On Tuesday, the U.S. Census Bureau released their report for March, showing a solid number of housing permits and starts — but these were boosted by multifamily construction. In addition, this data lags behind the current reality of a housing market dealing with much higher mortgage rates.

The previous month’s data were revised higher; on the surface, this is a favorable report with 1.873 million housing permits and 1.793 million housing starts. As you can see, since 2020 demographics has been driving the need for shelter for both the homebuyer and renter.

Now for another dose of reality. Housing competitions have gone nowhere for years, and this data line currently doesn’t reflect the big move in mortgage rates. As I wrote in the summer of 2020, what can cool down housing is a 10-year yield above 1.94%; currently, we are at 2.92%.

At the same time, I welcome the higher mortgage rate story to create balance in the existing home sales market, which is still showing negative year-over-year inventory data. I realize how builders react to higher mortgage rates, taking a more cautionary tone toward the single-family construction data.

From Census:

Privately‐owned housing starts in March were at a seasonally adjusted annual rate of 1,793,000. This is 0.3 percent (±12.3 percent)* above the revised February estimate of 1,788,000 and is 3.9 percent (±8.9 percent)* above the March 2021 rate of 1,725,000. Single‐family housing starts in March were at a rate of 1,200,000; this is 1.7 percent (±12.3 percent)* below the revised February figure of 1,221,000. The March rate for units in buildings with five units or more was 574,000

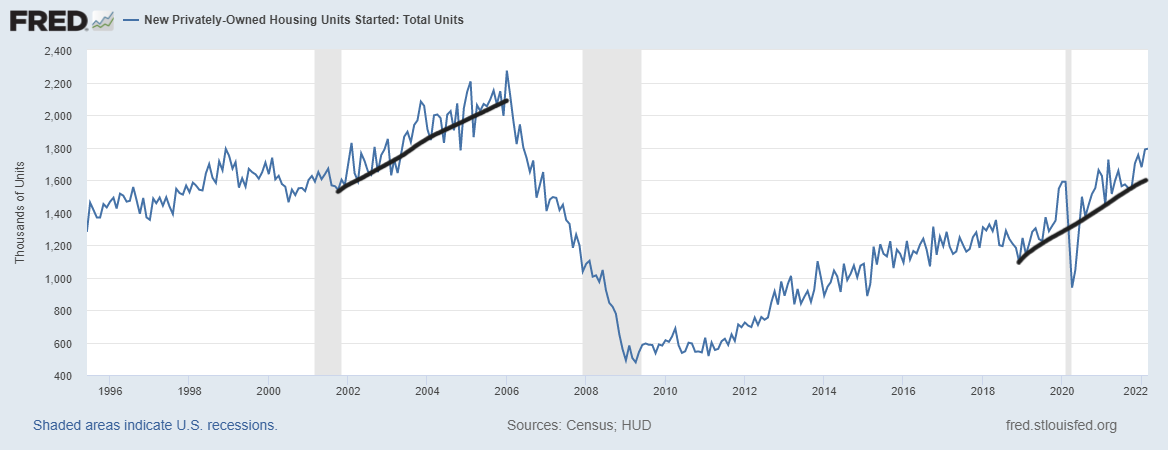

As you can see below, the housing starts data have been in a solid uptrend from the lows in 2018. I often talk about the 2018 housing market because the builders showed stress in their business when mortgage rates hit 5%, which created a supply shock for them. As you can see, housing starts started to fade at that point.

However, mortgage rates fell in 2019, and the builders were back at it. With the boost in demand for apartments and growth in new home sales from the 2018 lows, you can see why the starts data looked positive. Remember, no matter how much the builders complain about labor, cost, etc., they will build it if they can make money.

From Census:

Building Permits:Privately‐owned housing units authorized by building permits in March were at a seasonally adjusted annual rate of 1,873,000. This is 0.4 percent above the revised February rate of 1,865,000 and is 6.7 percent above the March 2021 rate of 1,755,000. Single‐family authorizations in March were at a rate of 1,147,000; this is 4.8 percent below the revised February figure of 1,205,000. Authorizations of units in buildings with five units or more were at a rate of 672,000 in March.

We can see in housing permits data that it’s been literally a roller coaster since COVID-19 happened. Housing starts data, like new home sales data, can be very wild month to month, so the trend is all that matters with the revision data.

Before rates rose, the data line looked good, but now we have a material change in the housing story so we need to look at the market with a different lens.

