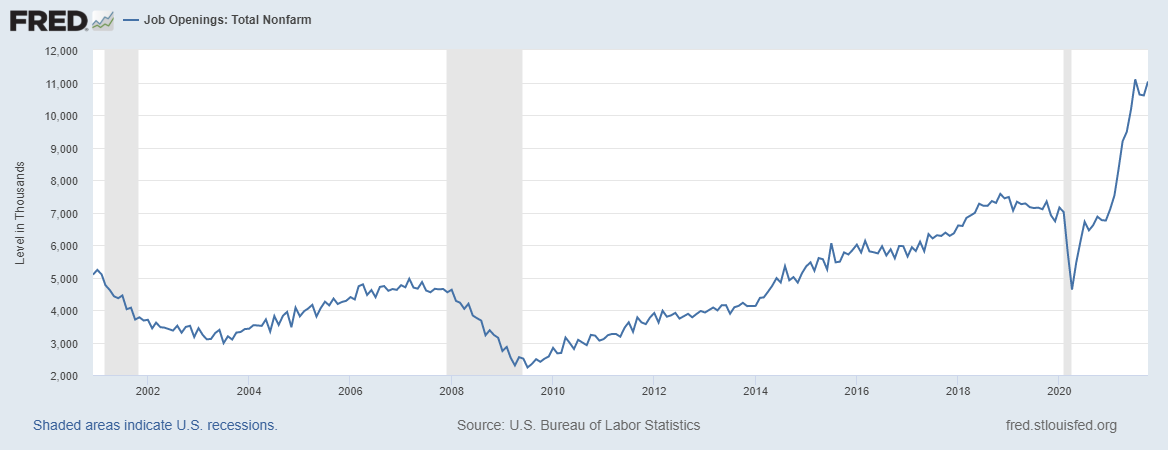

More jobs and more robust wage growth mean the need for shelter will grow. The housing market is already dealing with too much rent inflation, but as wage growth picks up on the lower end, this means landlords will charge more rent. Again, this the problem you want to have, a tighter labor market means wage growth will pick up and we have 11 million job openings currently.

So, look for the rent inflation story to be part of the 2022 storyline, as well as the rate of growth of home prices cooling down.

There is nothing like a fifth wave of COVID-19 and a new highly transmissible variant to crank up the personal stress meter. While the continuing COVID crisis can cause havoc on some short-term data lines for the economy, we will, as we have done, get through this and move forward. Our reality is that, as a nation, we have learned to consume goods and services with an active virus infecting and killing us every day.

The St. Louis Financial Stress Index, which was a key data line to track for the America Is Back recovery model, has still been in a calm zone for the entire year, currently at -0.8564. When we break over zero — which is considered normal stress — then we have some market drama. However, that wasn’t the storyline in 2021 and we didn’t have a single day where the S&P 500 was in correction mode. It’s not normal to not have a stock correction, so a stock market correction in 2022 is in the works and this can lead more money into bonds and drive rates lower.

For more discussion on this index and the America is Back recovery model, this podcast goes over everything that has happened in 2020-2021.

Conclusion

What a ride it has been for all of us since April 7, 2020 when I wrote the America Is Back economic recovery model for HousingWire. We end 2021 with one of the greatest economic recovery stories ever in the history of the United States of America, and a terrible, dark, two-year period of failure for the extreme housing bears. Now we are well into a recovery and looking forward to a new year with its new challenges.

The job of the analyst is to forecast the positive or negative impacts that a whole slew of variables have on the economy based on carefully formulated economic models. The variables, such as demographics, the unemployment rate, what the Federal Reserve is doing, commodity prices and so many others, are constantly in flux and feed off of and influence one another. Additionally, new economic variables pop up all the time. My job, with every podcast and article, is to show you how the changes in these variables light the path to where the economy and the housing market is heading.

Take a deep breath — in through the nose and out through the mouth. The last two years have been crazy, but I am glad you are here to read this. This is our country, our world and our universe, and everyone is part of team Life on Earth. Merry Christmas, Happy Holidays and have a wonderful Happy New Year. We will get through 2022 one data line at a time.

“We have always held to the hope, the belief, the conviction that there is a better life, a better world, beyond the horizon.” Franklin D. Roosevelt

This is a fantastic article that I shared with my entire sales team. Thank you for your keen insight and unique perspective.

You’re most welcome, Stacy