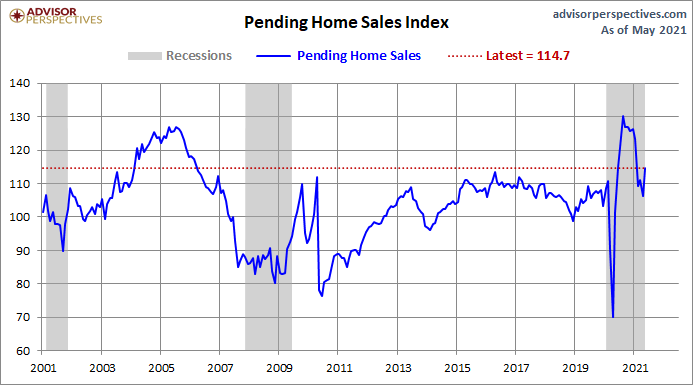

The most recent pending home sales report that soundly beat estimates after a downtrend in the previous months caused some serious head-scratching. Pending home sales were up a healthy 8% from April and just over 13% compared to the same month last year. Of course, last year’s comps should be discounted due to COVID-19.

From the National Association of Realtors: “Pending home sales rose 8% in May from the prior month and 13.1% from one year ago. The May 2021 Pending Home Sales Index of 114.7 is the highest reading for May since 2005. Contract signings rose in all regions in May compared to the prior month and one year ago.“

I agree the data looks wonky, but there is a method to the madness. Here is what is happening: The COVID-19 shutdowns paused sales during what looked to be a solid market going into the first few months of 2020. Once the fears of COVID-19 faded, the backup demand resulted in a straight vertical in sales data in the second half of 2020. Some of that make-up demand bled over into the early months of 2021. The weeks of stalled sales due to COVID-19 gave us a low bar to work from for 2021, so that is why the year-over-year data appears strong.

However, in absolute numbers, existing home sales ended 2020 at 5,640,000, which was only 130,000 more homes sold than in 2017. After the spike in make-up demand, sales are moderating, going back to trend. The data essentially forms a base of stable sales, putting an end to the wild swings in the data. I expect it will take a few more months of fluctuations to establish that base.

Even with the extreme ups and downs of the housing data last year, every existing home sales print of 2021 has been higher than last year. This is with the excessive year-over-year price growth and low total inventory. What is apparent to all of us now is that more Americans are buying homes with mortgages in 2020-2021 than any single year from 2008 to 2019. Total sales growth is still trending higher this year but not booming, and considering our demographics and mortgage rates, things look normal on the demand front.

