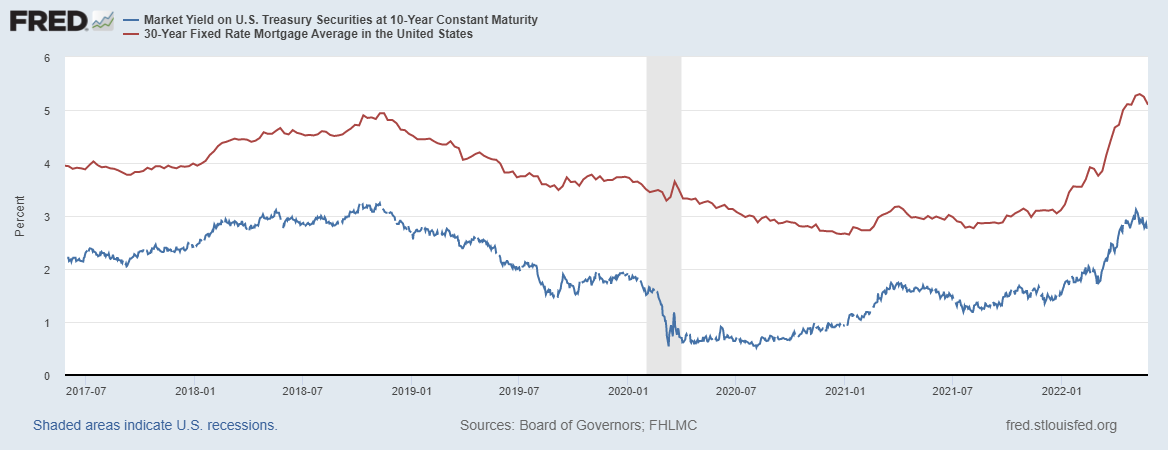

It’s an excellent time to discuss housing inventory. The housing market shifted in March of this year. As the 10-year yield broke above 1.94% and mortgage rates rose, we saw the impact on housing data. Since the summer of 2020, this has been my main talking point on what can cool down housing; it’s a 10-year yield above 1.94%, meaning rates above 4%.