From Census:

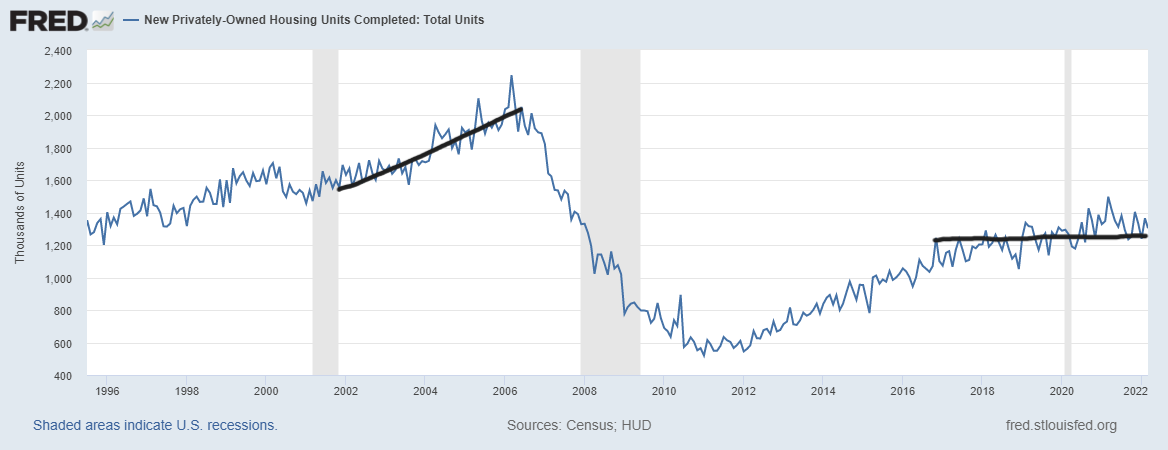

Housing Completions: Privately‐owned housing completions in March were at a seasonally adjusted annual rate of 1,303,000. This is 4.5 percent (±11.3 percent)* below the revised February estimate of 1,365,000 and is 13.0 percent (±9.8 percent) below the March 2021 rate of 1,497,000. Single‐family housing completions in March were at a rate of 1,000,000; this is 6.4 percent (±10.7 percent)* below the revised February rate of 1,068,000. The March rate for units in buildings with five units or more was 292,000.

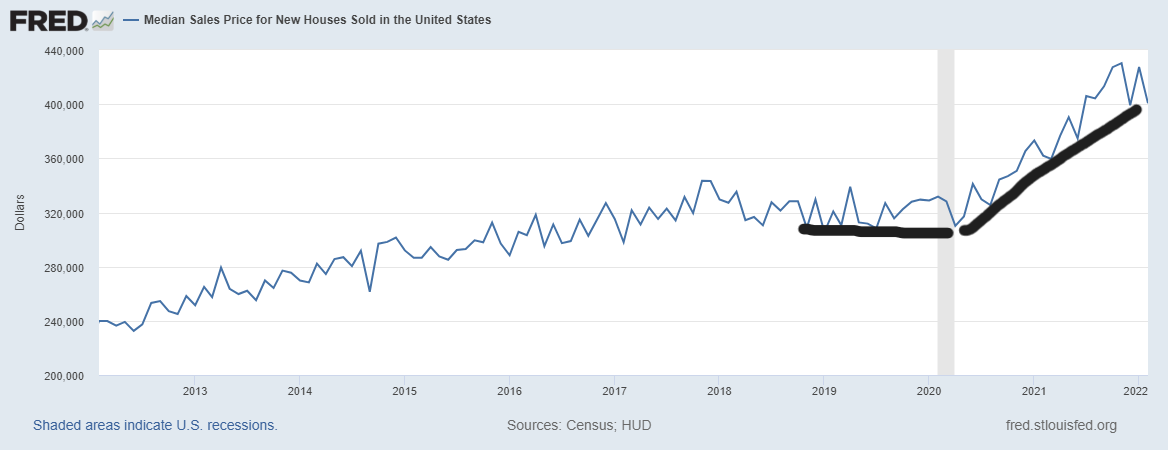

My premise that this is a savagely unhealthy housing market isn’t all about the lack of homes to buy, which creates harmful home-price growth. It’s also about the fact that the housing completion data in America looks just dreadful. Out of all the times in U.S. history for this to happen, it happens in 2020-2024.

As you can see below, this is an apparent historical deviation from what we typically see in the housing market; when housing starts and permits rise, completions follow along. Now, completions are acting like a stubborn dog who doesn’t want to be walked by its owner on a hot day. It is what it is; we have to deal with this reality until the production completion timeline gets faster.

Now the problem is that people who bought a new home with a 3% to 3.25% mortgage rate are looking at a mortgage rate of 5% to 5.25%. That is a meaningful change of rate and cost for a home. Part of why I say we need balance in the housing market is that higher rates should check home sellers, but also should check the builders, who have used their pricing power to boost their margins.