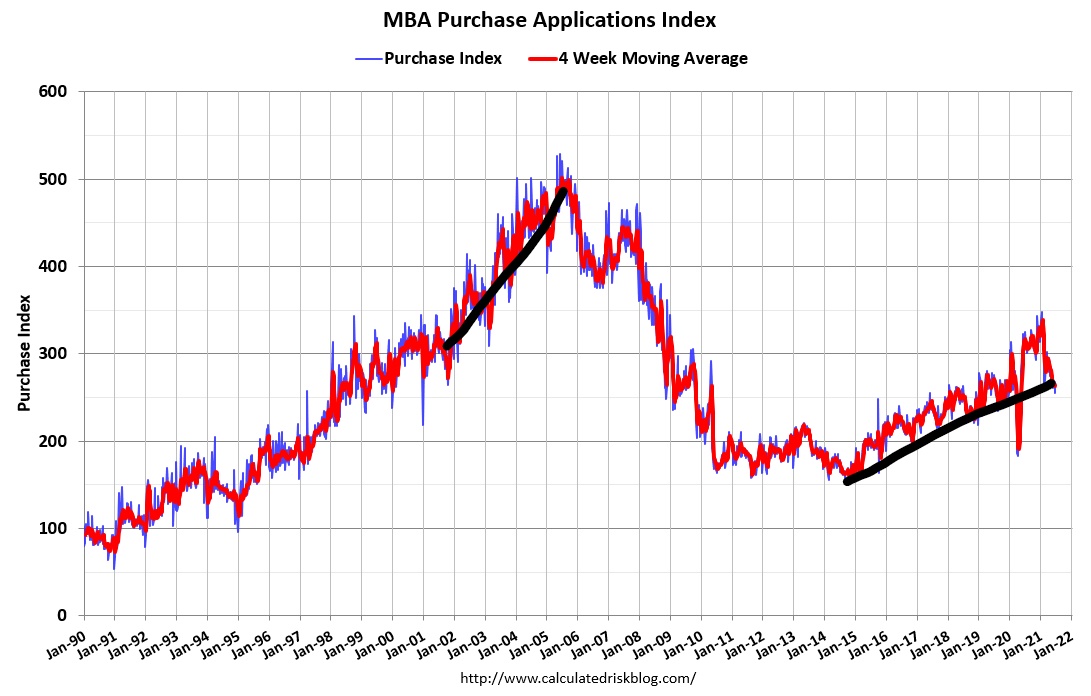

Earlier this year, I wrote that purchase application data in the second half of 2021 would be negative year over year. For the same reasons I described above, we should ignore the year-over-year data after March 20 this year, even though purchase applications were trending positively in the double digits in 2020.

Purchase application data provide an excellent example of how the year-over-year data can be misleading. COVID-19 created a crazy waterfall dive in the data then; not only did we have a V-shaped recovery in this data line, but the total volumes blew out expectations for the second half of 2020. Volumes never rise post-May in this data line last year; an artificially high level was created as sales were rebounding.

For the second half of 2021, keep an eye on the overall trends for both existing home sales and pending home sales, rather than trying to read the tea leaves on any single move, either up or down, in the monthly data. The stronger-than-expected numbers in pending home sales have confused some people. Ignore them and keep your eye on the prize — it’s all about that base. We will likely be fluctuating around a base as this data normalizes. Give it some time to find that stabilizing level but know that the demographics of America don’t move up and down as housing data did during COVID-19.

Total inventory has ticked up a bit recently, so buyers in the existing home sales market will have more choice and should be facing fewer multiple bid situations.

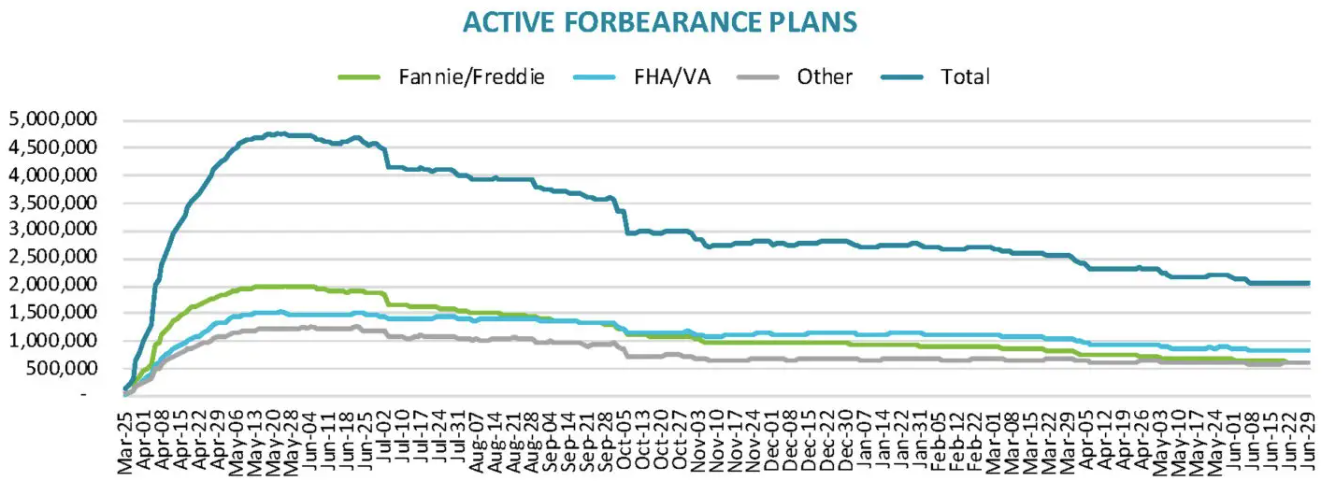

Some have suggested that when the forbearance programs time out, we will see massive unloading of inventory as distressed homeowners are forced to sell. This was the main proposition of a group I named the forbearance crash bros. I don’t expect this enormous increase will happen for a couple of reasons.

