Looking at the latest NAHB/Wells Fargo homebuilder confidence data and builder stock prices, I can say the homebuilders got very lucky this time around in the middle of a housing recession. There is one simple reason for this: it’s not 2008. They have less competition as they are working from low sales levels in today’s housing market.

The truth is that if mortgage rates fell below 5.875% and kept going lower, everyone’s housing predictions would need to be revised this year because the builders can sell their homes with lower mortgage rates. However, the glaring difference today versus the recession of 2008, is that in 2007 the builders had to deal with over 4 million active listings as competition for their pricey new homes.

Last year we had monthly existing home sales collapse back to 2007 levels, except this time around, NAR has total inventory at 970,000 and not over 4 million.

In an odd twist of fate, the delays due to COVID-19 are currently an infrastructure and jobs program for Americans in the construction industry. Let me explain my logic with today’s housing starts report.

Building permits

From Census: Building Permits: Privately-owned housing units authorized by building permits in January were at a seasonally adjusted annual rate of 1,339,000. This is 0.1 percent above the revised December rate of 1,337,000, but is 27.3 percent below the January 2022 rate of 1,841,000. Single-family authorizations in January were at a rate of 718,000; this is 1.8 percent below the revised December figure of 731,000. Authorizations of units in buildings with five units or more were at a rate of 563,000 in January.

As you can see in the chart below, housing permits are falling, new home sales are down, supply is up, and you don’t issue more housing permits in this environment. Homebuilders will only permit new housing when they don’t have excess supply and they know they can grow sales.

Housing starts: Privately-owned housing starts in January were at a seasonally adjusted annual rate of 1,309,000. This is 4.5 percent (±15.9 percent)* below the revised December estimate of 1,371,000 and is 21.4 percent (±10.6 percent) below the January 2022 rate of 1,666,000. Single-family housing starts in January were at a rate of 841,000; this is 4.3 percent (±16.4 percent)* below the revised December figure of 879,000. The January rate for units in buildings with five units or more was 457,000.

As housing permits fall, as you can see below, housing starts also fall, so nothing is abnormal here with the housing data while in a recession.

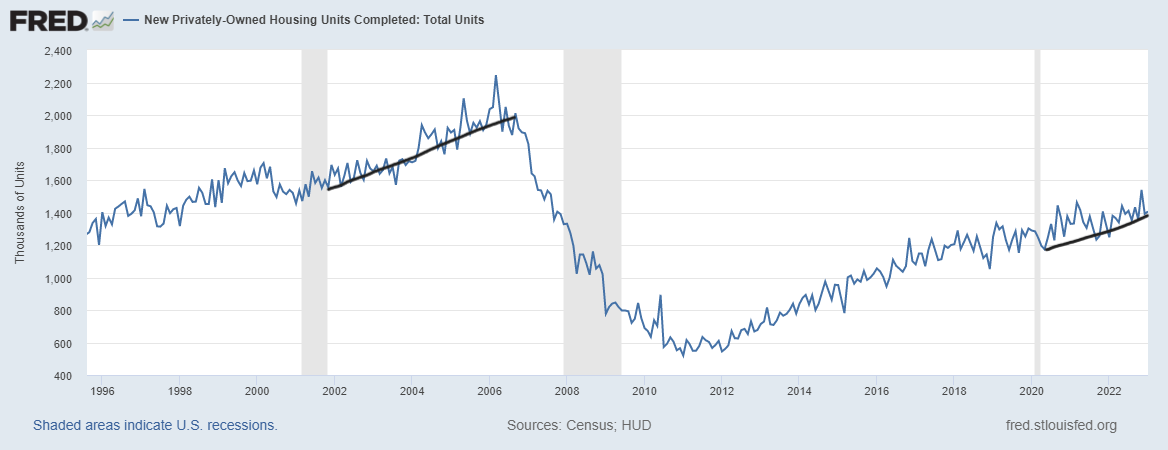

Now comes the abnormal data line: housing completions. This is so slow my tortoise would look like the flash against this data line.

