Painter Kenneth Noland said, “Context is key – from that comes the understanding of everything.” Whether that is true in the world of art I could not tell you, but it is most certainly true in the world of economics. What are numbers but meaningless points? It is when those points are considered in the context of what has happened before and what we expect to happen in the future that they become imbued with meaning. With that in mind, I would like to revisit my 2020 thoughts on U.S. housing market data and compare to where we are today — in the middle of one of the most epic years in our country’s history, due to COVID-19.

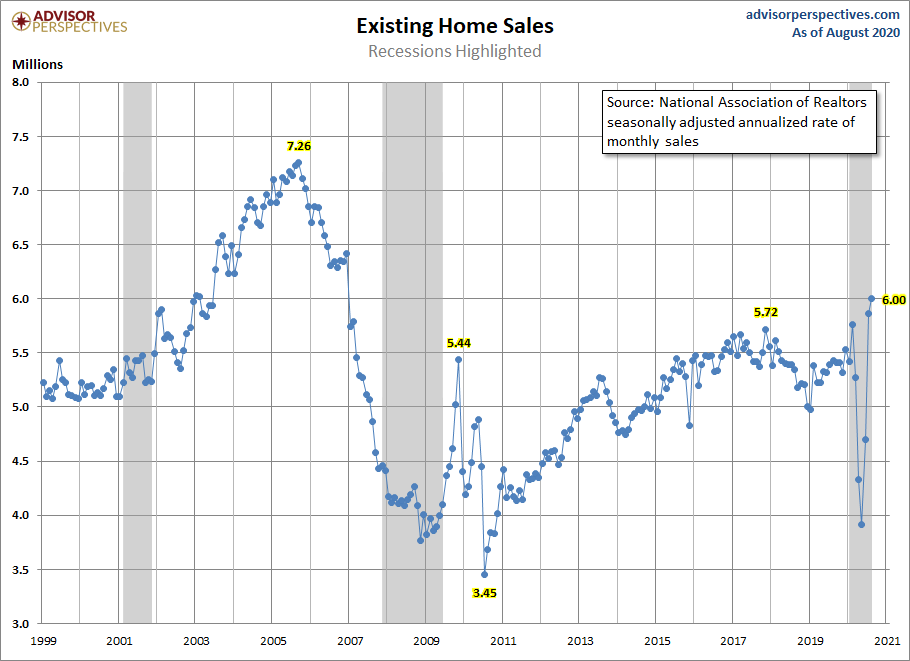

No doubt about it, the COVID crisis has taken some juice out of the 2020 housing market. The February housing data, pre-COVID, was juicy indeed. For the first time since the early part of the century, housing was the sector outperforming in the economy rather than a lackluster underperforming sector. If the February trend continued, total existing home sales would have been higher: we probably would have ended the year with sales between 5,710,000 and 5,840,000, a noticeable jump from last year’s number of roughly 5.3 million.

Woulda, coulda, shoulda. Even with today’s 6 million existing home sales print, we are down 3.2% compared to 2019 levels.

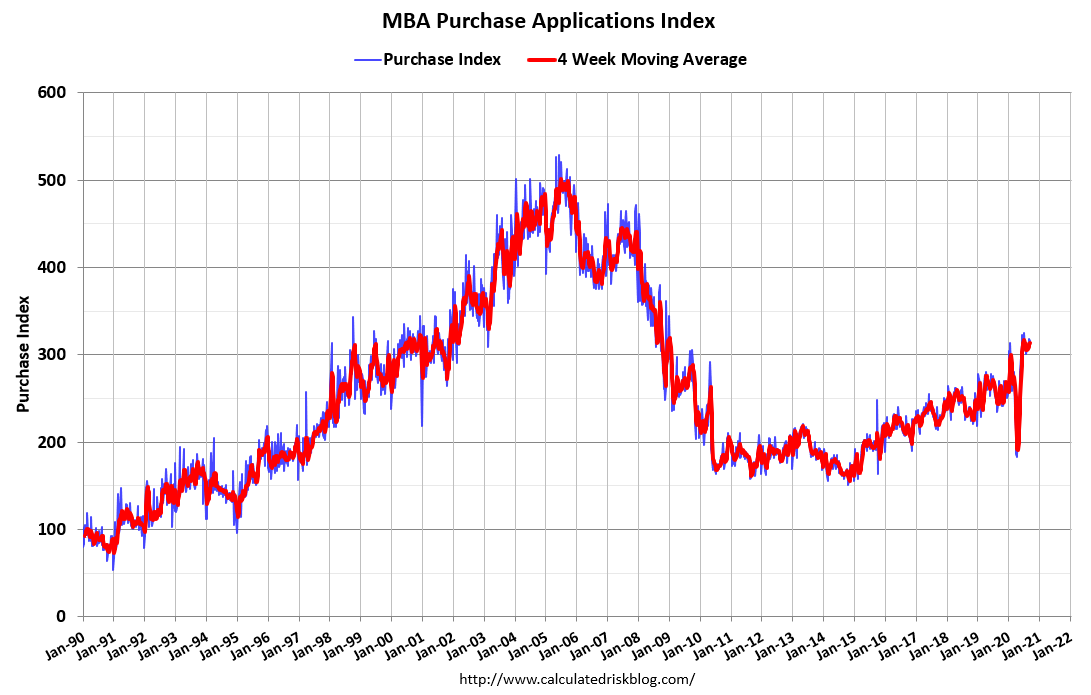

But, even with the COVID-19 crisis, we have had 17 straight weeks of double-digit year-over-year growth in MBA purchase applications data following a nine-week period of negative year-over-year numbers.

