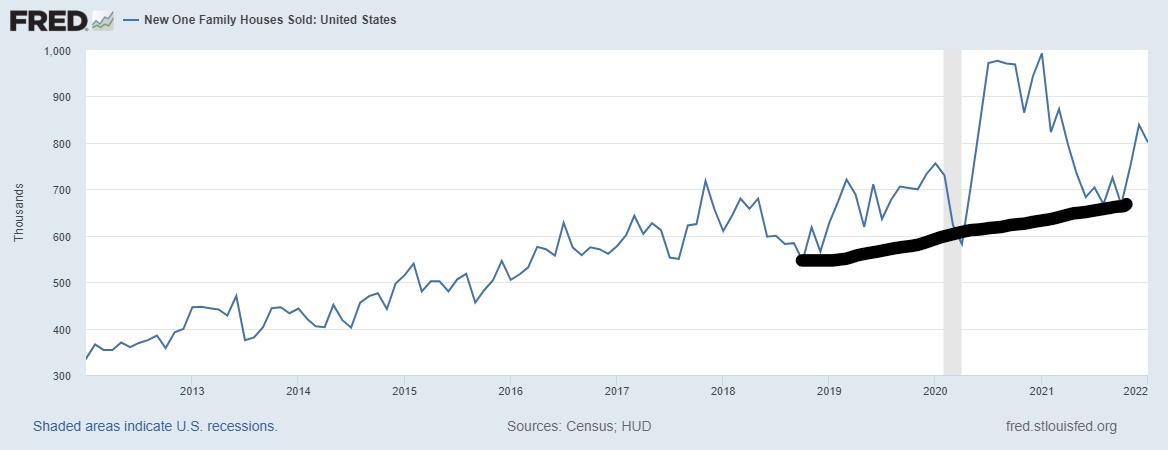

The new home sales report came in as a miss of estimates at 803,000, but positive revisions make the report much better than the headline. To be honest here, the new home sales market is stuck for now. While housing permits have been growing, completions have gone nowhere for years.

