The rapid collapse of four regional banks that began last March shocked regulators and investors alike.

The banks had courted high-net-worth clients working in speculative tech and crypto startups in Silicon Valley, while also tying up a large portion of the banks’ assets in Treasury securities. When interest rates shot up, their customers needed cash at the same time that the banks’ assets became less valuable.

Since the Federal Deposit Insurance Corporation (FDIC) insures only up $250,000, the banks’ wealthier customers panicked and demanded all of their money immediately. A succession of bank runs wiped out the four banks, all of whom had concentrated too much of their customer base on this wealthy, tech-linked cohort.

The demise of those banks, which had relied in part on friendly terms on jumbo mortgage loans to entice wealthier clients, had lasting effects on the mortgage landscape – as part I and part II of our jumbo series show.

Regional banks are once again in the grip of a concentration problem. This time, it is not their depositors, but their loan recipients. Regional banks in recent years went big on commercial real estate loans for office towers throughout America’s downtowns, the same buildings that now often sit unoccupied while remote workers stay home.

For now, the problem is most acute at New York Community Bank — the 7th-largest bank originator of residential mortgages, 5th-largest sub-servicer of mortgage loans and the 2nd-largest mortgage warehouse lender in the country, according to its earnings materials.

Trouble at NYCB

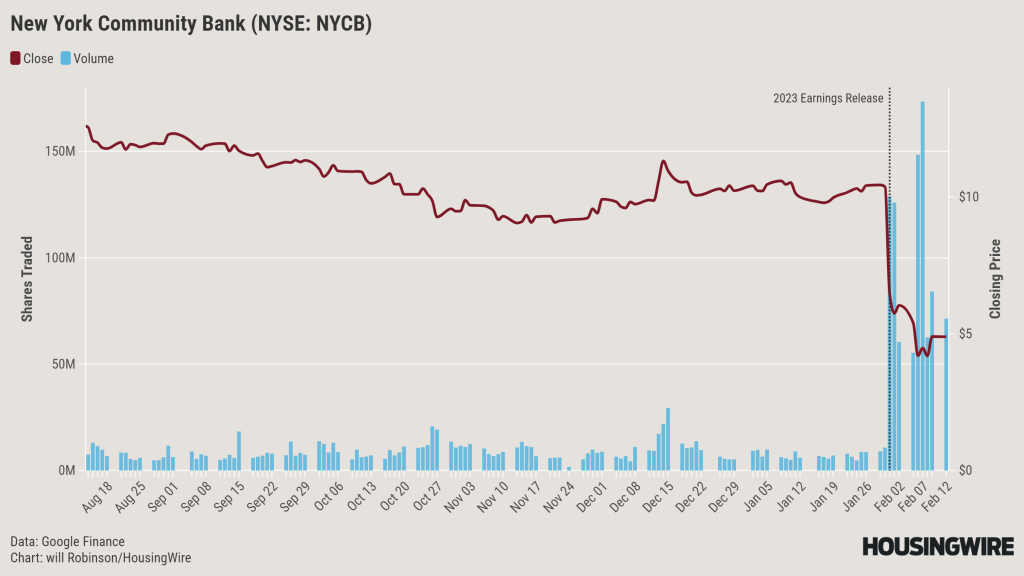

New York Community Bank released its earnings on Jan. 31. By the end of Feb. 1, the company had lost 45% of its market value.

Investors were shocked by NYCB’s $252 million net loss in the fourth quarter and outraged that the bank slashed its dividend from 17 cents a share to 5 cents a share. The dividend cut was needed to help the bank build up more than $552 million to protect against loan losses.

That is a huge build-up of loan loss reserves for NYCB. Reserves in the prior quarter had been just $62 million. The change was sparked by “weakness in the office sector,” according to earnings materials. The company had $185 million in charge-offs in the quarter, mostly from two loans — a co-op loan and an office loan.

The bank also raised its allowance for credit losses by $373 million in the fourth quarter, again “to address weakness in the office sector.”

Days later on Feb. 6, Moody’s downgraded its ratings on NYCB’s long-term and short-term debt to Ba2, or junk status. Moody’s also downgraded NYCB subsidiary Flagstar Bank, through which the bank originates residential mortgages.

NYCB had hoped to expand its reach when it acquired Flagstar in 2021, and it expanded its reach even further when Flagstar acquired most of the assets of Signature Bank, one of the banks that failed in last year’s banking crisis.

In a press release the same day as Moody’s downgrade, NYCB CEO Thomas Cangemi stated the company “took decisive actions to fortify our balance sheet and strengthen our risk management processes during the fourth quarter,” has not received downgrades from other rating agencies and is hiring a new chief risk officer.

The statement has not buoyed the company’s stock price, which has since fallen further. On Feb. 7, the bank was reportedly looking to transfer some of Flagstar’s residential mortgage assets, possibly through a “synthetic risk transfer” of low-interest-rate home loans, per Bloomberg.

A wave of office debt at regional banks

Higher capital requirements after the 2008 financial crisis caused large banks to pull back on their commercial real estate lending; regional banks, unburdened by those requirements, seized the opportunity for expansion, Bloomberg has reported.

As a result, smaller banks are more exposed to office-tower-tied debts just as $2.2 trillion in commercial real estate debt comes due in the next three years. Remote and hybrid work have dampened the prospects — and therefore valuations — of office towers across the country, causing tenants to miss rent payments and banks to write-down the asset values of the collateral tied to the loans they’ve made.

This in turn prompts banks to hoard more cash to cover losses by returning less cash to shareholders and being less active in the market, as NYCB did in the fourth quarter.

A contagion of bad office debts and high bank loss reserves at regional banks could be a big deal for residential mortgage originations. A HousingWire review of Home Mortgage Disclosure Act data of 54 regional banks with at least $2 billion in market capitalization found that just this subset of companies was responsible for 8.6% of all single-family originations in 2022, the most recent year of HMDA data available.

From 2019 to 2022, this cohort of large regional banks averaged about $224 billion across 866,000 single-family mortgage originations per year.

Their impact is far greater in certain regions. In 2022, these 54 banks were responsible for about 28% of all single-family mortgage originations in Puerto Rico, 26% in Hawaii, 21% in Montana and 20% in Ohio.

NYCB was the 2nd-biggest single-family mortgage lender by dollar amount and 4th-biggest by origination count in 2022 of the 54 banks reviewed by HousingWire.

Although primarily a CRE debt crisis (and most acute with office real estate), this debt problem matters for residential mortgages. Whether higher loan loss reserves prompt a pullback in residential mortgage originations or new bank failures lead to more consolidation among mortgage originators, CRE debt is another factor to watch in 2024.

For now, all eyes are on NYCB.