First: Jobs!

The most recent jobs report showed 850,000 jobs were created last month. I still believe that we will recover all the jobs lost due to COVID-19 by September 2022 or earlier. Currently, we are 6.8 million jobs away from getting that goal and have 9.3 million job openings. Higher paying jobs, the kind held by homeowners, are returning faster than those with lower-wage jobs, and the bulk of the jobs lost were tied to those with a renter financial profile. A strong employment picture means fewer distressed homeowners who will be forced to sell.

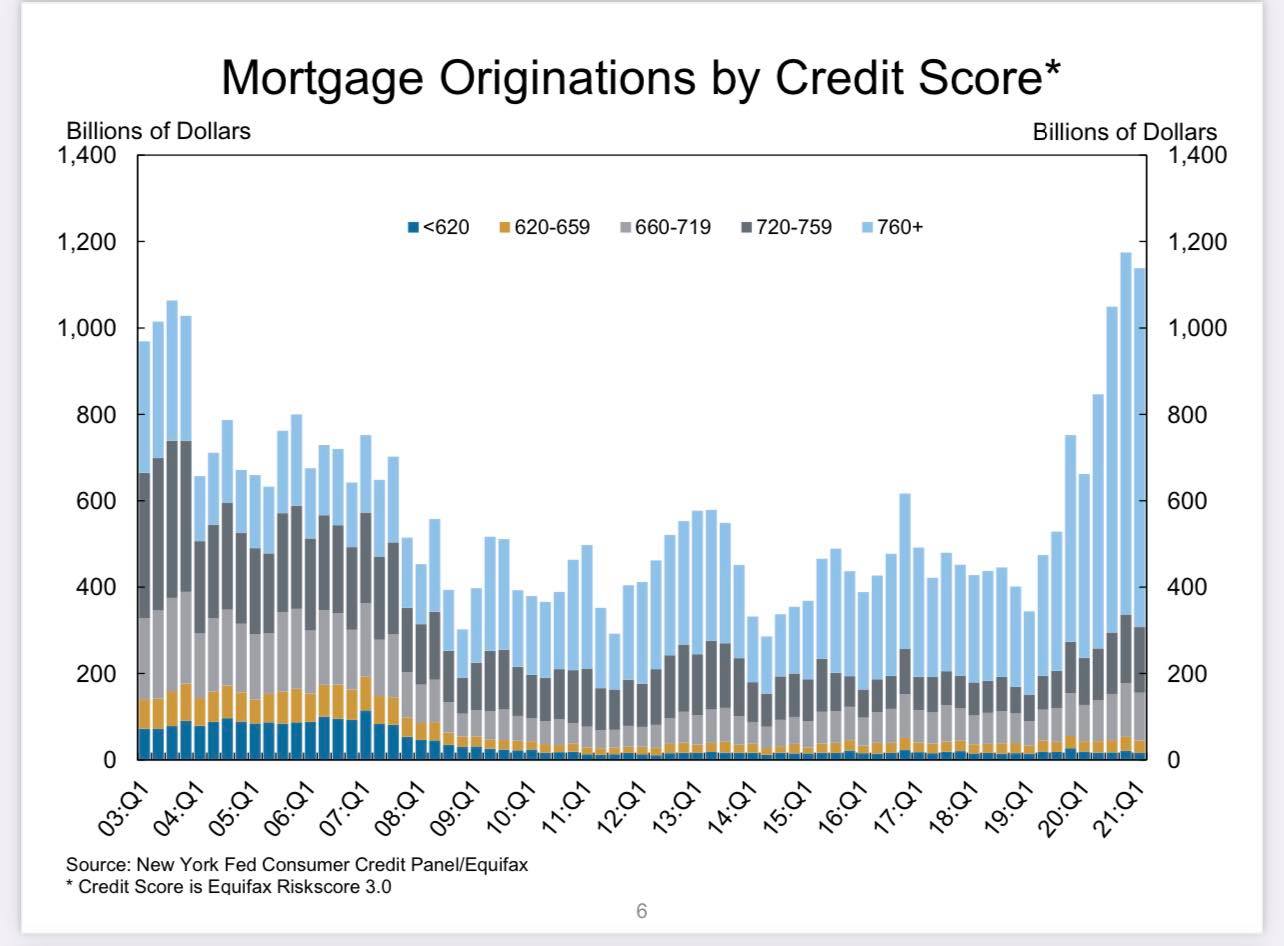

But even if they do have to sell, the loan quality in the previous expansion was excellent, which means loan holders had good cash flow and were building equity. When loan holders get their incomes back, there is a very high probability that they get off of forbearance and get back on track, paying their mortgages.

Second, what started at near 5 million homes in forbearance has fallen toward 2 million. The core basis of the forbearance crash bros was that unemployment rates would keep on rising, the U.S. would not recover soon, and 10-20 million loans could be in forbearance just like the distress markets after the housing bubble popped. The exact opposite happened.

From Black Knight:

Third, homeowners in forbearance have a lot of incentives to stay in their homes. First, of course, it’s the house they live in and the neighborhood they have developed a relationship with: the local schools and places to visit with their kids. Also, with a fixed low debt cost, renting might not even be a much cheaper option for some families since rates have been falling and their wages rising.