Housing completions: Privately-owned housing completions in January were at a seasonally adjusted annual rate of 1,406,000. This is 1.0 percent (±9.8 percent)* above the revised December estimate of 1,392,000 and is 12.8 percent (±13.0 percent)* above the January 2022 rate of 1,247,000. Single-family housing completions in January were at a rate of 1,040,000; this is 4.4 percent (±10.4 percent)* above the revised December rate of 996,000. The January rate for units in buildings with five units or more was 349,000.

As you can see below, housing completions are slowly moving along; the homebuilders have more new homes under construction that they haven’t even started yet than active new homes for sale. While the two charts above are falling noticeably, housing completion data is slowly moving up. This is why construction workers haven’t been laid off while other jobs in the housing market have been.

Let me be honest here: we got lucky as a country. If the homebuilders and homebuyers knew rates would hit 7% in 2022, many would not have taken those contracts they’re canceling now. This means the builders would not have even considered taking permits out for those homes. So, for now, we are simply working through that backlog, which means we have more housing supply and construction workers are still employed.

However, to my first point, the builders are lucky that total housing inventory is near all-time lows because this means their product holds more value. Buyers have fewer choices than normal in the past eight years — but in reality, since 1982.

Homebuilders confidence

The homebuilder’s confidence index has picked up in the last two months, and three months ago, their forward-looking survey looked positive. I am not shocked that forward-looking housing data works again. As I have tried to highlight in my economic work, the housing market started to improve on Nov. 9, so we have three months of positive data trends filtering into the monthly housing reports now.

However, I tried to bring some context into this discussion on CNBC last Monday. Even though the housing data has improved, it needs to be understood in context from working off a historical dive in 2022.

Historically speaking, when you see a bounce in the homebuilder’s index like this, it tells us the economic recession is ending, or at least the housing recession has ended. However, I caution people not to look at it this way since the U.S. economy isn’t in recession today, and mortgage rates have risen almost 1% from the recent lows.

New home sales

Next up is the new home sales report that comes out next week, so let’s check on how the monthly supply for the builders looks before the report. In the last report, the builders had 9.0 months’ supply, as the chart below shows.

Here’s the breakout:

- 71,000 new homes have been completed: 1.4 months of supply.

- 291,000 homes are still under construction: 5.7 months of supply

- 99,000 homes have yet to be started: 1.9 months of supply

My rule of thumb for anticipating builder behavior is based on the three-month supply average. This has nothing to do with the existing home sales market; this monthly supply data only applies to the new home sales market, and the current nine months are too high for them to issue new permits.

- When supply is 4.3 months, and below, this is an excellent market for builders.

- When supply is 4.4 to 6.4 months, this is an OK market for the builders. They will build as long as new home sales are growing.

- The builders will pull back on construction when the supply is 6.5 months and above.

Still, the builders have some work to do, and thankfully they’re keeping construction workers employed while working off their backlog.

Homebuilders are efficient sellers of homes because it’s like a commodity to them; they don’t have to look for shelter after they sell or have a 3% mortgage rate they have to give up after they sell.