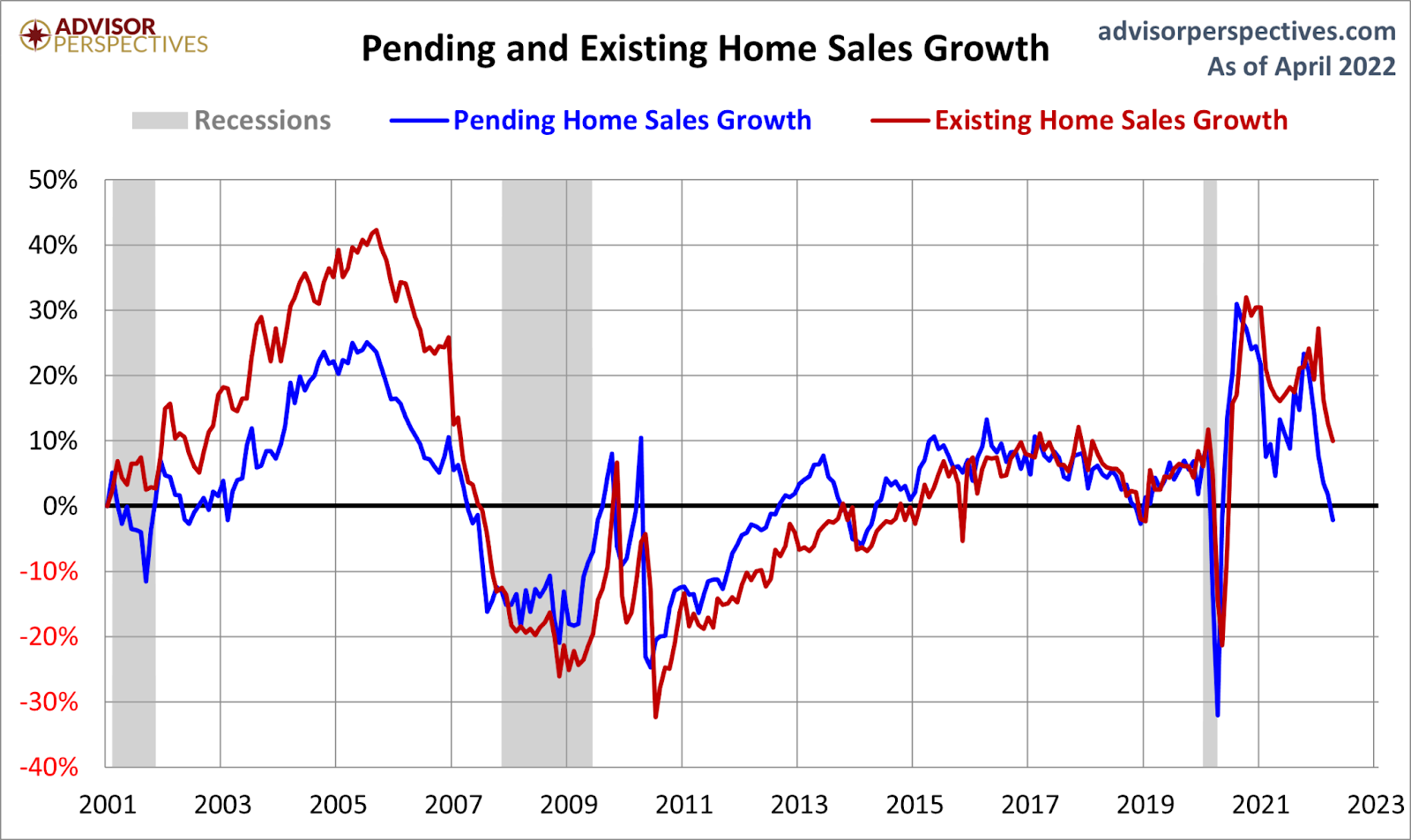

We see this in the data. Purchase application data, while doing better than I thought it would with rates over 5%, is still negative year over year, and this time it’s real. Last year we had COVID-19 comps. Now, it’s no longer the case, this negative trend is real on a year-over-year basis.

