I’ve been hearing some chatter lately that the uptick in home buying that started in February of 2020 (before COVID, by the way) and has continued into 2021 is being substantially driven by a national emotional state of fear of missing out (FOMO). Now, I understand emotional eating (me, plus Halloween, plus a big bowl of Reese’s Peanut Butter Cups for instance) and even emotional buying (still whittling down hand sanitizers).

Still, emotional home buying seems like a stretch. Nevertheless, some supposedly erudite thinkers on the housing market are saying this, so I thought I should investigate.

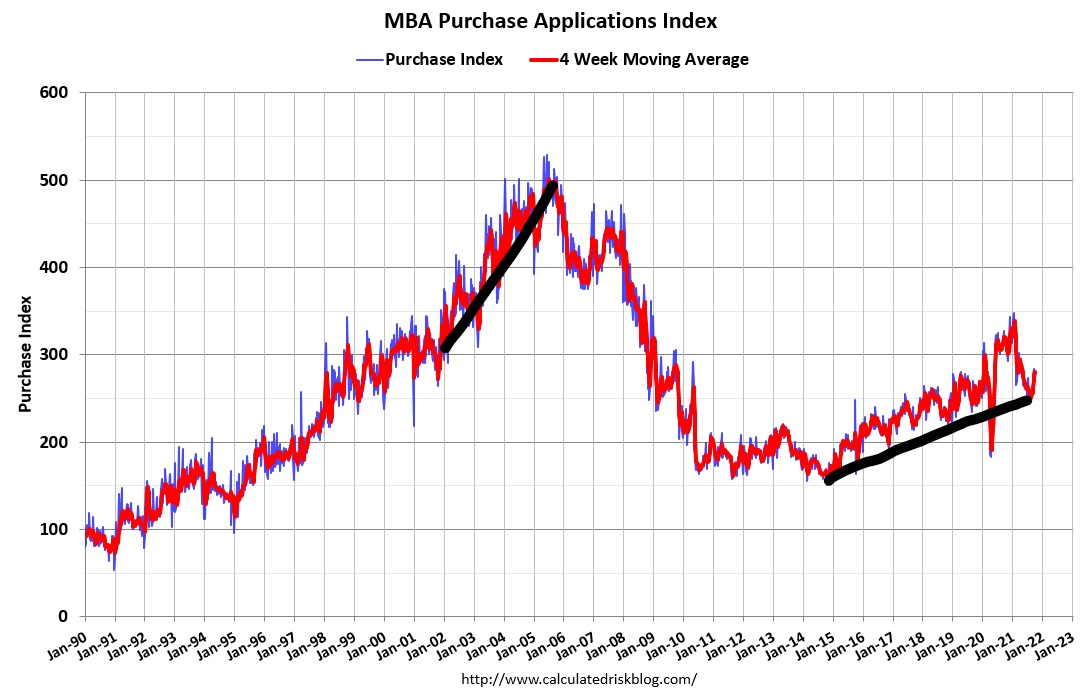

If the housing market was in the grips of some mass hysteria of irrational purchasing, we would expect to see certain hallmarks in the data. First, purchase applications in the data should be skyrocketing as they did during the 2002-2005 ill-considered, home-buying extravaganza. The data shows a positive growth trend since the lows in 2014, but looking at the two trajectories, there is no comparison. Considering population growth and the current more favorable demographics for home buying, I would say purchase applications are precisely where we would expect them to be, sans nationwide hysteria.

Based on favorable demographics during 2020-2024, I forecast that purchase application data would get to the 300 level. We reached this in the early part of 2020. I also predict that housing starts will finally start a year at 1.5 million during this period. That has not happened yet. So yes, we have seen positive growth, but not irrational growth.

The credit market supports this case for moderate, rational growth. At the same time, it is true that we have had more Americans purchasing homes with mortgages in 2020 and 2021 than any single year from 2008-2019. But I wouldn’t call the recent growth a credit FOMO boom.