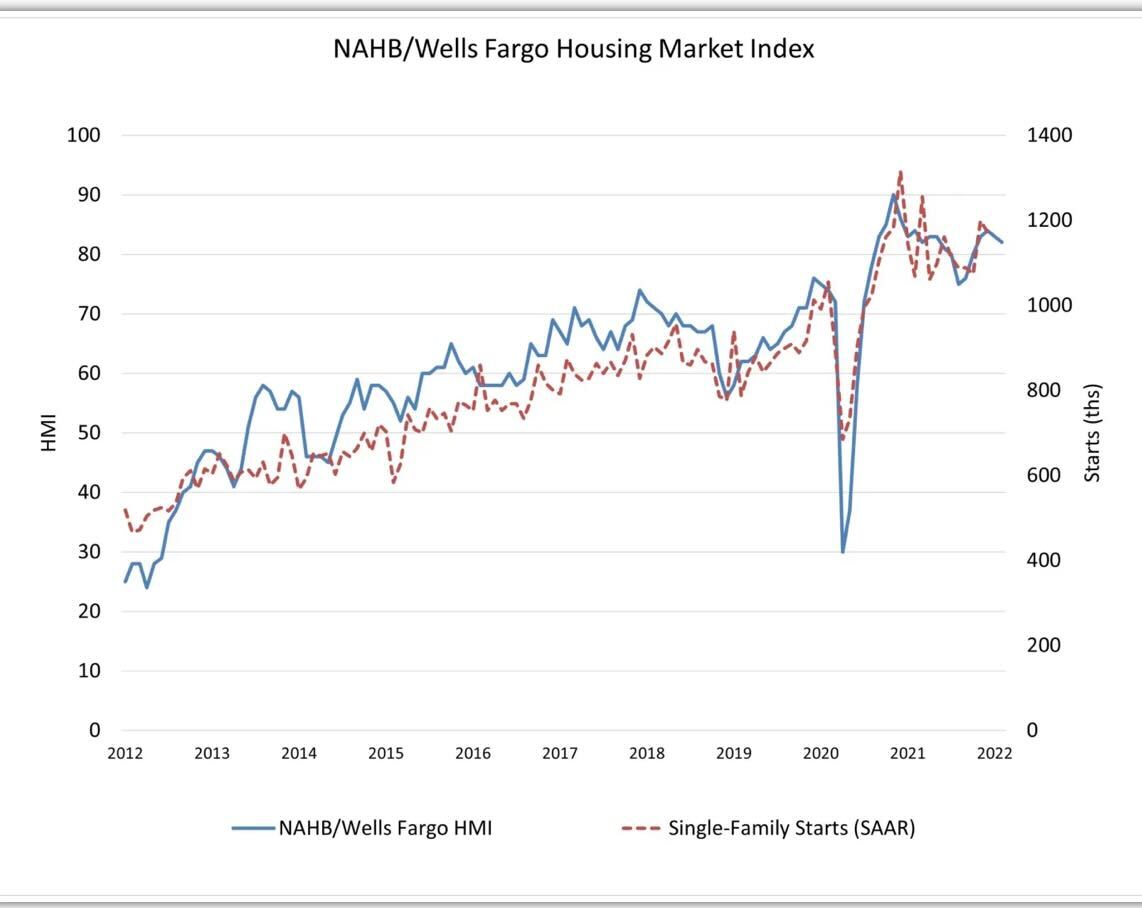

The builders have pushed their pricing power on American consumers, and as long as new home sales can grow, they will use their pricing power to offset all the other costs in this economy of higher prices and shortages. The builder’s confidence data has been stalling out the last two months, so not much is happening in this sector yet.

From the National Association of Home Builders:

For many years I have stressed that the most important housing data I follow is the monthly supply of new homes. It gives an idea of what to expect for housing construction.

From Census: The seasonally‐adjusted estimate of new houses for sale at the end of January was 406,000. This represents a supply of 6.1 months at the current sales rate.

My rule of thumb for anticipating builder behavior is based on the three-month average of supply:

- When supply is 4.3 months and below, this is an excellent market for the builders.

- When supply is 4.4 to 6.4 months, this is an OK market for the builders. They will build as long as new home sales are growing.

- When supply is 6.5 months and above, the builders will pull back on construction.

The significant positive revisions actually show up here in the data. We have gone from 6.6 months on a three-month average of supply down to six months on a three-month average. Of course, we all know how long it takes to build and finish a new home, which plays into this data. However, traditionally speaking, when sales are declining, the HMI data falls, and once we get over 6.5 months, it’s a red flag.

We don’t have that now, but I wouldn’t say this is a booming new home sales marketplace; it’s just ok. The real question is how much higher mortgage rates will bite the most sensitive sector to rates: new homes. This stands in contrast to the existing home sales market, where higher mortgage rates can create more inventory and cool down price growth. The builders will pull back on construction growth if new homes sales start to head lower. The builders need to make sure they have a sound, profitable business; this is normal and has been done for decades.

So, the impact of higher rates on demand for new homes is more negative than positive. A good example was 2018. Back then, 5% mortgage rates created a spike in monthly supply, and the builders’ stocks were down 30% plus from their recent highs. They held back on construction growth until demand got better and monthly supply went down again, which did happen in a few months.

From Census: Sales of new single‐family houses in January 2022 were at a seasonally adjusted annual rate of 801,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 4.5 percent (±16.2 percent)* below the revised December rate of 839,000 and is 19.3 percent (±15.2 percent) below the January 2021 estimate of 993,000.

The same story here with new home sales, the slow and steady ride higher from the previous expansion continues. COVID-19 has created a lot of strange-looking charts due to the surge in make-up demand in 2020-2021, but when you make some proper adjustments, you can see the uptrend in sales is still intact for now. This is also why you need to focus on revisions trend data and not the headline new home sales report because it tends to be off a lot.