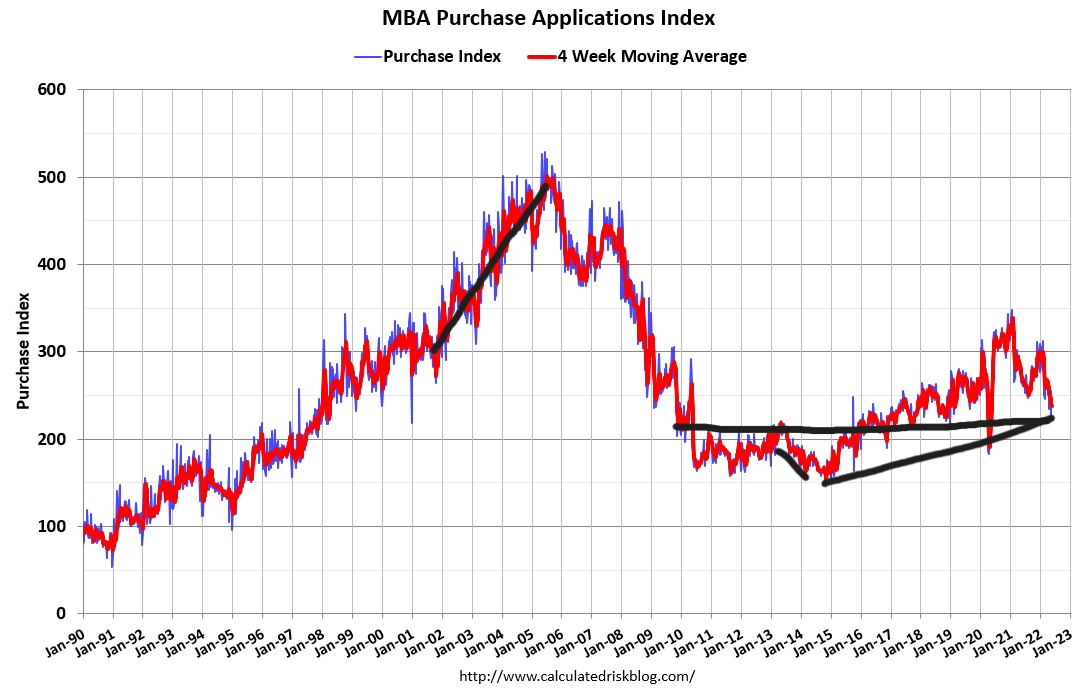

This week’s purchase application data showed week-to-week growth of 0.2%. The year-over-year data is down 16%. The four-week moving average is down 12.5%. I anticipated negative declines of 18%-22% by now, so that hasn’t happened yet on the four-week average. We will have more challenging comps to work in October of this year, and maybe that 18%-22% decline will happen then.

Today, however, the purchase application data is actually down to levels we saw in 2009!

Yes, crazy to think, but this is a survey trend data line, and the housing market was in free-fall at that time. That’s not the case now because we have’t had a credit boom post-2010 as we did from 2002 to 2005. If you connect the lines, you can see where we are on a historical basis.

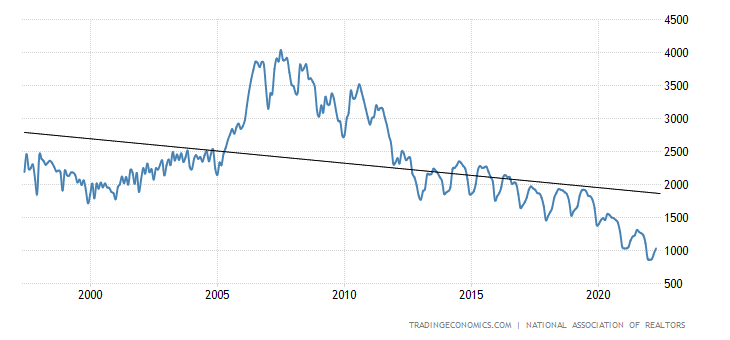

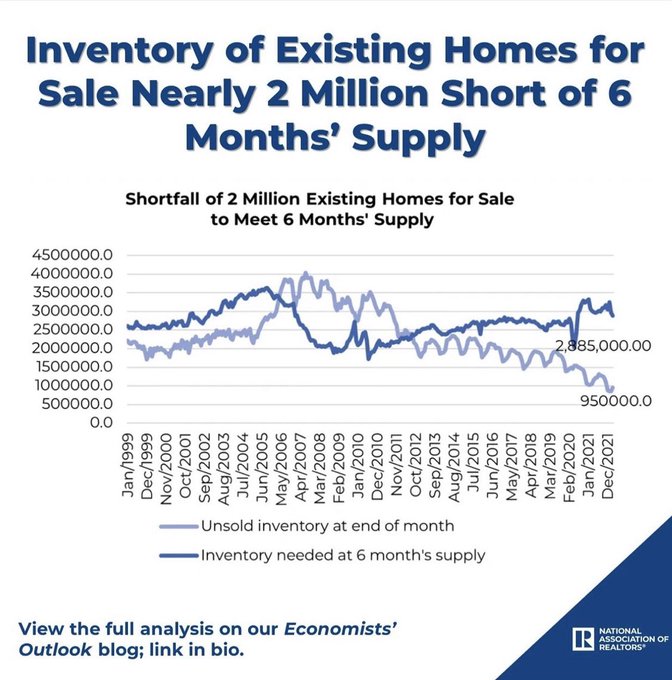

What is going on here? How can housing inventory be so low today when it skyrocketed back in 2009? Let’s take a look here together because I have been worried about unhealthy home price growth since the breakout in housing demand in 2020, but it’s not because of record-breaking credit demand. It’s more of a lack of supply.

