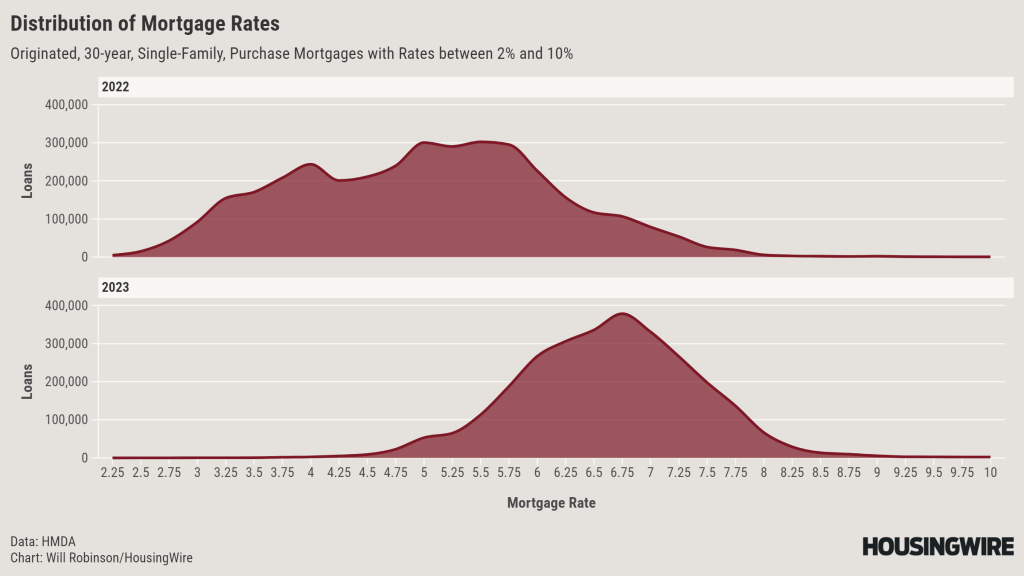

Perhaps the most striking detail gleaned from a HousingWire analysis of millions of single-family purchase mortgages is how much more homebuyers had to pay in 2023 compared to 2022.

The median borrower on a 30-year mortgage in 2023 received an interest rate of 6.625%, which is 1.635 percentage points higher than the same borrower a year prior. That is a difference of $309 a month, an 18.5% increase.

Out of 1,990 counties that had at least 100 single-family purchase mortgage originations in both 2022 and 2023, the median interest rate rose in every single one in 2023.

This analysis is based on the latest Modified Loan Application Register data published by the Consumer Financial Protection Bureau on March 26. Residential mortgage originators are responsible for filing data with the CFPB under the Home Mortgage Disclosure Act.

The rapid run-up in mortgage rates after years of low rates was a shock to buyers and a disincentive for prospective sellers to list their homes. The resultant tight housing inventories propped up record-high home prices, a bad pairing with high borrowing costs. Unsurprisingly, this hurt mortgage originations.

Mortgage Originations

Single-family purchase mortgages – excluding mortgages for commercial purposes, open-ended lines of credit and reverse mortgages – totaled about 3.2 million originations last year for a sum of $1.14 trillion. That represents a 21% drop in originations and a 23% drop in the amount of money loaned.

Originations fell in all but 82 of the 1,990 counties with at least 100 such mortgages in both 2022 and 2023.

United Wholesale Mortgage and Rocket Mortgage remain on top of the origination heap in terms of both originations and dollars loaned – highlighting the stakes of recent litigation against UWM and allegations made an investigative article published by a hedge-fund-affiliated news group whose hedge fund went long on Rocket and short on UWM.

As in other industries, including residential brokerage, the top 10 mortgage originators shared a smaller pie than in prior years:

Affordability

Lenders generally advise borrowers to take on mortgage payments that constitute no more than 28% of their monthly gross income. Income did not keep pace with the run-ups in home prices or mortgage rates, shrinking the pool of prospective buyers who can meet this rule of thumb.

The share of borrowers paying more than 28% of their monthly income on their mortgage rose in all but 103 of the 1,990 counties with at least 100 such mortgages in both 2022 and 2023. In 809 counties – or 40.7% of the subset of counties – the median share of income was above the 28% rule.

To see all county-level data used in this analysis, click through the filters in the map below: