Given the hotter inflation reported in Tuesday’s CPI data, can mortgage rates go above the 2022 peak of 7.37%? Initially the 10-year yield fell after the report, then rose higher, only to fall back down again. For all the hype around today’s stock market close, it was a dud of a Valentine’s date if you ask me.

A lot of times, on days when big economic reports are released, you can get wild intraday action but not have much happening by the end of the day. We still have a lot of big housing market economic reports this week, so stay tuned as retail sales, builders confidence, purchase apps, jobless claims, producer price inflation, and leading economic indicators data are still to come.

2023 bond and mortgage rate forecast

When I do my mortgage rate forecasting for each year, I don’t target mortgage rates but where I believe the 10-year yield channel will be with a set of variables in play. Of course, post-COVID-19, we have had extreme variables that can crazily move the market.

However, for 2023 I believe this range on the 10-year yield would be appropriate, considering the labor market is still solid. If the labor market starts to get worse — meaning jobless claims rise with some speed — the initial range of this forecast will break, and bond yields will go lower. The data isn’t there yet to even have that conversation.

From my 2023 housing market forecast: “For 2023, the 10-year yield is currently at 3.70% and I believe the 10-year yield range this year will be between 3.21%-4.25% as long as the economy stays firm. Now if the economy gets weaker, especially in terms of the labor market breaking, which for me is jobless claims rising to 323,000 and beyond, then we can get as low as 2.73% on the 10-year yield.

“With that 10-year yield range (3.21%-4.25%), mortgage rates should be between 5.25%-7.25%. This assumes that the spreads are wide and pricing for mortgages is still weak. However, if the spreads get better, we could even see mortgage rates under 5% if the 10-year yield breaks under 3%.”

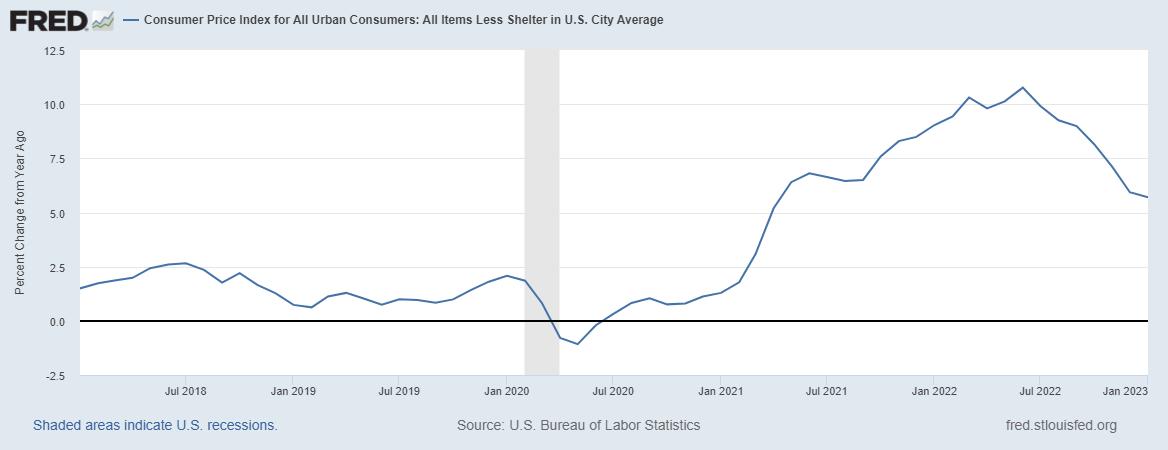

What do we know about inflation? The growth rate is cooling from last year’s peak, and the shelter inflation portion of housing will cool down over time. It’s widely known that the CPI inflation shelter data lags a lot, and since it’s the most significant component of core inflation, it’s a big deal.

This is why I went on CNBC last year to say the growth rate of rents falling was a positive for inflation for 2023. However, the CPI data lags badly on this reality, and the fear was that the Federal Reserve didn’t understand this.

However, then the Federal Reserve actually created a new index that excludes shelter to adapt to the more current data, which shows the growth rate of rents is cooling down. Now the Fed focuses on core inflation data, excluding food and energy. However, even if I take shelter away and leave food and energy inflation in the equation, the growth rate of inflation is cooling more noticeably.

Without rent inflation taking off, you can kiss the 1970s inflation comparisons goodbye, and this is why the 10-year yield never broke above 5.25% — a critical level for me to even have a thought about 1970s-style inflation. As you can see below, the growth rate of rents took off a few times back then. After the 1970s, the growth rate was stable for decades.

My mindset with inflation data since October of 2022 has been to give it time: 12 months from now, we will be in a better place. If the economy went into a job-loss recession, the bond market would get well ahead of the Fed and mortgage rates would fall faster. However, we aren’t there yet.

The Fed pivot won’t happen until jobless claims break over 323,000 on the four-week moving average, but the truth is the bond market isn’t old and slow; they will head that way before the Fed does.