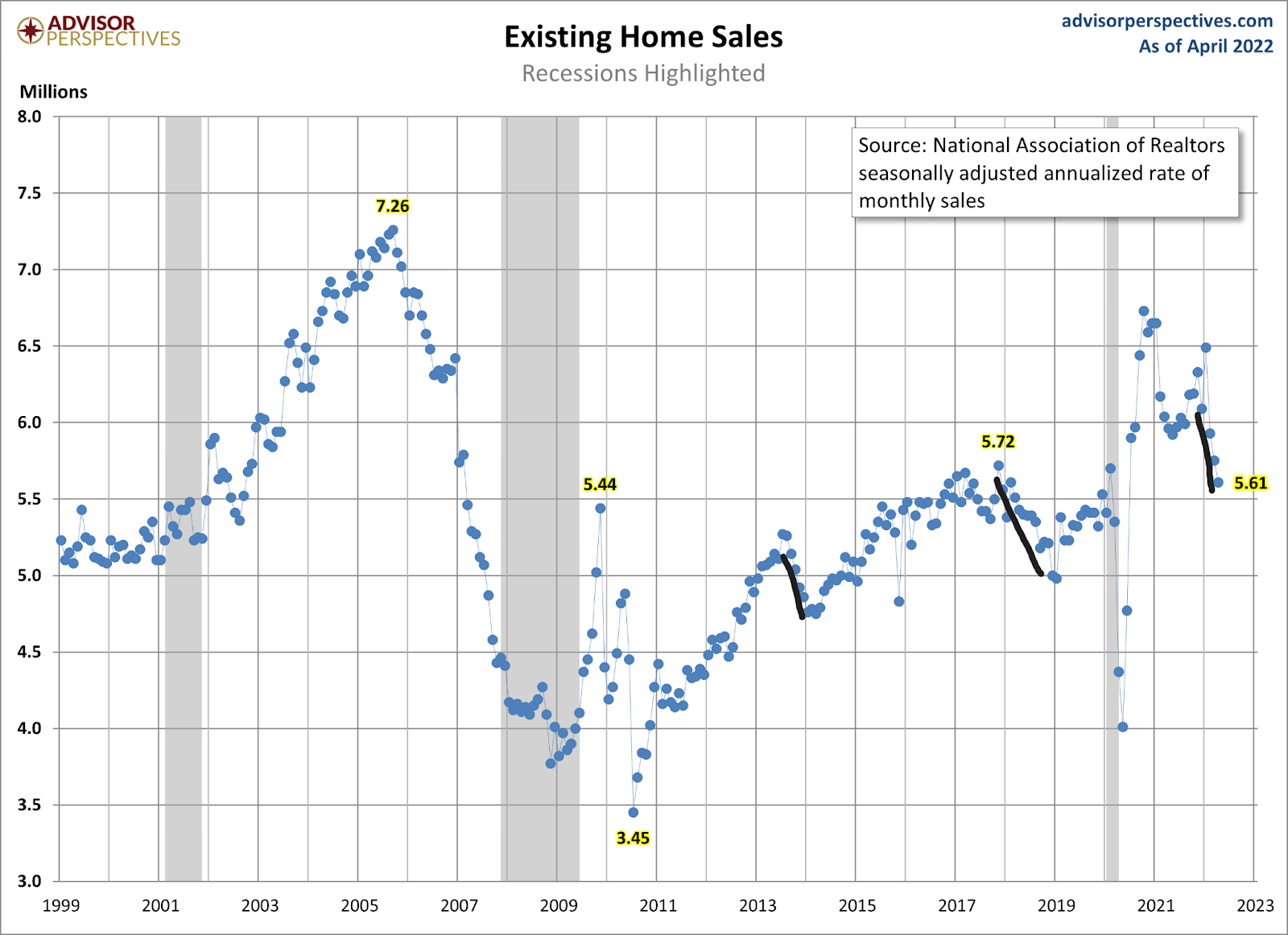

If you follow the trend of housing supply since 2014, it’s been falling every year — with a pause in 2018-2019 — and then collapsed lower post-2020. Now don’t get me wrong: demand is better in 2020 and 2021 than in any single year from 2008 to 2019. We had roughly 300,000 more existing home sales in 2020 than in 2019 and 800,000 more in 2021. I would average those two out because I believe we got some demand push through from the second-half surge in demand in 2020 into 2021.

So, on average, just 500,000 more homes were bought than in 2019. If I take existing home sales from 2017 levels, it’s roughly, on average, just 300,000. Currently, home sales are falling like when rates rise.

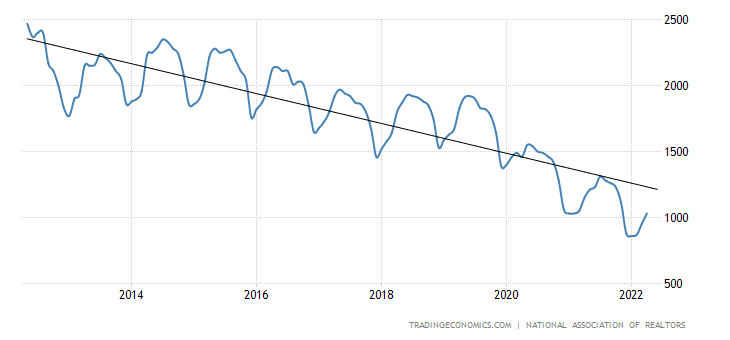

As you can see below, the inventory keeps falling from 2014 levels, and even with the weakness in demand this year, we are nowhere close to 2013 levels, let alone 2018 levels.

I don’t believe housing inventory below 1.52 million is a natural state for the U.S. housing market. This is a red danger zone area for forced bidding action, which destroyed my affordability models in just 2.5 years since the start of 2020. In reality, my worst fear for housing came true, and it got even worse in the early part of 2022 as we had record low inventory creating more forced bidding. You can understand why I upgraded the housing market from unhealthy to savagely unhealthy

Of course, being “team higher rates” since February of 2021 isn’t the most popular talking point, but in 2022 I increased my call for higher rates to create some balance — otherwise or pricing can get even worse. We are seeing higher rates do their thing. Today pending home sales came in at another decline.

Inventory data for the first time is showing growth, which is a good thing, folks; we don’t want to stay at these low levels and see more and more unhealthy home-price growth.

