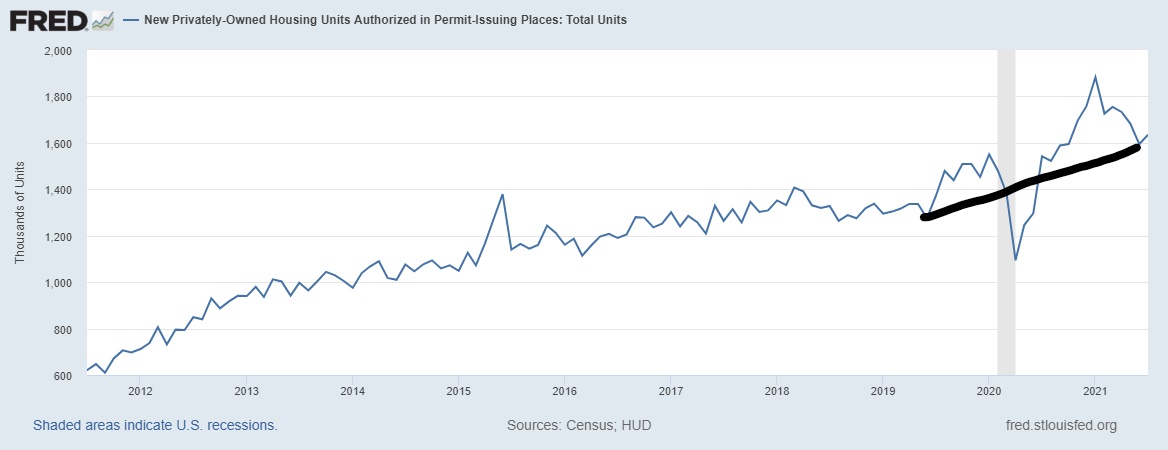

Today, the U.S. Census Bureau reported that housing starts hit 1,534,000 for July, missing estimates. Permits, on the other hand, beat estimates, coming in at a seasonally adjusted rate of 1,635,000. Positive revisions to the previous data were made, but not by very much. This mixed bag of results reflects the typical variability in the data that occurs when not too much has been happening in housing except that monthly supply has been rising for the new home sales market. Homebuilders are navigating their housing stock well to make sure not to give up too much on the margin side of the business in the future.