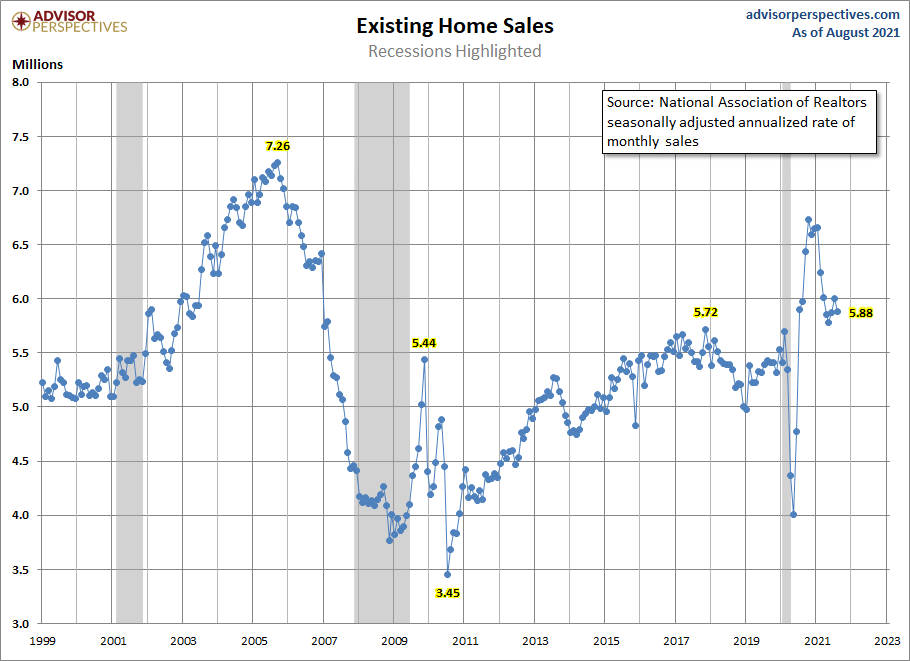

Our demographics are providing the market with built-in replacement demand, not a credit or sales boom. In the years 2020 to 2024, total home sales should be 6.2 million and over. If sales surpass 6.2 million, I would consider that a beat. This couldn’t have happened in the years 2008 to 2019 because the bulk of Americans were either too young or too old for home buying. So far in 2021, sales trends look normal to me, maybe just a tad better if we don’t see any more existing home sales prints under 5,840,000.

As I wrote here: “The rule of thumb I am using for 2021 is that existing home sales, if they’re doing good, should be trending between 5,840,000-6,200,000. This, to me, would be considered a good year for housing.”

It’s not irrational FOMO buying or emotional COVID pandemic buying – it’s just normal Americans needing shelter and buying homes. Because the uptick in the number of buyers is happening during a period of record low inventory, prices have surged to an unhealthy level. Trust me, I am rooting for more inventory than anyone else, as 2022 has some housing risks.

The only way I believed we could go under 6.2 million total home sales during the yeas 2020-2024 is if home prices rise beyond my five-year cumulative growth model of 23% and mortgage rates rise. This wouldn’t crash the market by any means, but making 6.2 million in sales would be in jeopardy.

Home prices have gone up by more than 23% in year two of this five-year growth period, but rates are still low — nowhere near the 3.75% and higher level that would impact demand. Remember, I am talking about a rate of growth slowing, not crashing, if the 10-year yield can get over 1.94%, which wasn’t my forecast for 2021. Certainly not a mortgage rate that would crash home sales and demand that would warrant a housing is oversupplied by 20% in 2022.

I mention this thesis that the market is oversupplied by 20% because Ivy Zelman of Zelman & Associates, one of those aforementioned housing market scholars, recently proposed this, which confused many people. How does one reconcile what we know to be true about the current market — that home prices have deviated upward from historical norms and inventory is at all-time lows — with a thesis that the market is significantly over-supplied? How can this be?

Let’s take a look at what was said in this interview with Sara Eisen on CNBC on Friday (Oct. 15, 2021) to see if we can parse this.

When asked if housing is still hot, Zelman said, “…We are overbuilding in single-family by 20% to normalize household demand… and because of all the investors in the marketplace including second homeowners, it’s clouded by dual ownership as well as institutional capital that is coming into the marketplace.”

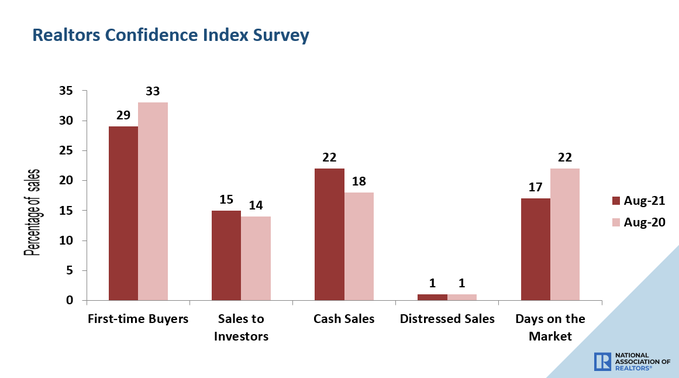

Sales to investors increased by 1% year over year in the previously existing home sales report. Not much FOMO action here.

As I have said previously, there is no Wall Street moat around housing. Second-home purchases increased recently, but this isn’t the primary driver of housing. A better premise would be to calculate how much demand would be lost if cash buyers, second-home buyers and investors went back to trend with the rise of mortgage buyers. This is why I keep my 6.2 million total home sales level as my key marker; it considers a lot of variables.