CPI report

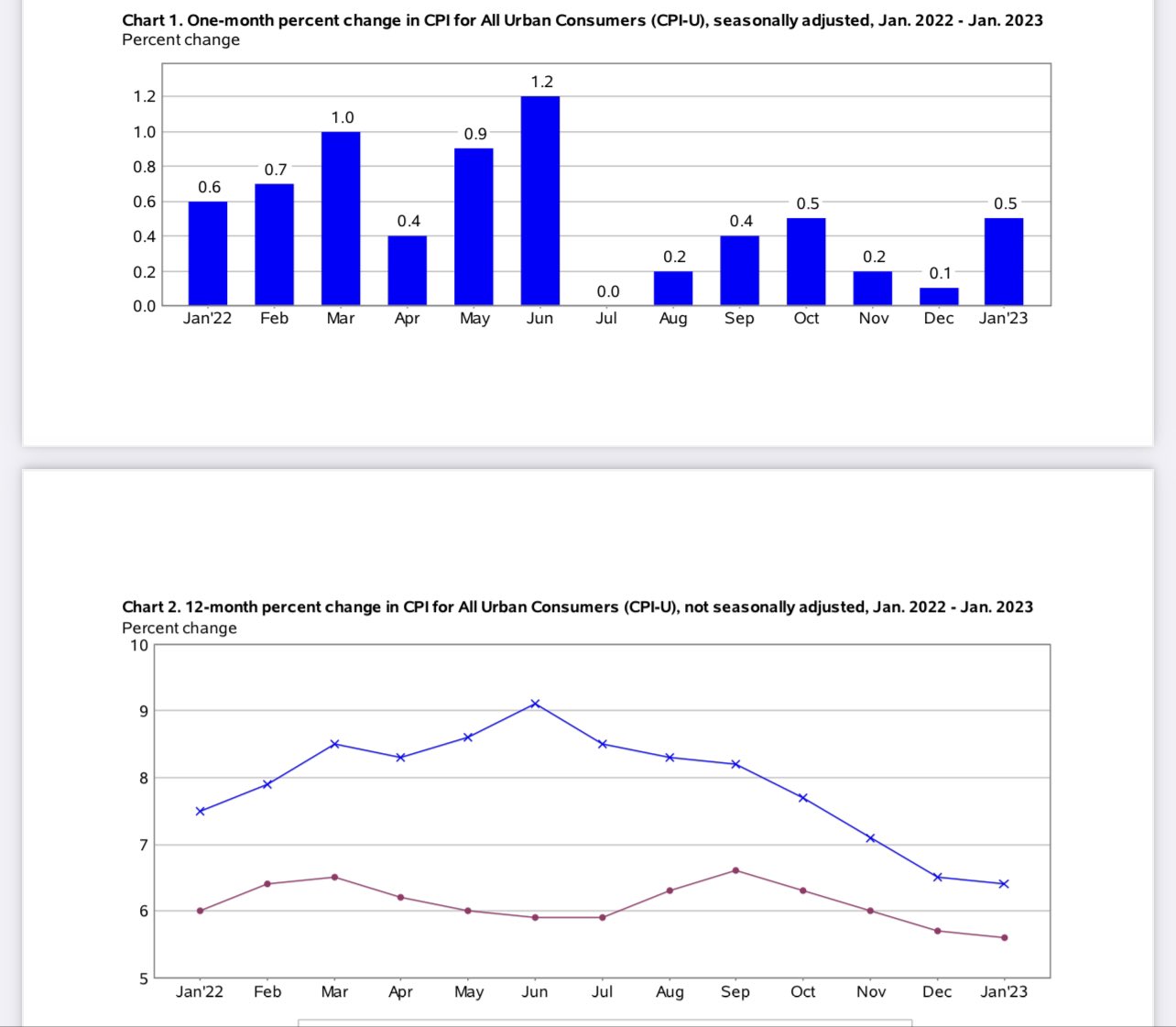

From BLS [bolding is mine]: “The Consumer Price Index for All Urban Consumers (CPI-U) rose 0.5 percent in January on a seasonally adjusted basis, after increasing 0.1 percent in December, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 6.4 percent before seasonal adjustment. The index for shelter was by far the largest contributor to the monthly all items increase, accounting for nearly half of the monthly all items increase, with the indexes for food, gasoline, and natural gas also contributing.”

As we can see below, the growth rate of inflation is cooling, but shelter inflation, “Which is lagging real-time data,” is keeping the core data higher than it should be today. Remember, you should always focus 12 months out with inflation data and tie it to the weekly economic data. This is why we created the weekly Housing Market Tracker.

Other rental inflation data shows a cool-down, common with global pandemics. However, not only is the real-time data cooling, we have nearly 1 million apartments that will be built in the near future, and the best way to deal with inflation is always more supply.

Hopefully, this explanation of my forecast for 2023, including the 10-year yield, mortgage rates, and inflation gives you a better understanding of why I don’t believe mortgage rates can rise above last year’s peak of 7.37%.

Now, one way mortgage rates could blow past 7.37% is if the economy starts to boom again, supply doesn’t grow, and wage growth, which has been cooling, reverses, and explodes higher again.

If rents and wages took off higher again, some new war created more of a supply shock, and the labor market got even tighter, this would counter my discussion that the growth rate of inflation has peaked. However, so far, it doesn’t look like anything I just talked about is happening, so give it more time, and the inflation growth rate will moderate.