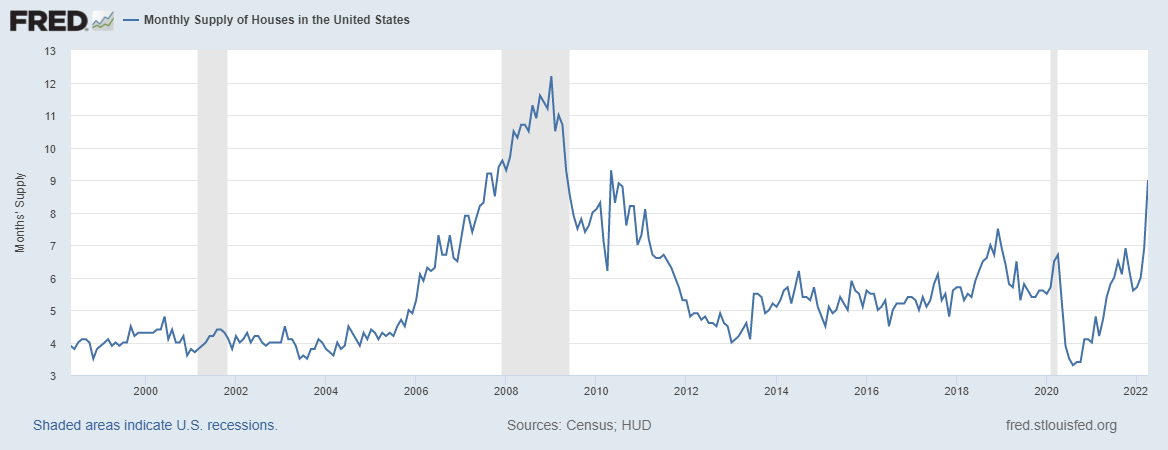

But we should ask: Why is inventory so much lower now if purchase application data is at 2009 levels — a period in time when inventory was rising noticeably in 2006, 2007, 2008 and 2009?

The first answer is that people are staying in their homes longer post-2008. Housing tenure ran at five to seven years from 1985-2007 and now is 11-13 years from 2008 2022. The Baby Boomers are not selling their homes en masse, and we have more investors providing shelter for renters than before.

