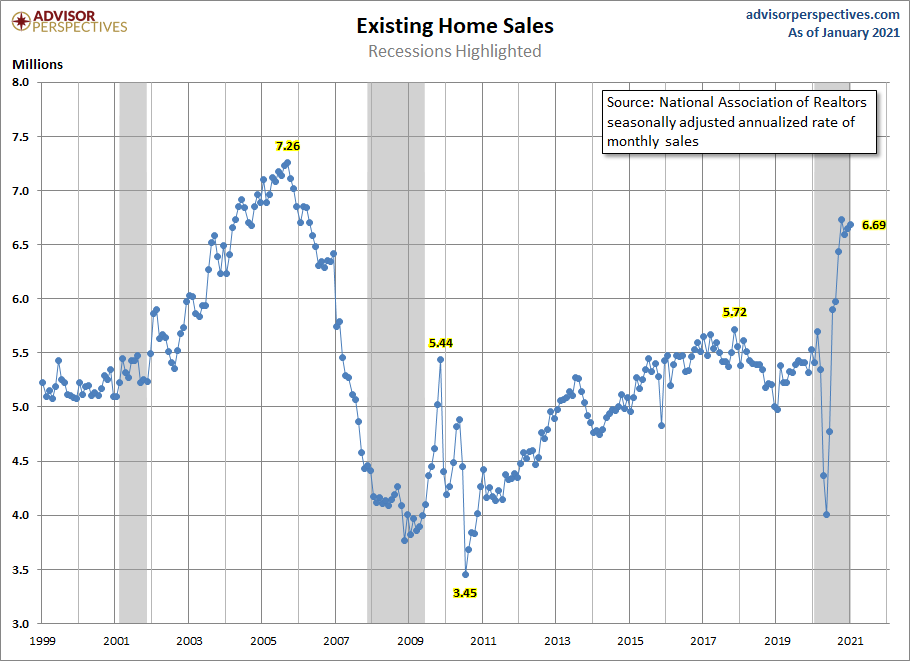

The National Association of Realtors reported that existing home sales for January were at 6,669,000, which beat estimates. The year-over-year growth was an impressive 23.7%. The median sales price also jumped 14.1% year over year, which I warned could happen during the years 2020-2024. On a recent HousingWire podcast, I discussed the need for higher mortgage rates to cool down this growth rate.

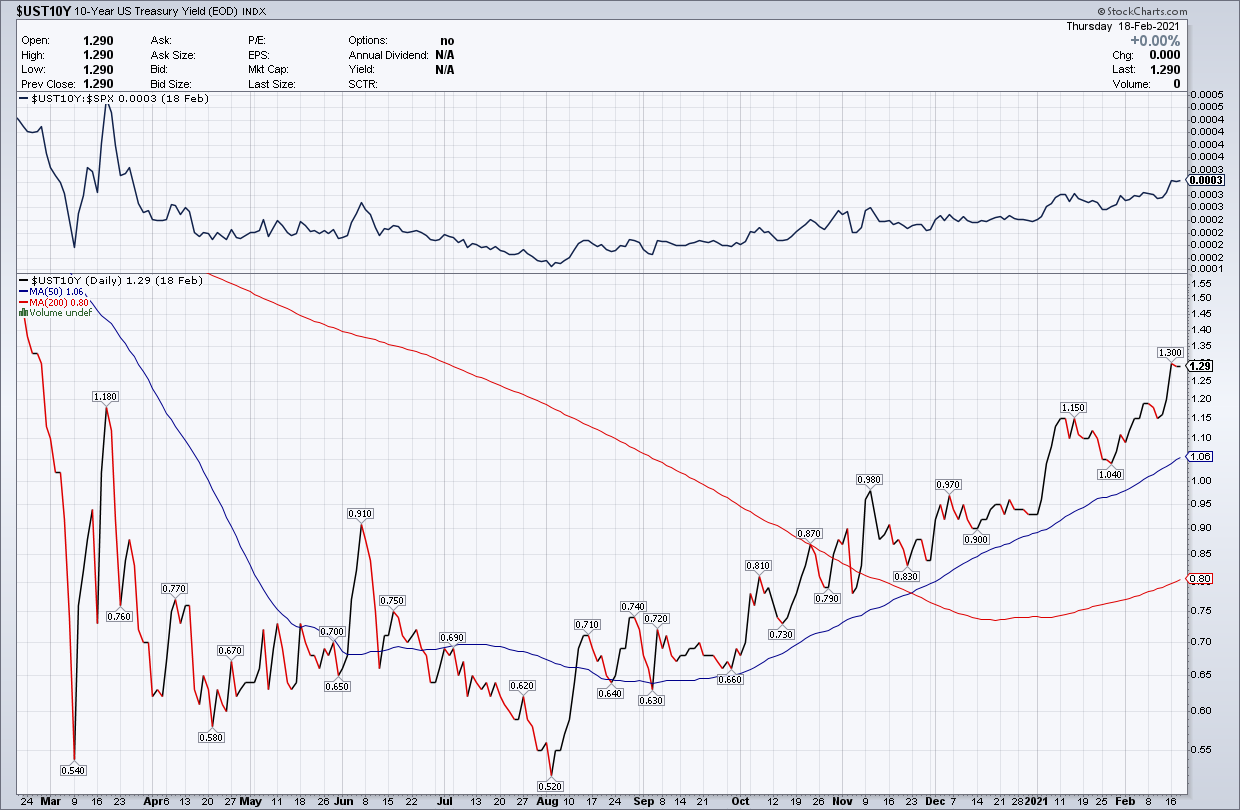

Currently, the 10-year yield is 1.35%, which is now above a critical level that I have talked about for some time. We should all be jumping for joy as the bond market shows the American bears that America is back. Mortgage rates should also creep higher. When the 10-year yield gets into the range of 1.33%-1.60%, we will have achieved our goal for the “America is Back” economic model that I proposed last year, which I believe could only happen in 2021.