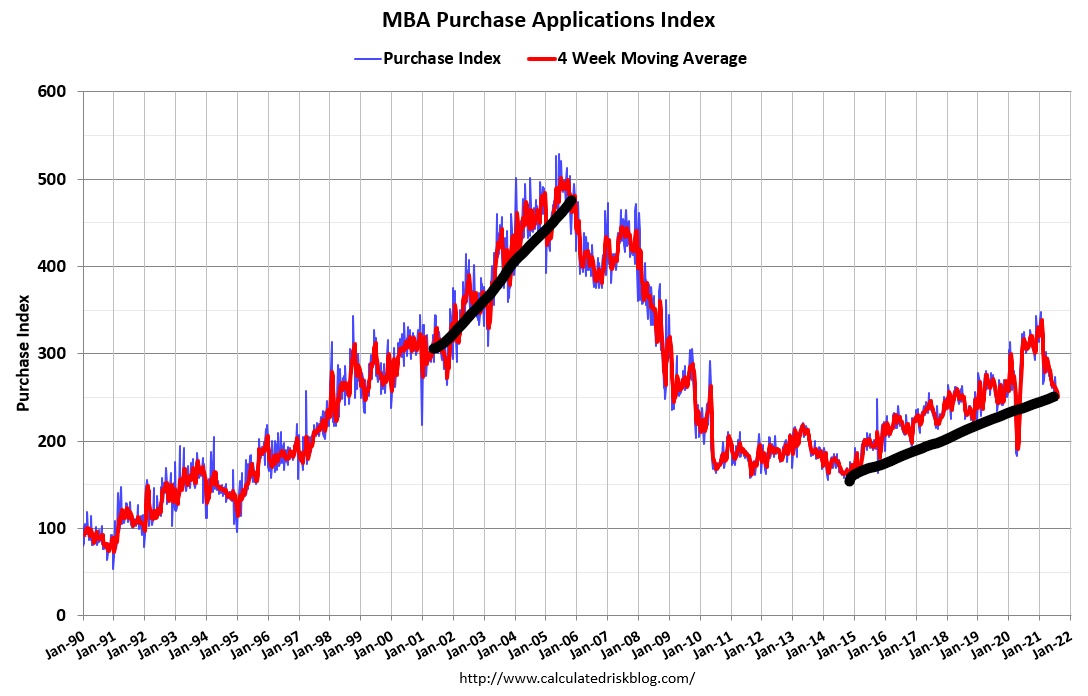

The previous economic expansion from 2008 to 2019 had the weakest housing recovery ever following the bust. I have often said that both purchase applications and housing starts would be limited until we hit the period of favorable housing demographics from 2020 to 2024.

Specifically, I said that purchase applications would not get to 300 in the MBA index until 2020 to 2024. During this period, household formation will create the mortgage demand needed to push applications to that level, and purchase applications did get to this level right before COVID-19 hit in February of 2020.

When considering the future trend for purchase application data, it is best to exclude the COVID-19 makeup demand in the second half of 2020. This rule pretty much holds for all housing data. If you ignore that big move in the second half of 2020, you can see that we currently do not have a credit boom, but rather solid demand from replacement buyers.

This is from the MBA today:

For housing starts, I’ve previously said that starts would not begin a year at 1.5 million until the years 2020 to 2024. This hasn’t happened yet, but we are getting there. Today’s Census report shows that the builders are managing their supply in order to protect their margins.

The builder’s motto may as well be “slow and steady wins the race.” They will never make the mistake of getting greedy and oversupplying the housing market as they did from 2002-2005 when the increased inventory came back to bite them. Lesson learned. In 2018, they got cold water thrown in their face when mortgage rates got to 5% and cooled off demand. The builders’ stocks went down more than 30% from their peaks at that time.

This report confirms that not much is happening in housing outside the unhealthy price gains due to a shortage of homes. This isn’t the sexiest storyline, but it’s the reality for 2021. Housing starts data can make violent moves month-to-month, so it’s best to view the trends while keeping an eye on the monthly supply data for new homes.