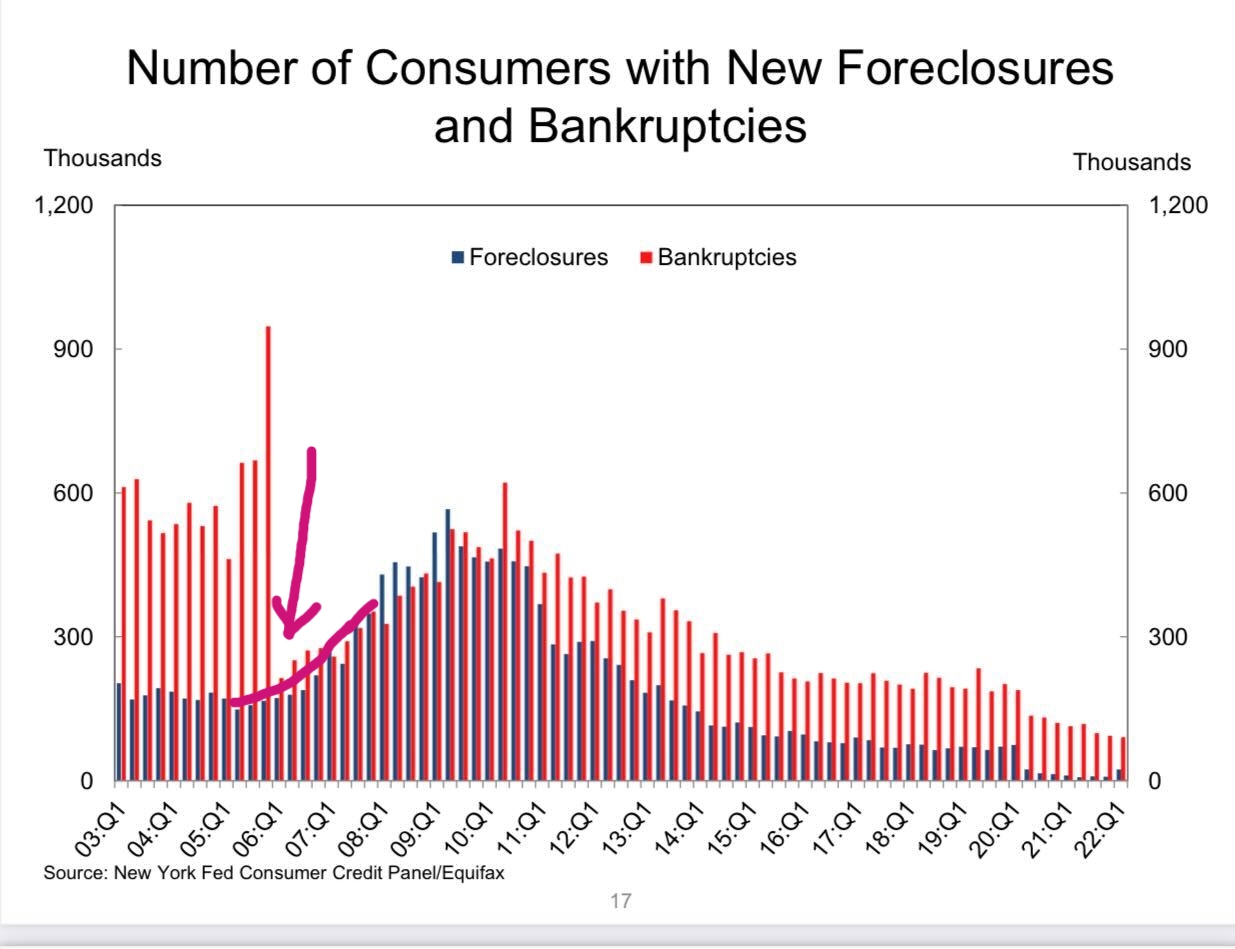

However, the spike in inventory that we saw from 2006 to 2011 can be attributed to the massive credit bubble we had from 2002 to 2005. You don’t want to overcomplicate this topic. Credit stress was evident from 2005 to 2008. People were filing for foreclosures and bankruptcy for years, and then, after all that, the job loss recession happened in 2008.

With a credit boom and credit bust, the monthly supply for homes in America got over six months for years. It took many years to clear up the credit deleveraging process that needed to occur in the U.S. housing market due to rapid credit expansion with exotic loan debt products.