With the yield in that range, we can expect the mortgage rate to move up toward 3.375%. We still have a lot of work to do to earn the right to create this range in the bond market; the first would be hitting 1.60%, which we haven’t yet. The chart below shows the 10-year yield as of the close of Thursday. Today, bonds are selling off and yields are higher.

Mortgage rates are still meager, historically speaking, but 3.375% or higher may be enough to slow the home price growth rate – which, right now, is simply too hot. The days on the market went from 43 days last year to 21 days currently.

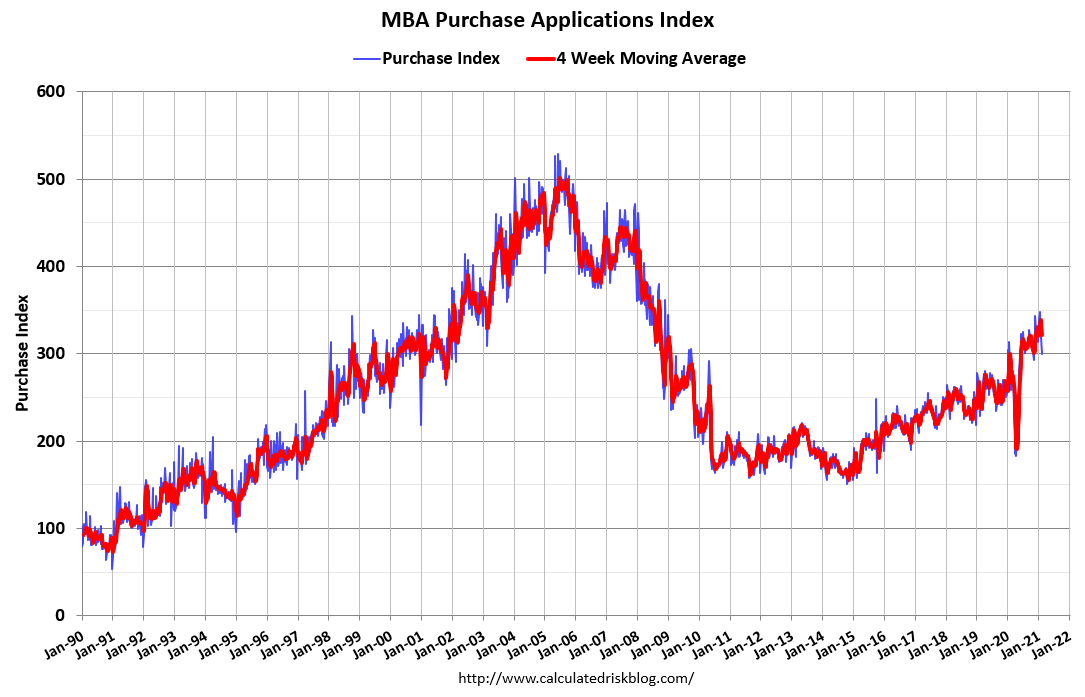

So far this year, the MBA purchase application data is running stronger than even I thought. This metric is a predictor trend of demand 30-90 days out. I believed the peak rate of growth in purchase applications would be around 11% year over year up until March 18th. It is trending at 13.1% this year, so we are off to a good start for 2021.

New home sales, existing home sales, and the builder’s confidence index that went parabolic towards the end of 2020 have stopped going up and started to fall. The last report on new home sales shows that housing data moderates and moves back to the trend.

The monthly sales prints for existing home sales show that this metric has stopped its parabolic move higher, but it still has not moderated enough. We still have not completely made up for the lost sales in 2020 due to COVID-19. We should have ended 2020 with 5,710,000 -5,840,000 in existing home sales but only realized 5,640,000. This number is only 130,000 higher than what we had in 2017, so this isn’t the booming speculative buying we saw during the height of the housing bubble years.

Once this makeup demand is exhausted, existing-home sales should moderate toward 6.2 million or even lower to get back to the trend. If existing home sales stay above 6.2 million on the monthly sales print for the entire year, we can consider the demand to be even better than expected.

For the rest of the year, the single most important and healthy event for the housing market would be higher mortgage rates to cool down home prices’ growth rate. We will see if mortgage rates rise high enough to cool demand and reduce the multiple bid situation we currently have in many markets.

Nobody wins when the housing market is too hot – not even sellers because they will need to find somewhere else to live. We have enough supply to grow sales to pre-cycle highs, but when choices are limited, the willingness to sell and move becomes less attractive.