Finally, even if they sold, assuming they couldn’t buy a home with the cash, do these homeowners want to be a part of this unhealthy housing market where prices are up well more than 20% since 2019?

Homeowners have a lot of motivation to stay, but landlords who haven’t been getting their rent payments, that is another story altogether. While I do believe we will see some forced selling when the plans expire, it was never going to be the collapse of housing as many had hoped for.

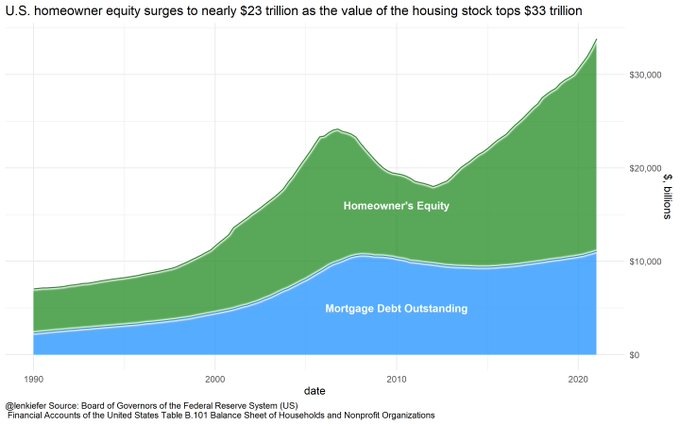

From Freddie Mac Chief Economist Len Kiefer:

During this July 4th weekend, I want everyone to enjoy Independence Day, even the much-maligned forbearance crash bros. I raise a hot dog to them for trying. But that whole 2021 forbearance crash thing just isn’t going to happen. Educated high-income homeowners, even those in forbearance, are not going to sell their homes at a massive discount for no reason. So just stop.

This 4th of July, we have reason to celebrate. Jobs are plentiful, wage growth is picking up, the savings rate is high and more and more people are getting vaccinated. This sets us up for a substantial economic expansion in 2022.

Additionally, the federal government about to kick in with a significant fiscal spending plan, and we can anticipate that something will be done to help with student loan debt. Politics are politics, so the process to get these things done will be neither fast nor elegant, but we can safely say our economy is solid and growing.