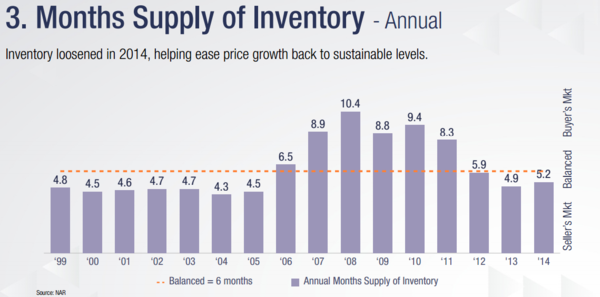

The housing market post-1996 has had a hard time creating more than six months’ supply unless you have extreme housing weakness and forced credit selling. These two factors were happening from 2006 to 2011 and added supply to the market. Demand has been stable enough to keep supply low, and we have no forced credit selling since the great financial crisis. This has been an issue in getting the market balanced for some years now.

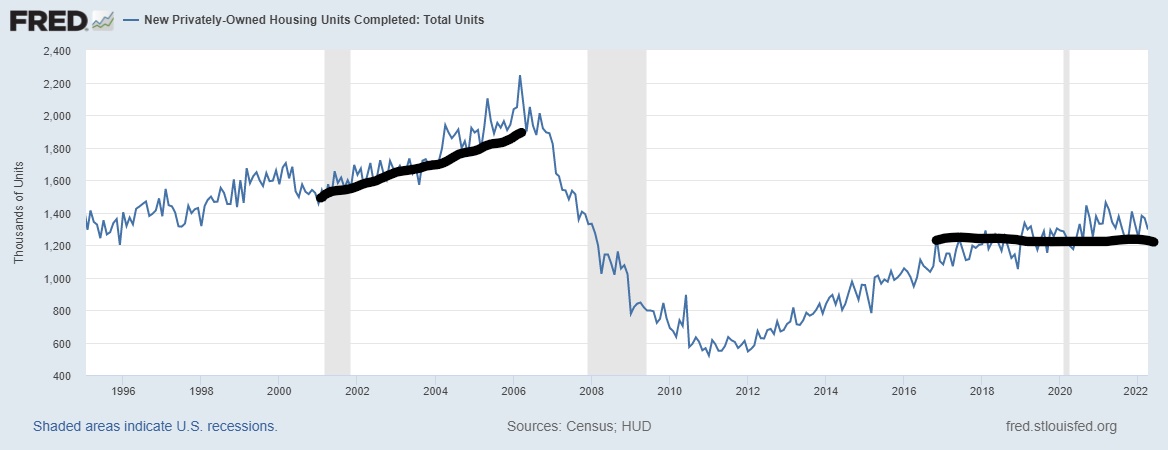

What about the builders? We have more housing starts under construction now than in recent history! This is true except for one big reality!

