The housing market saw inventory fall 4% last week from the week before. That’s a big one-week change. Does that mean we are heading back to all-time lows in inventory again for 2023?

Traditionally, we do see housing inventory fall in the month of December, however, we clearly saw in the second half of 2022 that higher rates created more days on the market and inventory was lingering longer. During the last four weeks and especially this past week, we are seeing inventory decline faster than expected.

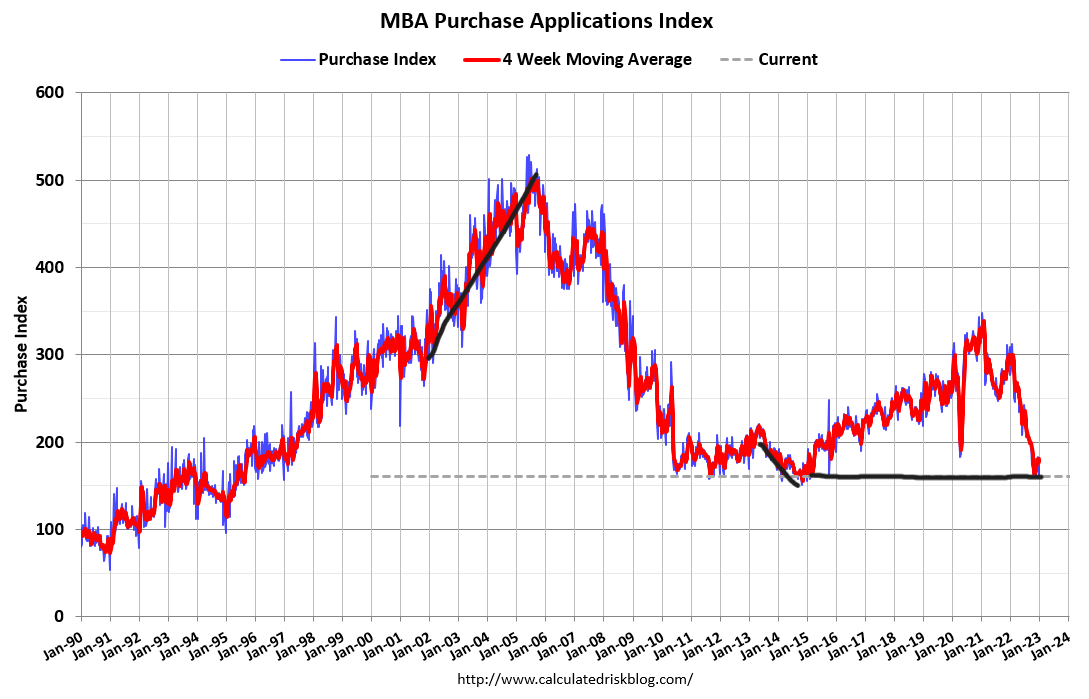

So, is this the traditional seasonal decline we see during every December/January, or have falling mortgage rates (since mid November) contributed to this? The purchase application data will help us find the answer. Purchase application data corresponds to future demand, meaning that even when the number of applications is growing, we won’t see it in sales data until 30-90 days out. This is why we need to track it on a weekly basis.

Purchase application data

Usually, I wouldn’t put much weight in data for the last week and the first week of the year because it’s seasonally the slowest period. However, even with a seasonal decline in volume and the fact that many people don’t apply for a mortgage during the holidays, there is something to be seen here because the data line snapped a seven-week positive trend as mortgage rates rose toward the end of the year.

Before these two weeks, purchase applications had seven weeks of positive data, tracking with the drop in mortgage rates from 7.37% in November to 6.12%. Then rates rose toward the end of the year to back over 6.5%: that rise in rates could have facilitated the weaker purchase application data in the past two weeks.

Since purchase applications deviated from the trend and changed with higher rates, we have to pay attention to that. Now that mortgage rates have fallen again, the next few weeks will provide more clarity.

Purchase application data is very seasonal in a standard setting: it typically rises after the second week of January through the first week of May. Traditionally after May, total volume always falls. However, the year-over-year data is still critical to keep track of for the housing market.

We have to show discipline here; this data line had a historic waterfall dive, wiping out seven years of gains in one year (see chart below). The bar is so low that we can all trip over it, so the weekly data focus will be critical.

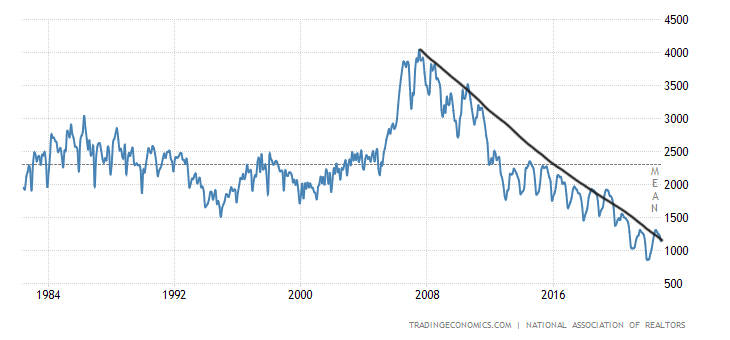

Weekly housing inventory

As noted above, the last few weeks have seen a noticeable 4% decline in inventory. Most of that decline can be attributed to the yearly seasonal decrease. If purchase application data started to improve toward the end of the year, and it looks out 30-90 days, then some of the inventory clearing can be attributed to better demand, not just the seasonal decline in inventory.

