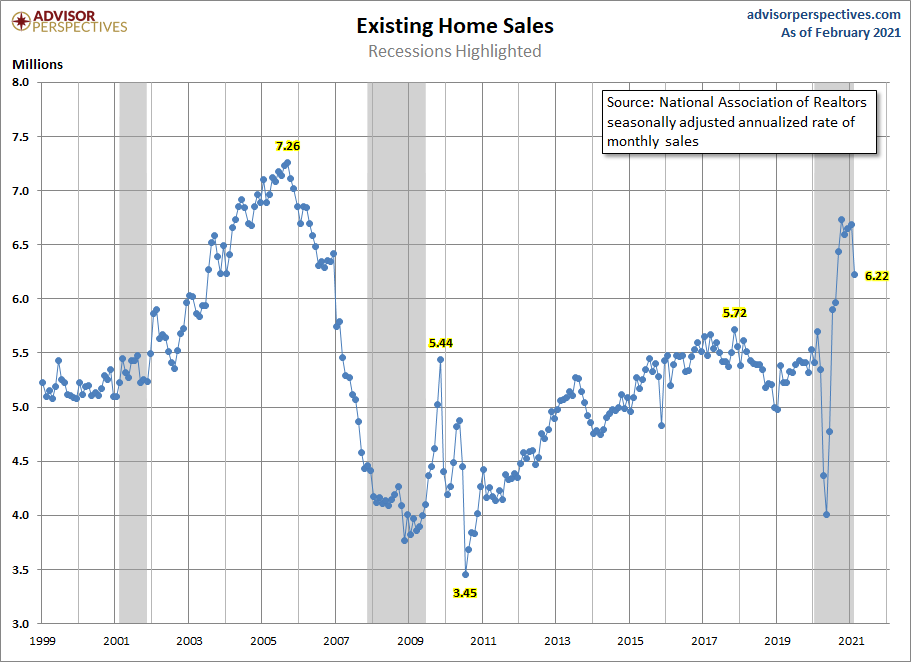

According to The National Association of Realtors, February’s existing home sales missed estimates, coming in at 6.2 million.

Because February 2020 sales were strong, the year-over-year growth in sales for February 2021 is impressive at 9.1%. For the housing market, the COVID crisis started in earnest in March of 2020. The data for February 2020 showed that the housing market was set to outperform all other sectors. Of course, when we got the February 2020 report, even though sales were robust, the country was in full crisis mode, so the report was ignored. At that point, we were too busy buying hand sanitizer and hoarding toilet paper to notice this good news.

This current NAR report also shows that the median sales price jumped 15.8% year over year. Yikes! You may recall I warned that this could happen during the years 2020-2024.

Because home prices are growing so fast, I consider this the unhealthiest housing market since after the housing bubble years. The market is not healthy when buyers and even some sellers who want to sell then buy again, can’t close a deal because supply is too low and demand is too hot so they are constantly outbid. This is what happens when you have the best housing demographic patch ever recorded in history run alongside the lowest mortgage rates ever recorded in history.

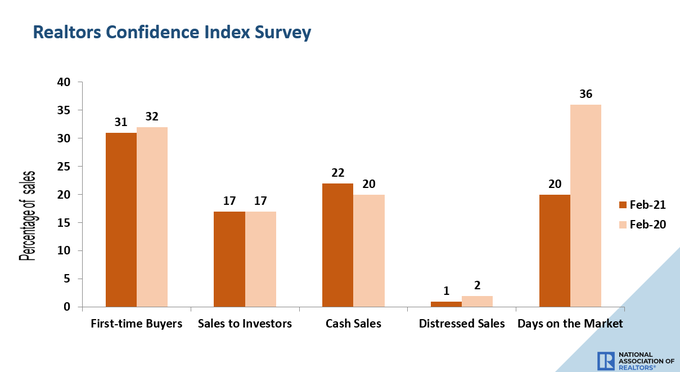

At some point in the future (hopefully), higher mortgage rates will cool down home-price growth and extend the days on the market. We are still at 20 days on the market, down from 36 days on the market we had last year.

I have talked for many months that existing home sales data should get back to 6.2 million and lower. The current report is getting us back there – we are just seeing sales revert back to trend.

Considering our current economic condition, the U.S. existing home sales market should have a monthly sales print between 5,840,000 and 6,200,000. If sales go above 6.2 million, then the housing market will have done better than I expected. In fact, so far the market is doing better than I expected for 2021. As I stated earlier, higher mortgage rates should cool down the market, but the question remains: How high do rates have to go to halt price growth and increase days on the market? I went into this topic in more detail in a recent Housing Wire interview.

Currently, the 10-year yield is 1.68%. This is great news because it shows the bond market believes that America is back. With the 10-year yield in the range of 1.33% to 1.60%, I believe that we have passed the final milestone for the “America is Back” economic model that I proposed last year. Presently, mortgage rates are rising as they should be because they were abnormally low due to COVID-19. The pandemic was a health crisis first, but became an economic crisis largely due to fear and shutdowns of certain economic sectors.

If COVID had not hit our shores (coulda, woulda, shoulda), our economy would still be continuing the longest economic expansion ever. We are just getting back to a normal (pre-COVID) range on the 10-year yield and rates. In time, we should see higher rates create some balance in the U.S. housing market.