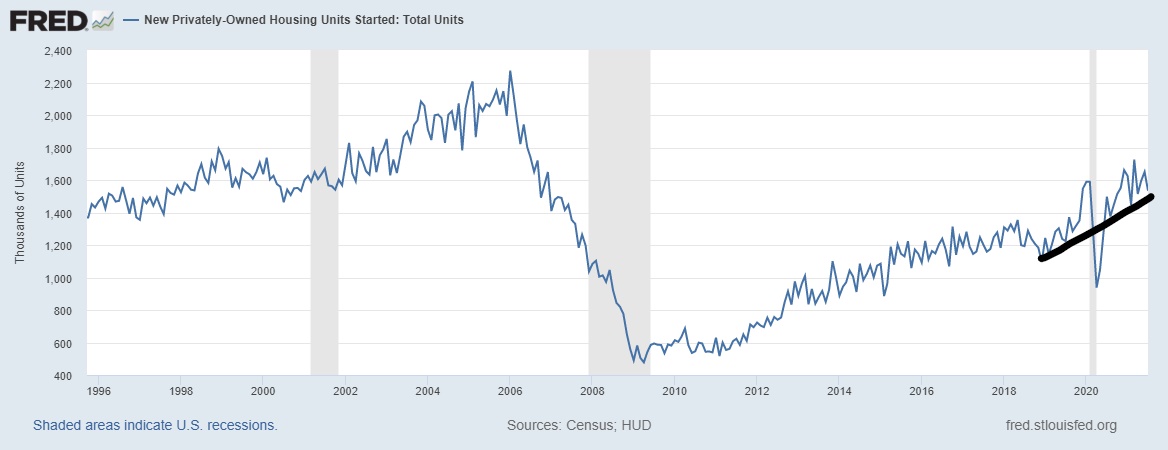

From the Census Bureau: Building Permits: Privately‐owned housing units authorized by building permits in July were at a seasonally adjusted annual rate of 1,635,000. This is 2.6 percent (±0.9 percent) above the revised June rate of 1,594,000 and is 6.0 percent (±0.9 percent) above the July 2020 rate of 1,542,000. Single‐family authorizations in July were at a rate of 1,048,000; this is 1.7 percent (±0.8 percent) below the revised June figure of 1,066,000. Authorizations of units in buildings with five units or more were at a rate of 532,000 in July.

Permits picked up a tad in July, even as a monthly supply for new homes has grown. Moving forward, builders are going to be mindful of their expansion plans, especially considering all the increased costs of hard goods that are needed for a new home. Not much to conclude from this except that demand for housing is above pre-cycle highs.

Housing starts are pushing along with the trend upward that started in 2018. The data shows a slow and steady climb higher with extreme variations in the month-to-month data. Remember ,we need to remove the COVID-19 V-shape data from the trend to anticipate what will happen going forward. That was a historical event due to a pandemic we hope will never be revisited and would never occur in a “normal” economic cycle.

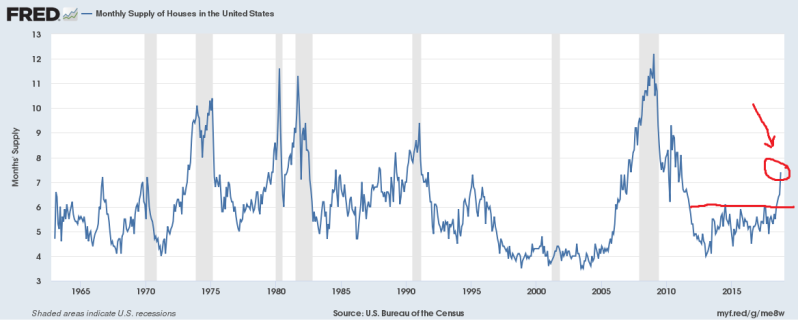

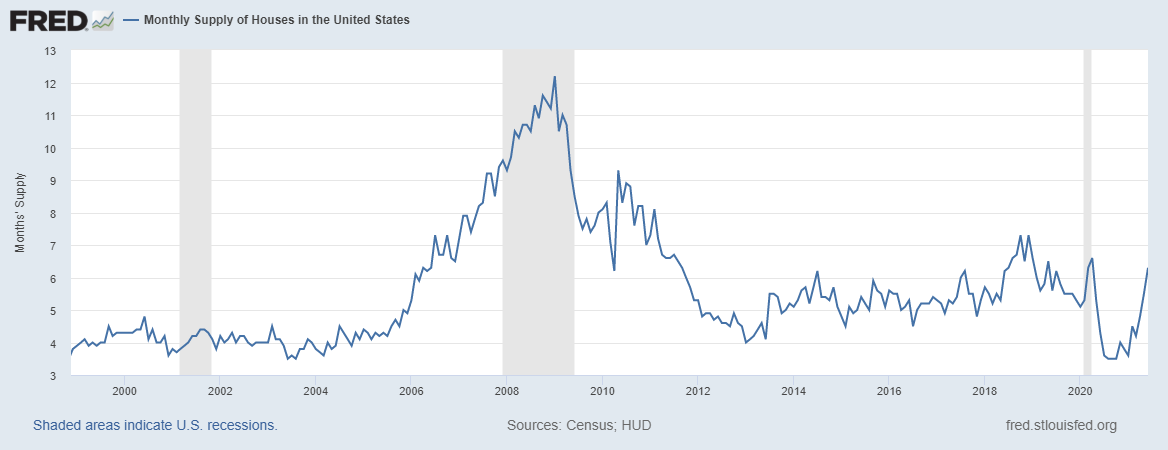

From 2018 to 2019, monthly supply spiked to over 6.5 months following a rise in mortgage rates to 5%. The builders then cooled construction activities to adjust to the hit.

