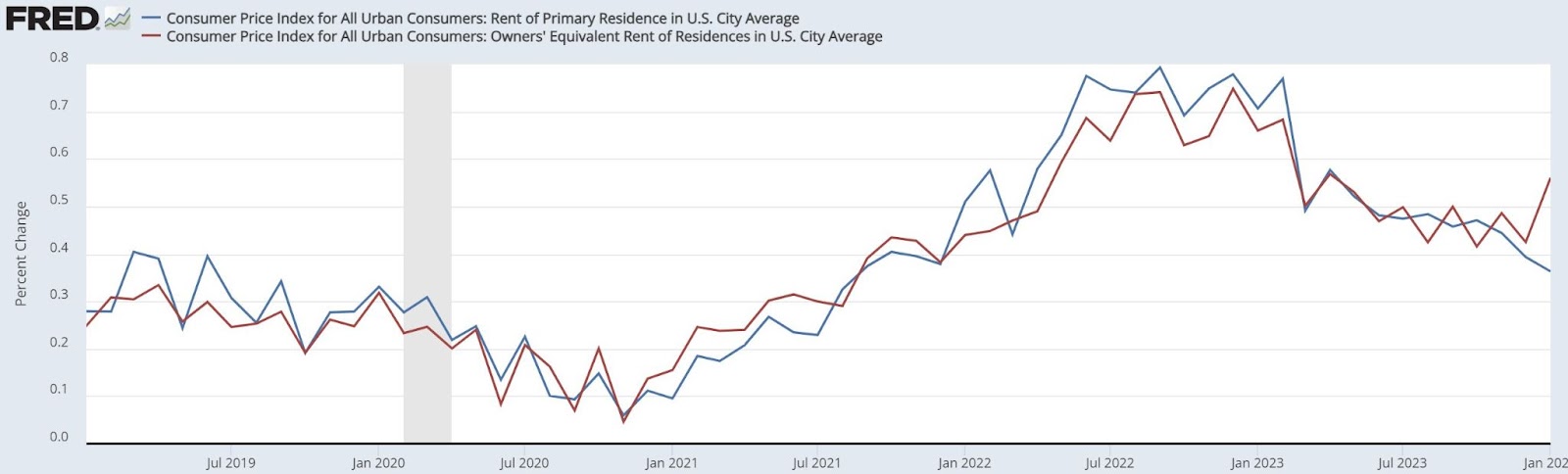

Today’s CPI inflation report was the craziest inflation report I have ever seen in my life. The progress in inflation is still intact as we have fallen so much from last year’s growth rate, but the Owners’ Equivalent Rent of Residences (OER) inflation has diverged from all the shelter rent data in the most prominent fashion I have ever seen, which boosted this report higher than it should have been.