The 10-year yield as of the close last week at 1.74%, currently at 1.68% — and although this is high compared to yields in the past year, bond yields are still low historically speaking.

My guess is that mortgage rates above 3.75% may be enough to slow home-price growth. I wrote last year that we should watch housing data closely when the 10-year yields get above 1.94%, assuming this facilitates rates above 3.75%

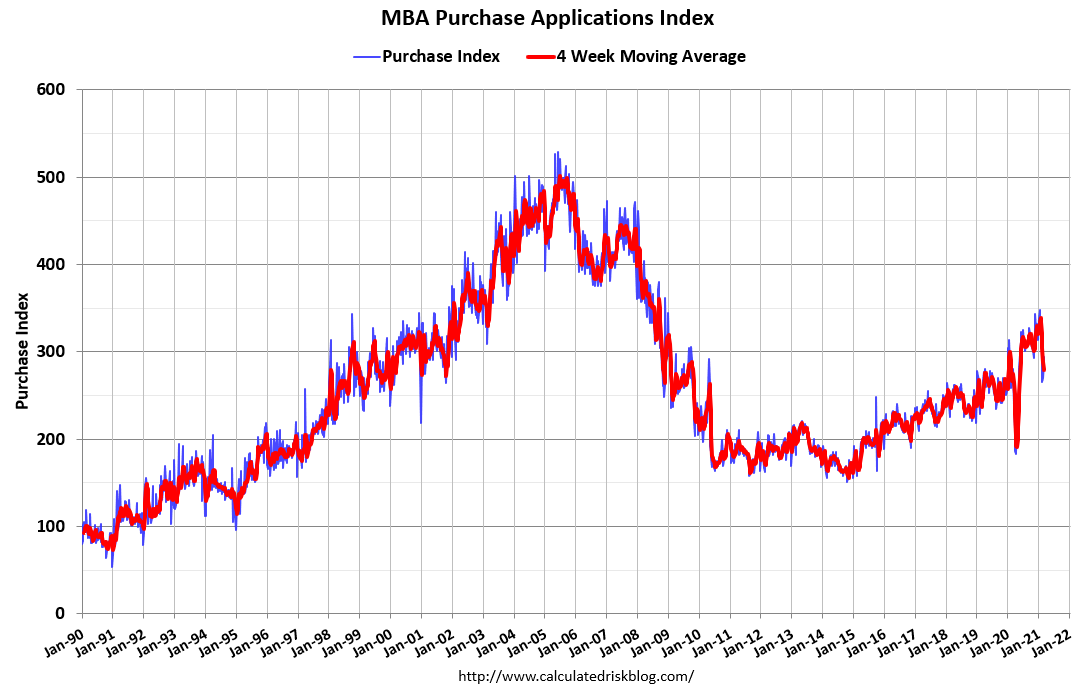

So far this year, the MBA purchase application data is a tad stronger than I expected. This metric predicts the trend in demand 30-90 days out. I believed the peak rate of growth in purchase applications would be around 11% year over year up until March 18. Currently, purchase applications are trending at 9.72% year over year, so we are off to a good start for 2021.

Remember though, that the year-over-year comparisons for at least the next nine weeks of 2021 are going to be somewhat pointless because last year’s data, due to COVID-19, were so low. After the next nine weeks, we should see negative year-over-year data for most of the rest of the year — especially after June, which was when we started to get parabolic rebounds in the housing data last year.

The last four weeks of purchase applications showed year-over-year growth of 5%, 2% 1%, and 7%. This is what I was looking for in 2021 before the low comps. We did have a lot of weeks showing 15% to 17% year-over-year growth. I attribute this to the make-up demand from the shut-downs last year. Existing home sales never got back to the 5,710,000 to 5,840,000 in total sales we expected for 2020, suggesting that some demand was delayed to 2021. Instead, 2020 total sales ended at 5,640,000.

New home sales, existing home sales, and the builder’s confidence index all went parabolic towards the end of 2020. These metrics have since stopped going up and started to fall. The last report on housing starts shows that this metric fell as well. These declines are normal and what we should expect after the parabolic rise in demand last year. So although the data looks funky to the casual observer, we can suss out from the data the real trend is in sales.

Existing home sales should get back to 6.2 million or lower. Any monthly prints above 6.2 million should be considered a beat, like this report.

When I look at today’s report, the most significant data point to my mind is the 9.1% year-over-year growth in existing sales. This is the best February sales data we have had in a long time, and it’s working from a high comp. This shows me that, despite what you may hear to the contrary, homes were on the market to buy and they were bought! But as inventory and days on the market decline, the housing market is getting unhealthier.

From the NAR:

Only higher rates will result in more days on the market and thus larger inventory. We need these two things in order for buyers to have more choices and more reasonable price growth. Again, the question remains if rates will get high enough to have this effect on the market before more price damage is done. Right now home prices aren’t high enough to impact demand in a major way. Demand is still hot as buyers are regularly getting outbid by other buyers with more cash or better income financials. Here is hoping for a balanced housing market instead of our current super-hot one.

Joyful to follow your data. Thank you.