Expect 2024 to be mildly better than 2023 with mortgage rates falling in the second half of the year, housing experts opined in their forecasts at the end of the year.

Cuts to the Federal funds rate (and subsequently to mortgage rates) are imminent, traders enthused after December’s meeting of the Federal Open Market Committee in which committee members predicted three rate cuts in 2024. Some experts forecasted as many as six rate cuts in the year based on this news.

Rate cuts are still coming, just not in March, traders and market experts reasoned more recently as the economy continued to run hot.

And now on the heels of reports of stronger than expected jobs growth and stickier than anticipated inflation, the market’s shift from optimism to pessimism over rate cuts is complete. Some even expect rate hikes before rate cuts.

The pessimism is visible in mortgage rates. Freddie Mac‘s weekly Primary Mortgage Market Survey is climbing back towards 7%. HousingWire’s Mortgage Rate Center, which relies on data from Polly, is already above 7.2%. Rates were as low as 6.91% for Polly and 6.64% for Freddie as recently as February. On Tuesday, they reached 7.50% on Mortgage News Daily, a high for this year.

Mortgage rates hold major power in the housing industry; most importantly, high rates exacerbate the current affordability crisis by walloping the buying power of would-be buyers and discouraging some would-be sellers – those with low, fixed-rate mortgages – from listing their homes, a drain on available inventories.

Rising rates are already having visible effects. For example, the Mortgage Bankers Association‘s purchase index, which represents all mortgage applications for the purchase of single-family homes, has fallen for four straight weeks.

The market yield on a 10-year Treasury security, a product that often correlates with the movements of mortgage rates, hit 4.56% last week, its highest level since November of last year, before the market’s rate-cut bullishness began. That is a sign that traders expect high interest rates for longer – possibly even rate hikes before we see rate cuts.

All this leaves housing professionals once again fighting for their share of shrinking pies – as we have observed with recently released mortgage data and RealTrends Verified’s brokerage data, as well as deeper dives on the brokerage landscapes in Jacksonville and San Diego.

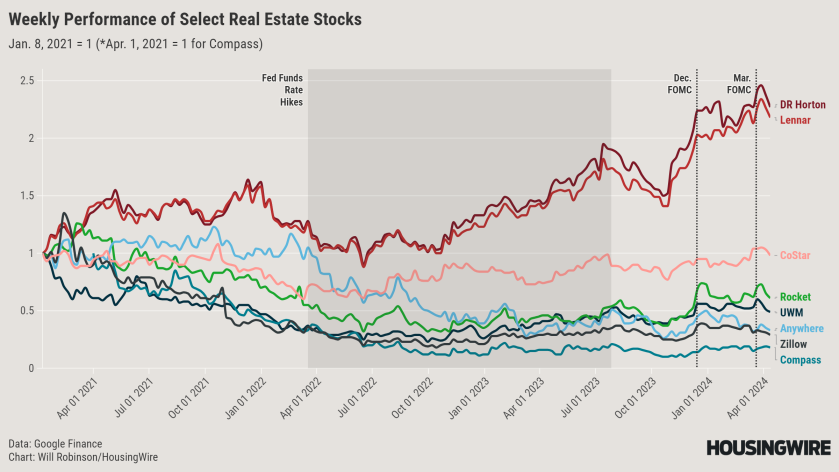

It is unsurprising, then, that real estate stocks have suffered since the FOMC’s March meeting and the recent job and inflation reports. That includes the nation’s top homebuilders (DR Horton and Lennar), mortgage originators (United Wholesale Mortgage and Rocket Mortgage), brokerages (Anywhere and Compass) and residential search portals (Zillow and CoStar, which owns Homes.com).

There are other dynamics at play for some of these companies, however.

The brokerages are also contending with the rule changes included in a proposed settlement by the National Association of Realtors; some investors also believe those rule changes advantage CoStar at the expense of Zillow.

UWM, meanwhile, is contending with a scathing investigative report by a hedge-fund-affiliated news organization whose hedge fund shorted UWM and went long on Rocket; it is also dealing with pending litigation. UWM denies the allegations made in the report.

High mortgage rates, fewer mortgage applications and fewer home sales are unfortunately not the only effects housing professionals could see from a more prolonged high-rate environment. There are also spillover effects from other industries, especially office real estate.

Regional banks – which traditionally have been major residential mortgage originators – went big on commercial real estate loans as larger banks scaled back in this area in recent years. That increased their exposure to downtown office towers, which have seen an exodus of tenants and a bottoming out of appraised values just as a record $2.2 trillion in commercial real estate debt comes due over the next few years.

That ties up capital that could otherwise flow to residential mortgages and in some cases stresses banks like New York Community Bank, parent of Flagstar Bank — the 7th-largest bank originator of residential mortgages, 5th-largest sub-servicer of mortgage loans and the 2nd-largest mortgage warehouse lender in the country.

Homebuilders, too, feel the effects of prolonged high rates. Although homebuilder confidence is still up significantly since last fall, new housing starts are slowing. The dim prospects for homebuyers have turned some investors to the nascent build-to-rent sector, essentially a bet that high rates are here to stay for long enough that would-be buyers are now would-be renters.