A balanced housing market is a good housing market. When pricing gets out of hand —as we have seen in 2020, 2021 and 2022 — it facilitates a stressful housing market that doesn’t do anyone any good.

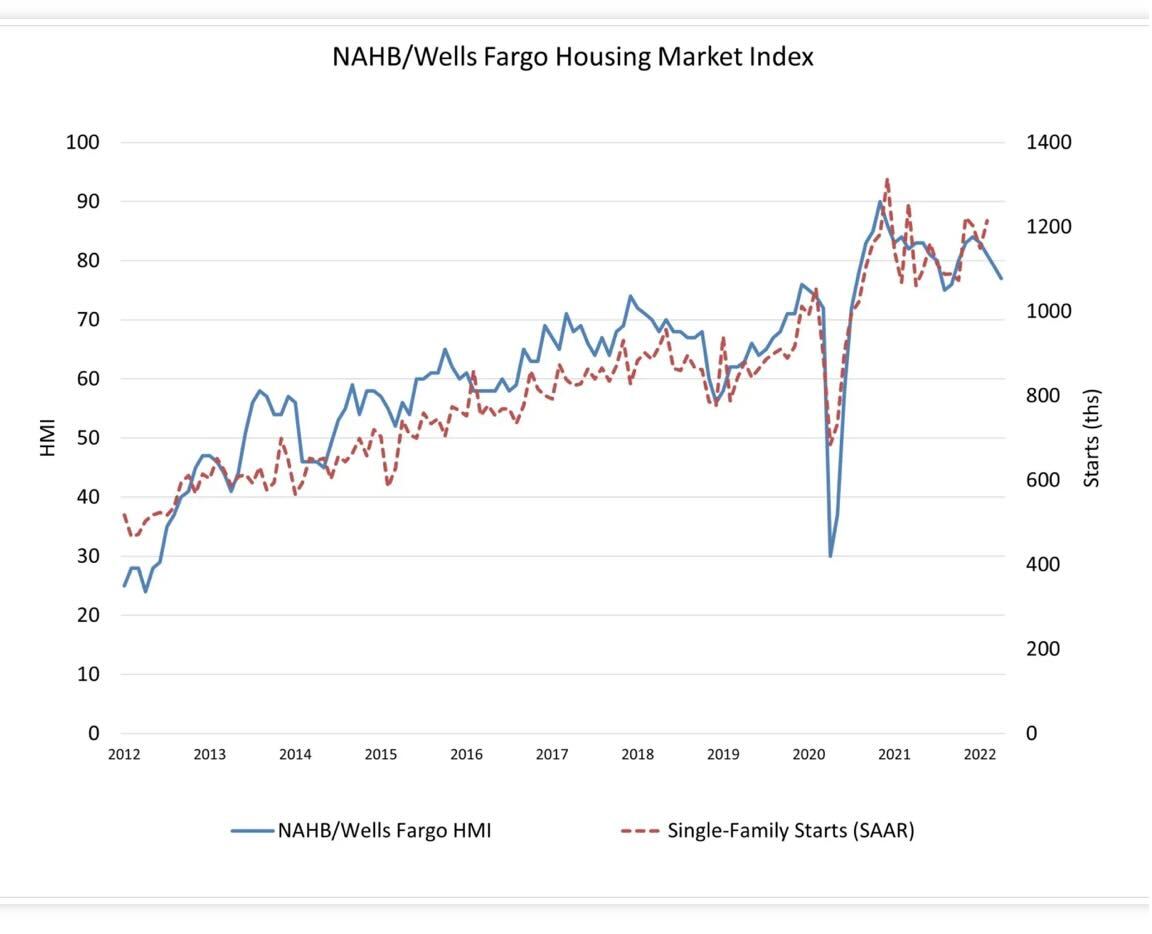

The builders are mindful of what can come in the future with cancelation rates rising, so they will be more cautious about single-family construction. This is perfectly normal behavior, so don’t fall in love with the premise that the builders will close their eyes and build when demand gets softer; that is not how they roll. This is a business to make money, not a charity case. It is important to pay attention to the builder’s confidence index, which has faded slightly.

From the NAHB:

https://eyeonhousing.org/2022/04/housing-market-at-inflection-point-as-builder-confidence-continues-to-fall/

Overall, the housing starts and permits data looks fine, but this data is backward-looking. The completion data keeps an overhang of supply for the builders who are now in the process of dealing with the threat of cancelations of those homes and deciding how much demand there is for their product with rates over 5%.

Remember, we always want to be the detective, not the troll. We will go over the economic and housing data together and deal with all the positive and negative variables than come into play.