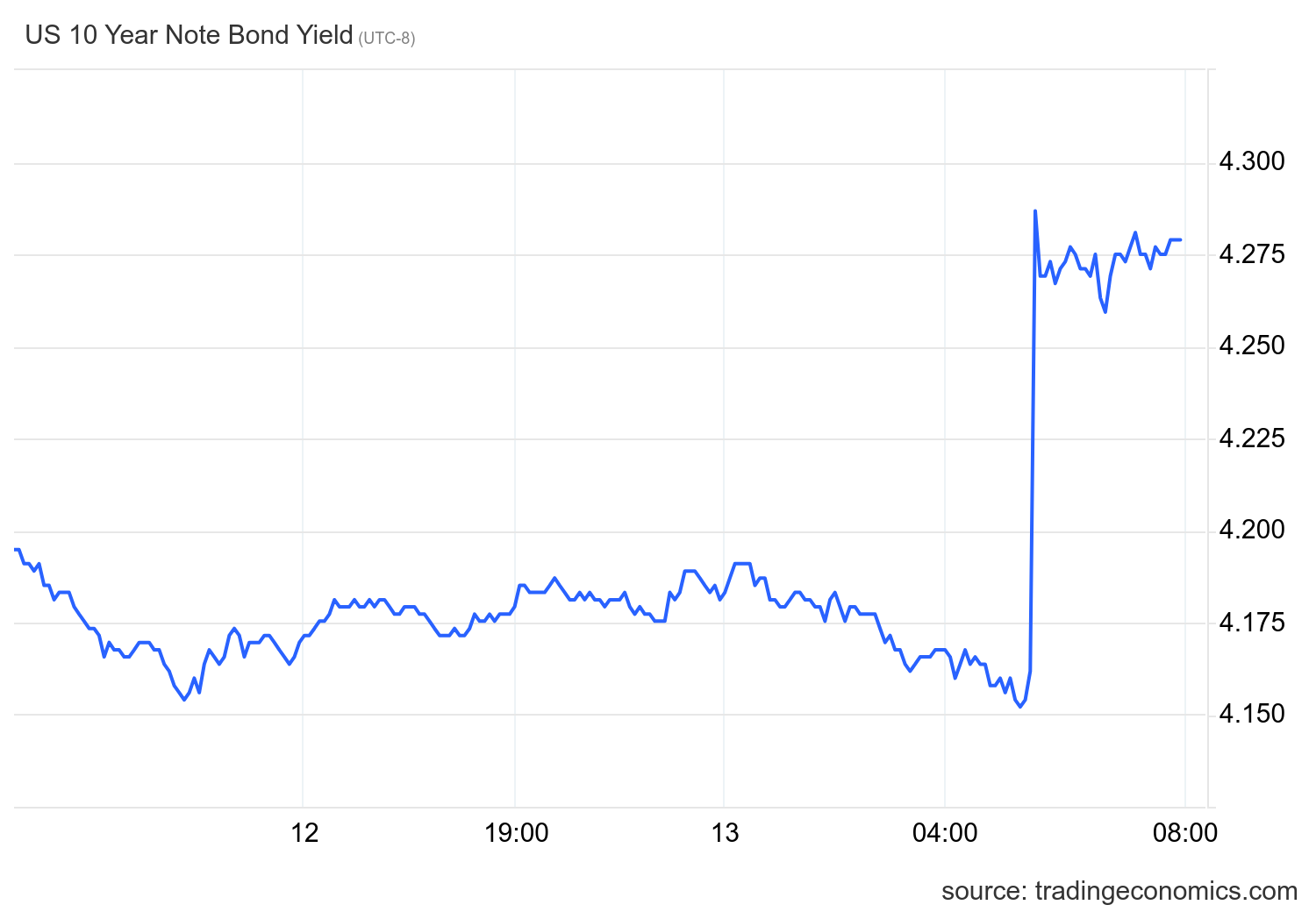

Bond traders were not ready for this, and the 10-year yield shot up higher, along with mortgage rates. As of this second, we are three basis points above my peak 2024 yield forecast call of 4.25%.

I have been tracking data for a long time and have never seen a divergence in the report like I see today. We all know the shelter rent lag in the data, but this is different — this is a straightforward one-month adjustment issue as the breakaway from OER is massive compared to the Rent of Primary Residence in the U.S. city average.

On Monday’s HousingWire Daily podcast I asked the question of which we will see first: 8% mortgage rates or 6% mortgage rates? I firmly believe that the Fed hasn’t pivoted. I believe the Fed has a COVID-19 housing economic policy to ensure that housing stays depressed because of the fear of a return to the 1970s, which had a housing boom, for those who don’t remember.

From the CPI report: The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.3 percent in January on a seasonally adjusted basis, after rising 0.2 percent in December, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all-items index increased 3.1 percent before seasonal adjustment.

Of course, the Federal Reserve focuses on core inflation, and even with the inflated shelter index, we have made a good progress on core Inflation year-over-year.

Even the shelter inflation index — the biggest driver of core Inflation as it is 44% of the CPI index — is slowly heading in the right direction. I believe everyone understands that this CPI report looks a bit fishy, but bond traders don’t care; they were not prepared for this, so they sell first and send yields and mortgage rates higher. The question is: Does the Fed know enough to see what is wrong in this report? That is a good question.

On a year-over-year basis, the OER inflation data is making progress, but it’s lagging the reality of the current data. Mind that when I talk about rent disinflation, the big push is apartments. Single-family rents are stabilizing and holding up well. However, apartments are having pricing issues, meaning more supply is coming online, which will halt production of many more apartments until the supply and demand equilibrium can stabilize to where it makes sense to spend money to build more apartments.

What does this mean for mortgage rates? Well, they’re going up today, and if bond traders feel the itch to start shorting the bond market again and push yields higher as they did last year, this again puts more pressure on the housing market, which is already in the third year of great recession lows in demand.

The one thing that is positive now is that when the 10-year yield headed toward 5% and mortgage rates were at 8%, the Fed called this a very restrictive policy, meaning that it wasn’t their intent to have yields this high. Now that PCE inflation is running below 2% on the three and six-month data pool, we shall see if they hold to that view since inflation is much lower in 2024 than in 2023.

However, as you can see, I don’t like playing with fire when you don’t need to risk being burned. Since the Fed hasn’t pivoted, they’re playing with fire when they don’t need to. I may be one of the last people on the planet who believes the Fed hasn’t pivoted, but today shows why I have taken that view.

Again, the progress in inflation is here, but as I have believed for a long time, the labor market is the key to mortgage rates, bond yields and the Fed’s actions. If jobless claims were running at 300,000, today’s data wouldn’t matter and the 10-year yield would have already been lower. Remember, when it comes to rock, paper, scissors, labor always beats inflation, and it’s all about jobless claims data.