Back to the basics

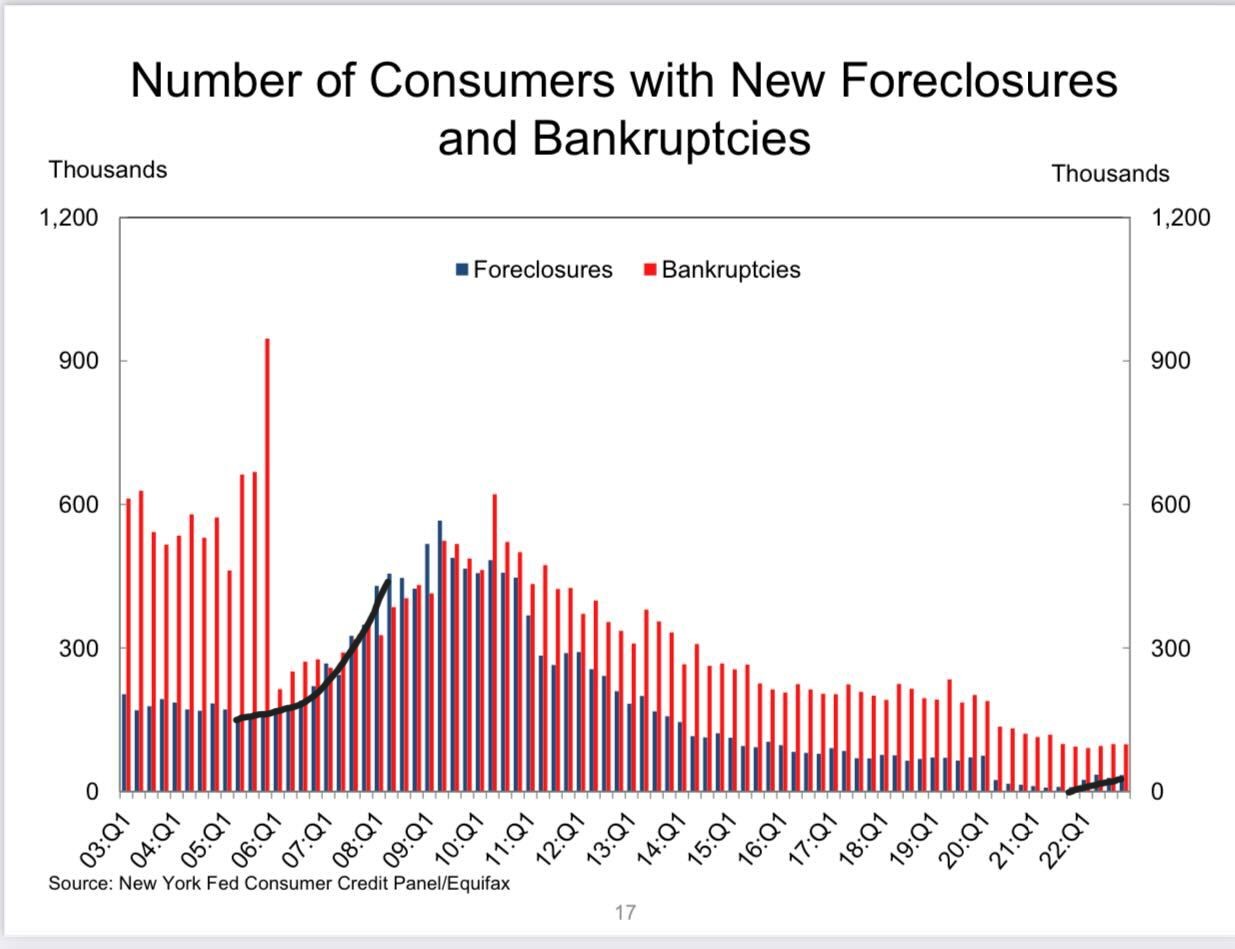

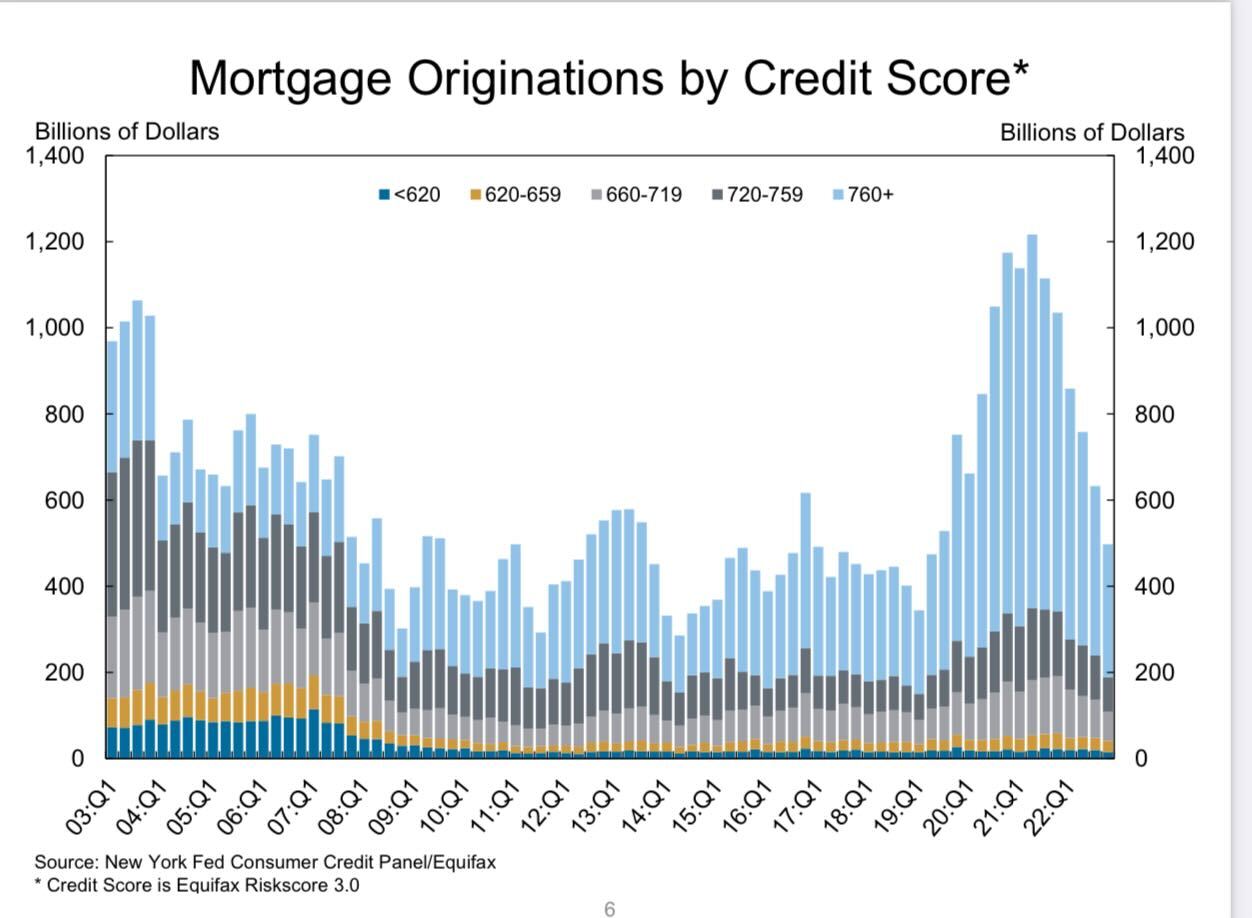

Lower mortgage rates are good for the housing market, and higher rates are bad; we are back to basic affordability demand here. Just look at the chart below and how bad credit looked from 2005 to 2008, then the job loss recession happened. This chart is a direct link to the excess supply that the homebuilders don’t have to deal with today.

Also, look how small the data looks in the bottom corner right If you need your glasses, I don’t blame you.

Today, homeowners look great on paper. In an inflationary environment of rising wages they have fixed long-term debt. The American home and its fixed long-term debt cost has been the best hedge against inflation.

Now, the question is: How much longer can this last? People buy and sell homes every year and total inventory growth can happen over time as homes stay on the market longer and longer. With mortgage rates up again, this can lead to inventory growing higher when homes take longer to sell.

Last year new listing growth turned negative year over year when rates got over 6%; now with rates rising into the spring season, we will see a lack of enthusiasm from sellers.

COULD YOU FORMAT THE ARTICLES SO THEY CAN BE PRINTED EASIER.

By right-clicking your mouse, the article doesn’t print efficiently.

FYI, I think the employment numbers are overstated in terms of the strength of the economy. I bet there is a large percentage of the net new jobs that are replacing the boomers retiring. Those replacements don’t show up in the new job numbers.

Having said that, its still impressive for housing since the boomer is probably staying in their home or some form of shelter, so the 517,000 new jobs is still adding around 200,000 of new household formations. Which is huge.