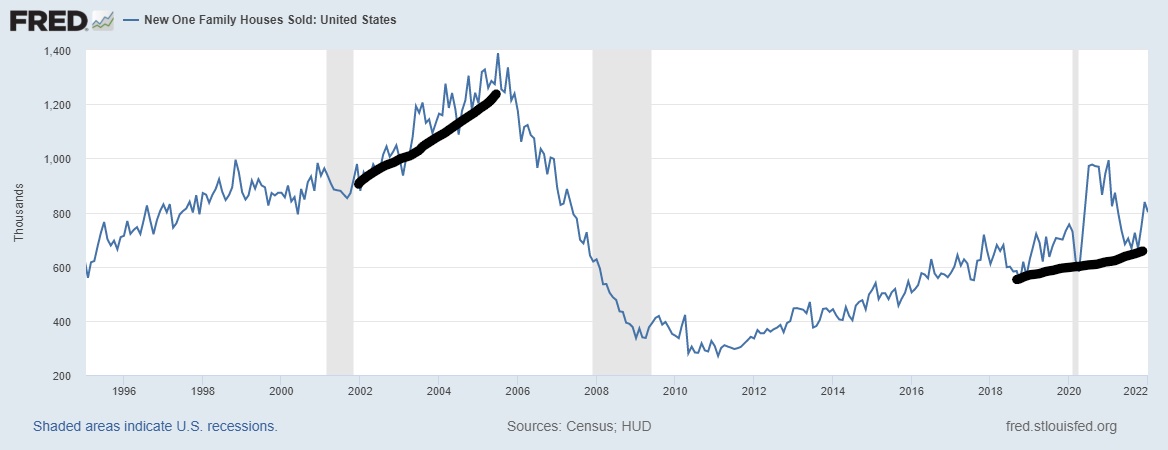

As you can see below, the market we’ve had from 2018-2022 looks nothing like the overheating demand we saw from 2002 to 2005. I have always stressed this because many extreme housing bears in America are just side-hustling professional grifters. Every housing weakness we have seen from 2012 to 2022 was supposed to be the housing bubble crash. Hopefully, my work on HousingWire over the last two years has demonstrated why this is not the case.

This is why I have stressed that we don’t have a credit housing boom and set specific home sale level targets for the years 2020-2024. If total home sales of new and existing homes combined beat over 6.2 million, consider that a good year. So far, 2020-2021 and now 2022 look to be passing that level.

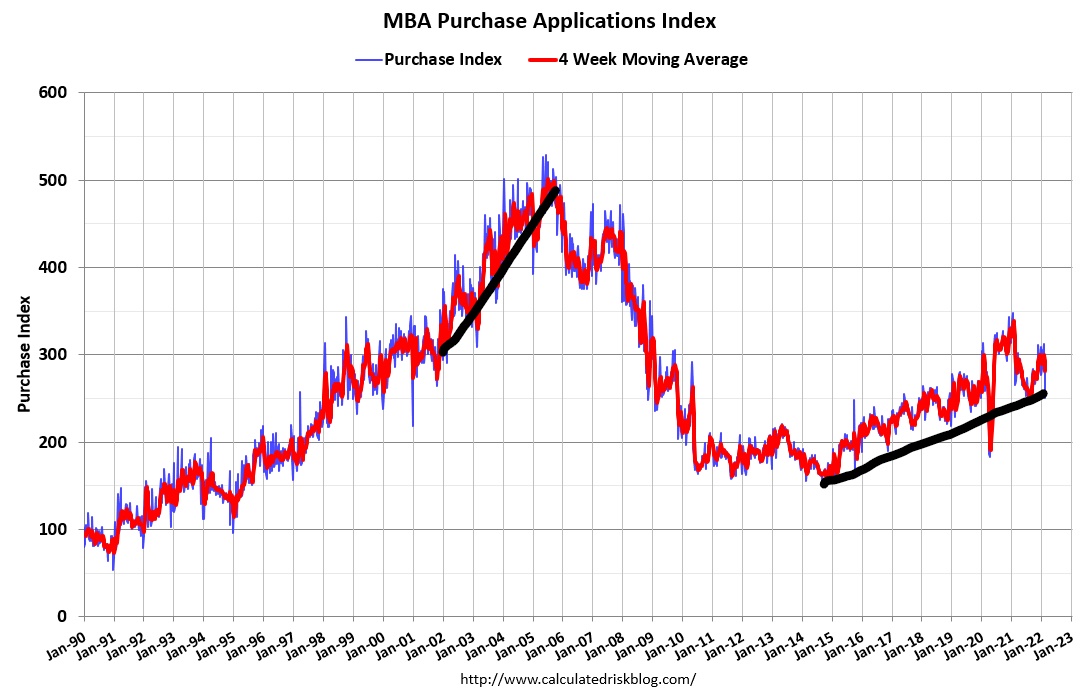

The MBA purchase application data from 2002-2005 is much different than what we have seen from 2018-2022. If we had a FOMO housing market with emotional buying, the credit demand would look much more robust than what we have seen. It hasn’t for a reason; that was always a marketing pitch.

Now for the bad and unhealthy news of the housing market in 2020-2022, price growth.

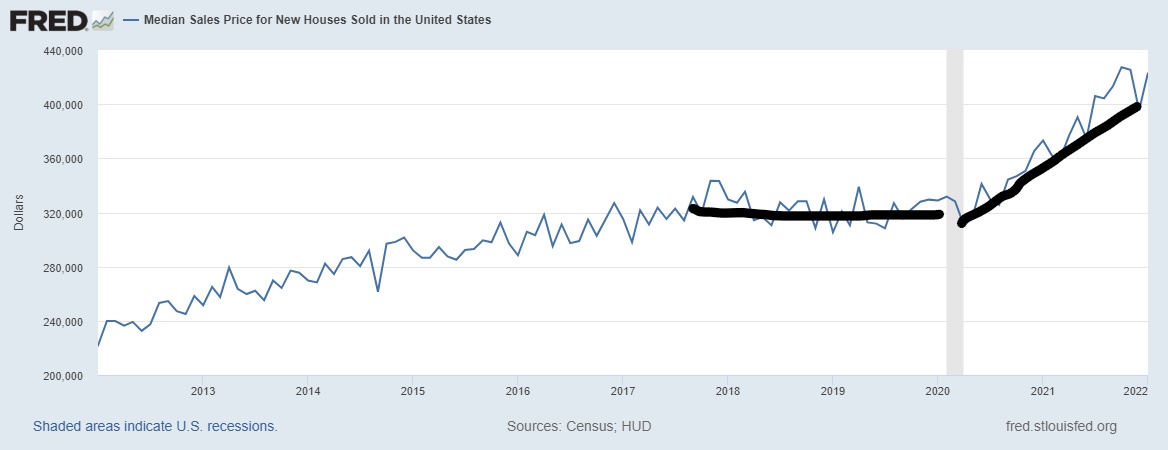

From Census: The median sales price of new houses sold in January 2022 was $423,300. The average sales price was $496,900.

As you can see below, new home prices have taken off much like the existing home sales market. During these last two years, I have tried my best to warn people that we should have always worried about home prices accelerating, even creating the term forbearance crash bros in the summer of 2020 to make it a bit fun. However, it feels like people didn’t want to believe the 2020 housing rebound or the scorching home-price growth in 2021. We need a cool down, folks; this is not a good thing.

The positive aspect of this report was the revisions which drew down monthly supply data on a three-month average noticeably. However, we don’t see a big booming sales market, so housing construction will have limits unless new home sales start to pick up. Know that the builders are always mindful of higher mortgage rates, and they keep an eye out on the cancelation data.

So far, nothing too dramatic is happening on the housing front; that could change if the 10-year yield can create a range with a duration from 1.94% – 2.42%. As I write this, the 10-year yield is currently at 1.94%. Right now we have a lot of geopolitical news moving the 10-year yield. Hopefully, that ends soon and then the real interesting story with the bond market will be whether slower economies in the U.S. and around the world drag bond yields lower or whether economic data stay firm to send yields higher.

If they do go higher, we need to be mindful of how it impacts new home sales and housing starts data as it has done in the past.