More Americans are buying homes with mortgages in 2020 and 2021; that is the primary driver in the housing market. When mortgage demand fades, so will housing. Millions of Americans buy homes every year. Post-1996, it’s scarce to have home sales under 4 million, so our numbers today don’t reflect FOMO as much as American citizens needing shelter.

Zelman also stated that “the housing market is already showing some moderation.” With this, I can agree. Moderation of housing data has been a big theme since the summer of 2020. The make-up demand that surged following the COVID shutdowns did a number on many of our housing metrics. We saw V-shaped recovery and make-up demand surge sales data to unsustainable levels. I’ve stressed repeatedly that the data will moderate, but it will find a base to work from.

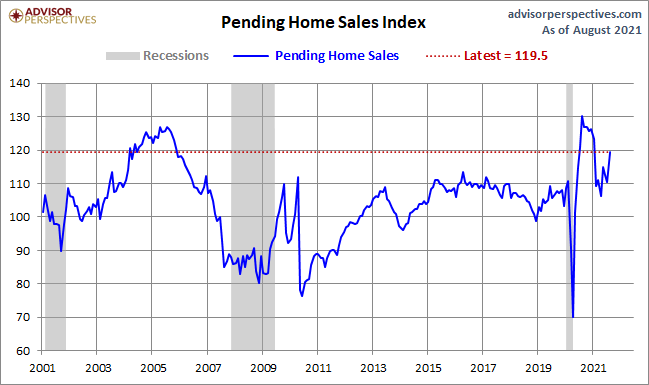

If anything looks normal to me, the recent pending home sales data, existing home sales data, and purchase application data, maybe possibly be better than expected in 2021 than I thought it would be. The sales range is on target, but I had anticipated more than one print under 5,840,000, and we don’t have many 2021 home sales reports left.

Zelman also said, “home price growth isn’t sustainable.” I’m hoping she is right. I keep saying that this is the unhealthiest housing market post-2010 because days on the market are too low. She said when mortgage rates get to 4%, housing prices will cool down. If you follow my work, you know that my line in the sand to cool demand is 3.75% and higher — so not too different from Zelman’s estimate.

My estimate is based on what we saw in the previous cycle. In 2013 and 2014, when mortgage rates rose, it did slow down home purchasing. The rate of growth of home prices was more substantial than normal in 2013, and once the 10-year started to head toward 3%, the rate of growth of prices cooled down. It didn’t go negative, but was a definite cooling. If this happens in 2022 and 2023, it would be the best thing for the housing market.

To her credit, Zelman didn’t say housing would crash if rates went to 4%, but to back up that number, it would help to give folks a total sales estimate for when that happens. When Eisen asked Zelman how much housing would fall, she didn’t answer the question, but talked about how population growth is falling. Without an estimate, there is no way to back-test her forecast or get an idea of how much damage to total home sales she might be looking for.

It is also noteworthy that she is not shorting the builders but staying on the sidelines, which I have no problem with. I had assumed that she was short the builders with the 20% over-supply premise, but staying on the sidelines sounds prudent.

Then again, stock investing and economics are two different worlds, and most folks are not made of the stuff to exist in both. Understanding the microcosm of one stock or even one sector is entirely different from understanding the planetary moves of economics. I love stocks; I was able to retire on my stock returns from March 2020 with a two-year verified return of 1,497.91% from Oct. 18, 2019, to Oct. 15, 2021. The 2021 year to date is a respectable 153.95% return.

I don’t say this just to brag (that’s just the frosting on the cake) but rather to show you that developing economic models that are rigorous enough to justify putting down your money sometimes pays off. For more on this, check out my America Is Back recovery model published April 7, 2020, and this recent podcast going over the recovery model I published on HousingWire in 2020.

My take on Zelman’s 20% oversupplied thesis is that I would have phrased it another way and given people total sales estimates for 2022 to clear up the confusion. I have no issue with her saying that the market would cool down at 4% mortgage rates; 3.75% and higher have been my talking points since the summer of 2020. Also, not being short the builders but being on the sidelines looks pretty prudent to me. Everyone has their economic models and takes, but my thesis on the lack of a housing boom goes way back with housing starts.

My core belief has always been that we won’t ever see a housing construction boom like people want in America. Those familiar with my work on HousingWire and quotes I have given other financial media outlets know I have always stayed consistent with that theme. See here for my article on June 7: Why we cant build our way out of this hot housing market.