When mortgage rates went lower, demand picked up. Housing starts were roughly flat in 2019, then for the first time following the 2008 bust, new home sales demand grew enough to drive supply below 4.3 months. The inventory level tells builders that new home sales demand is substantial. From 2008 to 2019, inventory never got to that level, but 2020 to 2021 is a different story. Recently, monthly supply has been going up — not because of mortgage rates but because demand has cooled.

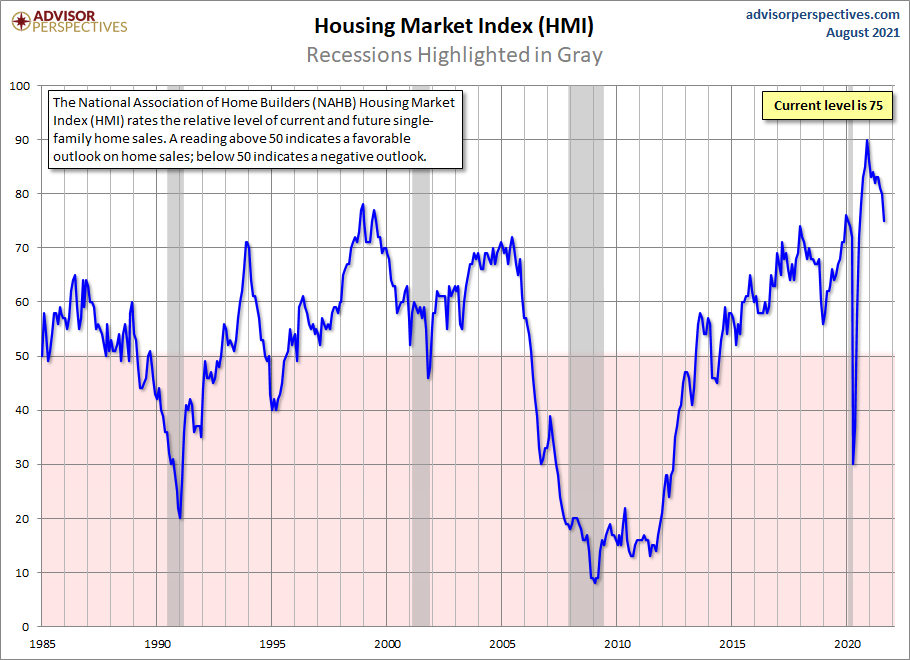

The builder’s confidence index, while historically high, has moderated from the parabolic move we had last year. Since the end of last year, a big theme of my work has been that all housing data will moderate following the surge due to the COVID-19 makeup demand. Builders’ confidence moves with the monthly supply data. When considering this data line, look at the rate of the change within a year.

While builder confidence is still at levels higher than the previous expansion, the monthly supply has been growing lately. The recent move lower in the confidence index is due to some of the moderation from the parabolic move we saw last year — similar to what we see with the existing home sales data.

The softness in this data is more noticeable because it is in proximity to near historical highs, so keep an eye on the monthly supply for new homes. Below 4.3 months, life is excellent for the builders; from 4.4 to 6.4 months of inventory, builders are meh. When inventory is over 6.5 months, builders start to pull back on construction to control pricing. Always use a three-month average when looking at the new home supply data.

Our take-home from this report is that permits are up with positive revisions. However, housing is in a slow and steady phase right now with pre-cycle highs in demand for housing permits.

Keep an eye on monthly supply in the new home sales. If demand is going to pick up, then the supply will be there to accommodate the buyers. The next new home sales report could breach above 6.5 months. Don’t think of the current market as a boom. Think instead that our good demographics will supply a steady stream of replacement buyers.

If total home sales are over 6.2 million when considering both new and existing homes during 2020 the 2024 period, then I consider that a beat of estimates. This could not have happened in the years 2008 to 20019 but now we do have the demographic capacity. We don’t have a credit boom, so that we won’t see a construction boom either. Slow and steady wins this race; the builders have been telling you that since 2008.