- Weekly inventory change: (Dec. 30, 2022-Jan. 6, 2023): Fell from 490,809 to 471,349

- Same week last year: (Dec. 31, 2021-Jan. 7, 2022): Fell from 293,477 to 292,021

Altos Research gives us a fresh look at weekly data before the traditional outlets give us that data line. As we can see in the chart below, the weekly inventory data is now heading down more noticeably. We want to see whether this weekly data stops declining before the spring seasonal push in inventory or if we will have a repeat of the second half of 2022, where we saw a lack of new listing growth. That mean homebuyers would have slim pickings again for the spring buying season.

What we don’t want to happen this year is a decline in new listing data on a yearly basis. We saw that after June 2022, and that showed me that the housing market wasn’t functioning normally.

We are on the cusp of breaking under 1 million total active listings, and if this happens in 2023, it will be only the second time in recent history this has occurred.

Per the last existing home sales report, we have 1.14 million homes for sale. Historically, the U.S. has between 2 million and 2.5 million. During the height of the housing bubble years, we had 4 million.

10-year yield and mortgage rates

The big story of last week was that after the solid jobs report, the 10-year yield fell lower, sending mortgage rates down to 6.20%. The bond market likes to see wage growth cooling down because if headline inflation is falling and wage growth is falling, the bond market is looking for the end of the rate-hike cycle.

Since the November CPI report, it’s been hard for the 10-year yield to break above 4.25%, and the bond market has decided that the peak growth rate of inflation has already happened, even with the labor market still tight.

I think the bond market is getting ahead of the Fed with the inflation story. We still have a tight labor market and mortgage rates are already falling. Now imagine if the labor market data get weaker, which is part of the Fed’s forecast. It’s hard to conceive now that mortgage rates would get up toward 8%.

This is a critical discussion for housing because the housing market is impacted disproportionately when rates fall during recessionary data. After all, most homeowners, buyers, and sellers who will buy homes are still employed during any traditional recession and can leverage lower rates to help affordability.

The week ahead

What we want to do with this weekly Housing Market Tracker is see the most current update to demand when rates rise or fall with purchase application data.

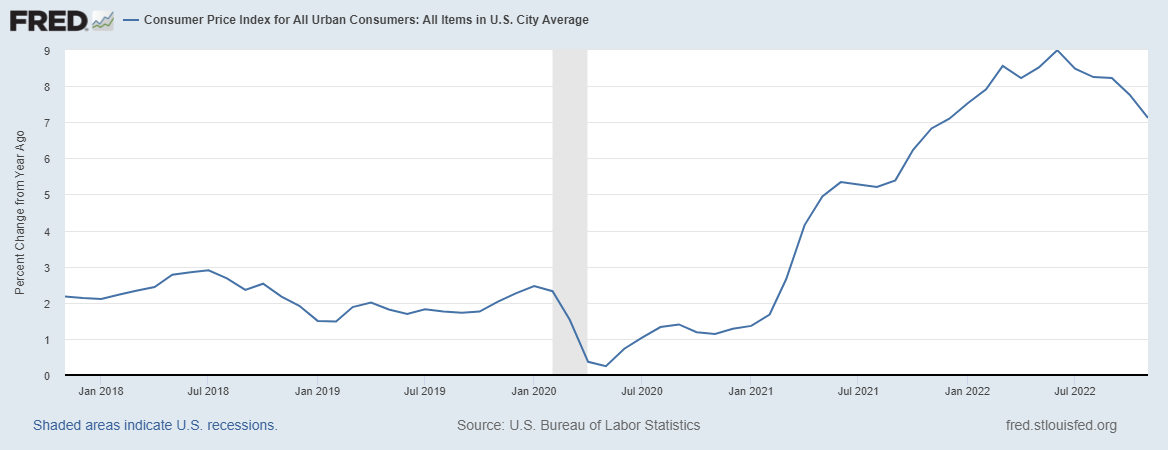

This week, we have some crucial data lines; they will come out on Thursday morning with the Consumer Price Inflation data and jobless claims. Inflation levels are still historically high, however the growth rate of inflation should slow down over the year.

The chart below tracks the Consumer Price Index and as we can see, it peaked in 2022 and it’s slowly moving lower now. The Federal Reserve has cautioned everyone not to read too much into the positive data that inflation is falling. However, if this trend continues, mortgage rates won’t be spiking higher.

Regarding the Fed pivot, although everyone talks about it, it’s a no-go until jobless claims break over the 323,000 level on a four-week moving average. Right now we are nowhere close for that level to break. Jobless claims fell in the most recent report, and the headline number fell to 204,000, while the four-week moving average is 213,500. Therefore, I don’t expect the Fed’s language to change much until the labor market breaks.

Continuing claims is another important weekly data line to track: it shows Americans who have filed for jobless benefits but haven’t been able to find a job in over a week. This number stabilized in the last report, but it has had a more noticeable rise than initial claims.

How these data lines hold up is critical to the mortgage rate/bond yield discussion. If the bond market is getting a whiff that inflation has peaked, imagine how it will act when the labor market breaks negative. Traditionally, post-1982, this means bond yields — and mortgage rates — will go lower.

To sum it up, inventory is falling like it usually does at this time of the year, but some of that inventory can be tagged to the current better demand from lower mortgage rates. In time, we should see the spring seasonal increase; if we don’t see that this year, that is a double net negative for the housing market.

Seasonal increases are the norm each year outside of 2020 because of COVID-19. I’m a big fan of getting inventory back to 2019 levels to have a buffer if rates fall and demand gets better, which would take inventory lower.

On the economic front, it’s inflation and labor; the inflation data looks like it has peaked, but the jobs data is still solid. We have a double treat this week, with inflation and labor data both coming out at the same time Thursday morning.

If you haven’t checked out my 2023 forecast, read that here. Also, I’ll be joining Altos Research President Mike Simonsen for a virtual Housing Market Update on Feb. 6.