The monthly spike in the new home sales sector looks like massive inventory should be here. Well, six months of that supply are homes that haven’t even been started, and only three months of supply are completed. We have a lot of multifamily construction going on that won’t help the homebuyer.

On top of everything else that we need to deal with on housing, housing completion data has looked terrible for years. People forget when rates rose to 5% in 2018, it delayed housing construction from really growing for 30 months. Then COVID-19 happened and the rest is history; I can’t express to you enough how everything that was supposed to go right for housing flipped negatively, and this is just one of them.

So when we look at the housing starts data, we need more context with it, and we can see that it has a much different backdrop than what we saw from 2002 to 2005, when housing starts were driven by new home sales and single-family starts on a credit bubble. Now we see a different reality with a big push in multifamily construction and a lack of complete data.

Of course, one of the issues now is that rising rates impact the new home sales sector more than the existing home market, so the builders, while not in the same situation they were in in 2002-2005, will be more cautious in building homes with the rising rate risk cancelations and future buyers. They’re at a disadvantage because their homes are more expensive than the existing home supply.

Hopefully, this article outlines the issues we have had with housing since 1996 and why it’s been hard to get inventory to grow unless we see major demand weakness and forced credit selling. I am rooting for more listings than anyone else, but I understand the limits that we have been under post-1996.

Higher mortgage rates in the past have created more days on the market and cooled down the rate of price growth, which I am hoping for again. However, the homeowner’s credit profile is much better this time around. Their cash flow is better.

They have fixed debt costs while their wages rise, an excellent hedge against all this inflation we are dealing with.

On top of all that above, they have nested equity, and more than 40% of the homes in America have no mortgage debt at all. I am hoping that if demand gets weaker, home sellers won’t be so stingy and will lower their prices because they have so much equity now. Hey, a person can hope, right!

Enjoy the Memorial Day weekend and realize that not all economic cycles run with the same playbook. We have to learn to talk about the housing market in a more sophisticated way that doesn’t have to do with an epic housing crash for clicks. Sometimes a long, painful drag is even just as bad and that home prices rising way too much is the crisis now.

Logan,

Great analysis as usual. We go to market with home on Puget Sound on the 31st so real data coming soon.

Best,

Matt

Logan

Thank you for helping to explain why inventory has remained consistently low and moved in a southerly trajectory for over a decade. I have thought about it a lot this past decade with no viable explanation until today. I would opine that the lack of a Major Demand Weakness is “trumped” by the “Demographic Sweet Spot” for the years 2020-2024 you have been expounding since 2020.

Happy Memorial Day to you & yours!

Robert

Logan, do you think extended housing tenure could recoil and release pent-up relocation or trade-up/trade-down movement as HPA stabilizes? Or do you think we’re finding a new normal at the 11-13 yr band…. at least until baby-boomers hit a certain age?

Hi Matt

While inventory is rising from record lows, it’s still well below my comfort zone. Once we get back to 2019 levels, I will feel much better about the inventory data. We Still have some work to do.

Hi Robert

Yes, demographics equal demand. They needed the shelter, but we didn’t have the supply for them, hence the forced bidding action. It’s sad to see all this price growth, but this is a first-world problem compared to what happened from 2005-to 2011.

Clayton, I always believed people would move more during the years 2020-2024 because that is the right time for people to get bigger homes. This was well before work from home; however, with the Baby Boomers staying in their homes until death and the more oversized home product now available since we went all in post-1996 on the bigger houses. Being above ten years should be the norm.

I am now smarter for reading this article… thank you for all of your hard work (I actually read your piece of work twice!)

This is why it’s always good to have one nerdy friend that has no life.