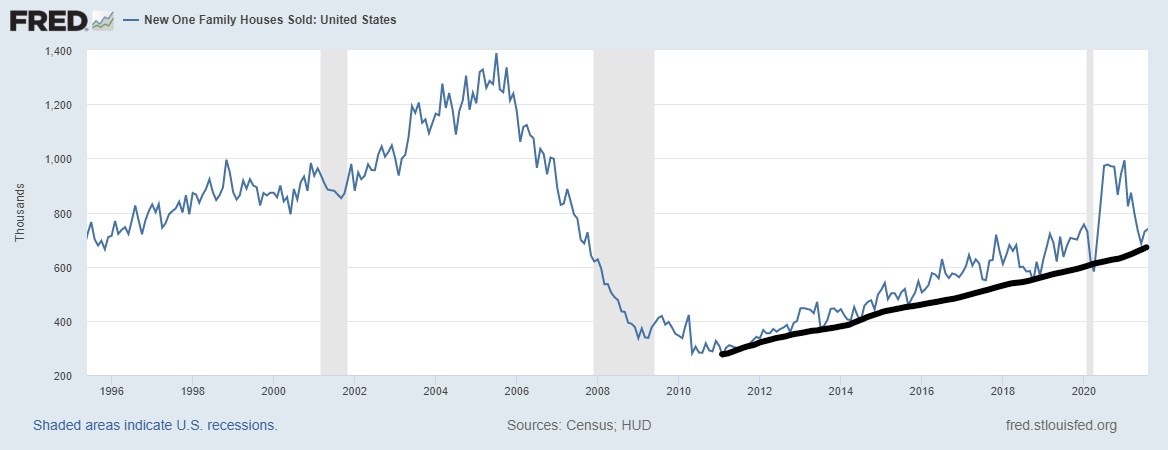

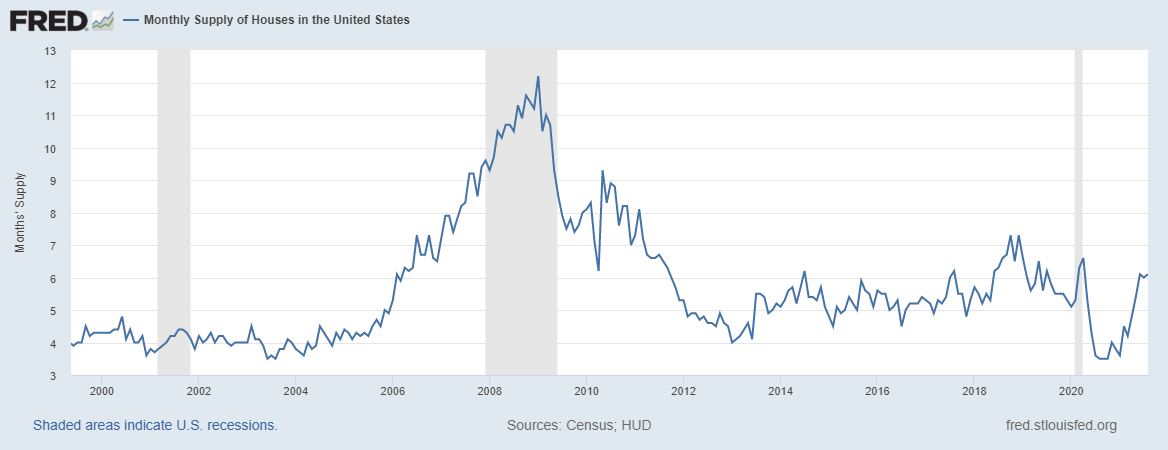

For now, I always give the same advice with the new home sales sector and housing starts. As long as the three-month average monthly supply is below 6.5 months, the builders will build. I would label 4.4 – 6.4 months of supply as just an OK market, nothing great. This is was very common from 2008-2019. Only in 2018 did 5% mortgage rates create a short-term spike with the builders over 6.5 months. Once we can get under 4.3 months of supply, life is great for the builders; they can do what they want.

Trust me, the builders did just that between June of 2020 until March of 2021. They had pricing power and pushed the cost to the consumer because they were willing to pay for it.

Now the builders are mindful of their product, because when rates rose in 2018, they saw a supply spike, their stocks were in a bear market, and one builder CEO said it was the worst quarter since the great financial crisis. Also, we aren’t working from the low bar in new home sales like we had from 2008-2019.

The builders had a great market for a short period. While monthly supply is stabilizing recently, it is still just showing an OK marketplace.

Regarding FOMO, I would say the only economic data that looks like FOMO that can’t be sustained is the retail sales — that data line is on fire on nominal terms.

In short, we don’t have a crazy FOMO booming housing market, we just have solid replacement demand. When mortgage rates rise, if they rise, things will slow down. Nothing that Zelman said is out of bounds. However, like I always stress, when you listen to anyone talking about housing, ask them where they see total home sales going and I believe that answer will always shed light on anyone’s real take on housing.