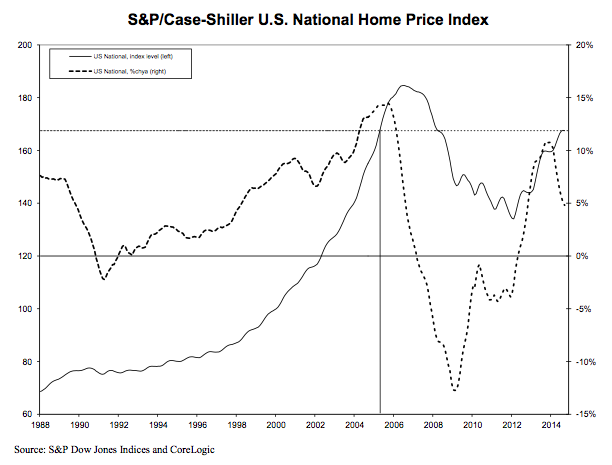

The pace of home price growth continues its downward trend as top cities across the country report a slight decline, the September S&P/Case-Shiller Home Price Indices reported.

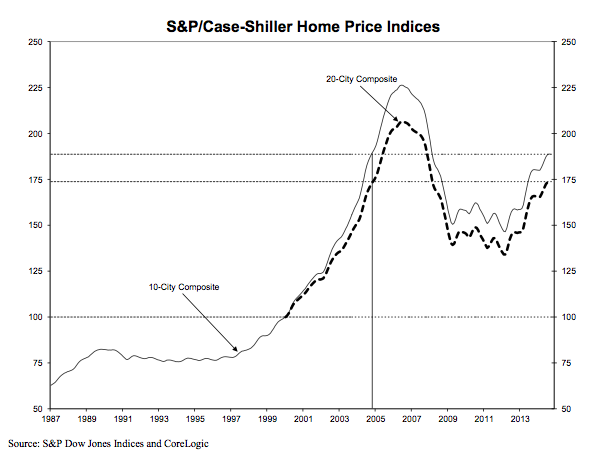

The 10-city composite climbed 4.8% year-over-year, down from 5.5% in August, while the 20-city composite increased 4.9% year-over-year, compared to 5.6% in August.

Both the national and composite Indices were slightly negative in September, with the 10 and 20- city composites reporting a slight downturn while the National Index posted a -0.1% change for the month.

(Source S&P Dow Jones Indices; click to enlarge)

This is the first month-over-month decrease in the national index since November 2013. “The overall trend in home price increases continues to slow down,” said David Blitzer, managing director and chairman of the Index Committee at S&P Dow Jones Indices.

Other regional highlights include the Northeast region reporting its first negative monthly returns since December 2013 and its worst annual returns since December 2012 due to weaknesses in Washington D.C. and Boston.

Meanwhile, the West and Southwest reversed course and are seeing price gains fade after previously being known as strong regions.

This leaves the Southeast as the only region showing any substantial strength, led by Florida with help from Atlanta and Charlotte.

Charlotte and Miami led all cities in September with increases of 0.6%.

However, Atlanta and Washington D.C. offset those gains by reporting decreases of 0.3% and 0.4%.

“No news is good news as home prices continue to stabilize. Most sellers would love to see their home equity continue to jump, but leveling prices provide an opportunity for those looking to enter the market – particularly the millennial generation that has been waiting patiently on the sidelines,” said Quicken Loans Vice President Bill Banfield.

(Source S&P Dow Jones Indices; click to enlarge)

As of September 2014, average home prices for the MSAs within the 10-City and 20-city composites are back to their autumn 2004 levels.

Measured from their June/July 2006 peaks, the peak-to-current decline for both composites is approximately 15-17%. The recovery from the March 2012 lows is 28.8% and 29.6% for the 10-city and 20-city composites.

Charlotte and Dallas were the only two cities to see their annual gains increase while Cleveland remained virtually unchanged for the fourth consecutive month. All other cities saw their annual gains decelerate. Miami continued to lead all cities with a 10.3% year-over-year gain. Detroit saw its gains drop to 5.0% from 6.7% the previous month.

September recorded mixed monthly figures. Nine cities recorded lower monthly figures while nine posted increases. Los Angeles and New York both reported flat monthly changes. Washington D.C. had the largest decrease of all 20 cities at 0.4% month-over-month.

“Like a perfectly prepared Thanksgiving turkey, it’s important for things to cool off a bit in the housing market, because too-fast appreciation risks burning both buyers and sellers,” said Zillow Chief Economist Stan Humphries. “In this more sedate environment, buyers can take more time to find the right deal for them, and sellers can rest assured they won’t be left without a seat at the table when they turn around and become buyers. This slowdown is a critical step on the road back to a normal housing market, and as we approach the end of 2014, the housing market has plenty to be thankful for.”