We have seen on average in the last 17 weeks roughly 20% year-over-year growth. But don’t expect the 20% plus year-over-year growth in purchase applications to continue. Some of the positive growth was catch-up demand from those nine weeks of a frozen market due to COVID-19. Even if growth fades toward single digits or even flat, this doesn’t mean a crash is coming in two weeks. If 2020 has taught you anything, it’s that the American housing bubble home price crash bears in the past few years have no idea what they’re talking about because all they care about is trolling for clicks — these are not real economic people. This is why I gave them the new nickname Forbearance Home Price Crash Bros.

The big question for the rest of 2020 is whether or not we will get total home sales of 6.2 million. The context for this number is that from 2008-2019 my belief was that we would have the weakest housing recovery ever, but in the years 2020-2024, our demographics for housing became vastly improved. I have never had a forecast of total home sales (new and existing home sales combined) 6.2 million or higher until this year. Today’s existing home report at 6 million and the solid growth in new home sales means we still have an outside shot to hit my 2020 high range forecast levels even with this pandemic. It is not out of the question that we can get to 6.2 million total home sales by the end of the year.

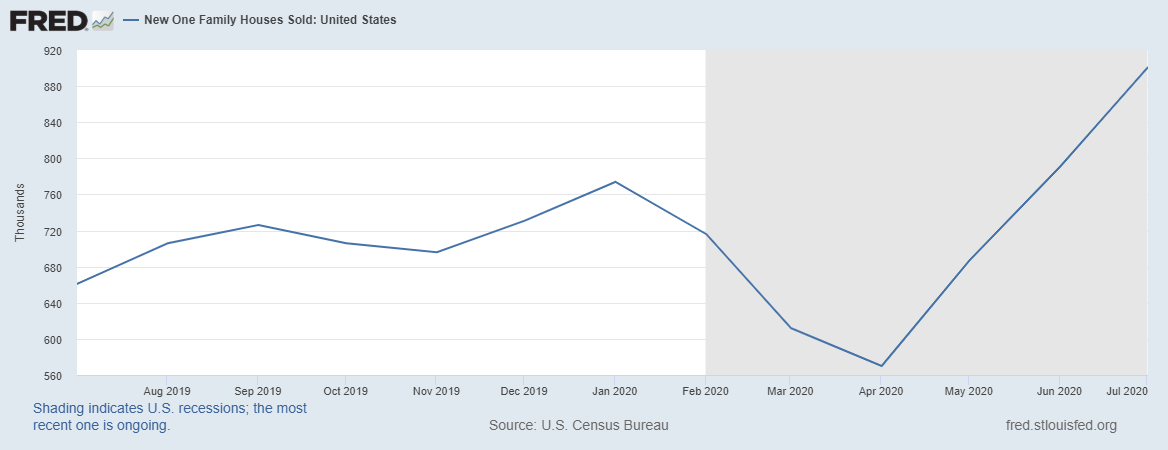

The new home sales market is doing well as it really benefits from lower mortgage rates. I have said for many years that we wouldn’t see total housing construction start a year at 1.5 million until the years 2020-2024 because we would need to start the year with over 737,000 new home sales in order for developers to see the need for that amount of building. 2020 is looking great on that front for the new home sales market and housing starts, which need more new home sales to warrant more single-family construction.

My biggest concern for housing in 2020-2024 is that real home prices could take off. Good housing demographics, housing tenure at 10 years and low mortgage rates are a perfect recipe for unhealthy home-price growth. The median sales price is now 11.4% higher than a year ago. I’m not saying that home-price growth will somehow morph into a speculation bubble like it did in the 2000s — our credit lending standards will prevent that — but housing could become considerably less affordable even with low mortgage rates if this continues.

Because housing is becoming an outperforming asset, we may see an increase in cash buyers in 2021 as a percent of sales. In today’s existing home sales report they were at 18%. Housing may be an attractive place to park money for yield returns when yields are low elsewhere, and this could also increase demand slightly in 2021. I wouldn’t put too much weight on this story because it’s a smaller portion of total home-sales demand.

The reality for housing has always been the same: Housing is the cost of shelter to your own capacity to own the debt, it’s not an investment. The majority of home buyers in America buy homes to live in, not for an investment. This is the big difference between the housing market now and what we saw in 2002-2005, when we saw a lot of speculation going on.

Rates, of course, still matter. Mortgage rates are one of the primary drivers of demand. Housing demand slowed when the 10-year yield went above 2.62% in the previous expansion. In this market, expect cooling when the 10-year yield goes above 1.94%. For the next several years the housing market is going to be a battle between good demographics driving demand and affordability keeping demand in check.

This is why I believe if we ever get total home sales above 6.2 million in years 2020-2024 I will consider this an outperforming metric compared to what we saw from 2008-2019. However, we are nowhere close to the speculation demand we saw during the bubble years of 2002-2005. When it comes to housing market data, context is key!

Also, we are nearing our peak sales capacity on these monthly sales prints for 2020. If you see a lower rate of growth sales print in the future, don’t be a fragile housing crash bear, this mindset hasn’t ended well for those that believe home sales demand is going to crash just because of a lower monthly print. It’s sporadic in the 21st century to have any existing home sales print below 4 million. It’s only happened three times this century and two of those events were one-off items such as the home-buyer tax credit and this year with the low level of sales due to COVID-19, just a tad under 4 million.

The existing home sales demand market isn’t overheating as we are still down compared to 2019 levels. Context is key! 2019 was a very healthy year for housing in that we had negative year-over-year real price gains and sales stayed flat. But more recently, price growth is rising higher as demand has picked up. We are at levels now that depend too much on lower rates. So I’m rooting for negative real home price growth again but finding it harder to get there with demand so good and rates so low.