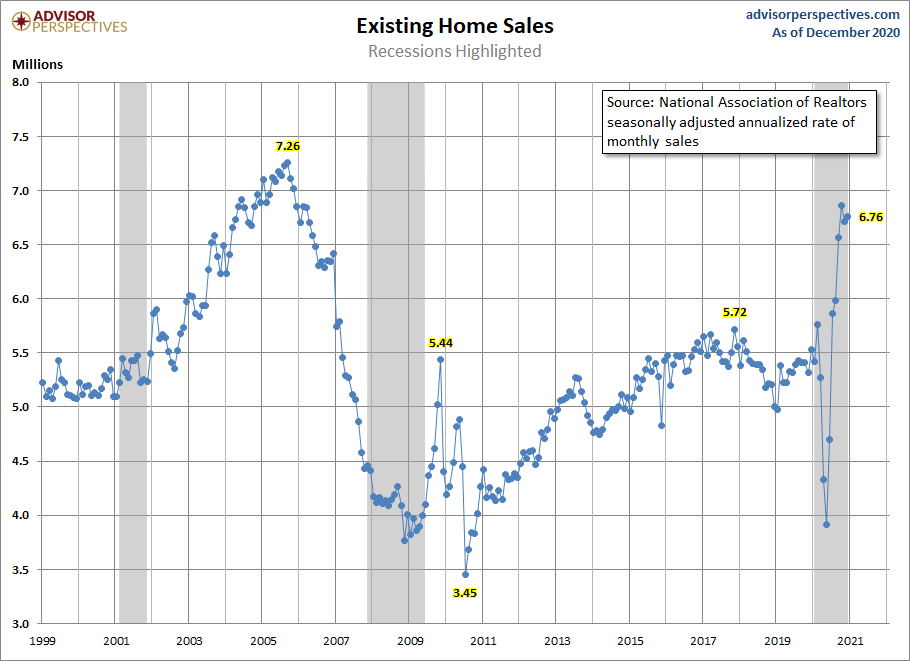

The National Association of Realtors reported existing home sales for the month of December were at 6,760,000, a beat of estimates. This also closed the books on 2020’s housing market as we finished out the year at 5,640,000 total existing-home sales — a 5.6% increase from the same month in 2019.

Instead of thinking of the end of 2020 and going into 2021 as a hot sales market, this increase over December 2019 sales may be more appropriately interpreted as an end-of-the-year bump due to “make-up sales” for sales missed during the COVID shutdown in the spring of 2020.

The COVID crisis of 2020 was responsible for a lot of abnormal metrics in the housing market. Data lines that are typically very sticky, i.e. take months to move significantly in either direction, took waterfall dives, and then made parabolic recoveries — the existing home sales numbers are an extreme case of this.

When I think about the 2020 housing market, the big take-home is not the V-shape recovery in many of the housing metrics or even the hotter-than-expected price growth. The big take-home is that 2020, despite the COVID crisis, began a period in our country (the years 2020-2024) when we have both the best housing demographics ever combined with mortgage rates low enough to keep housing stable for years to come.

We saw hints of this prime housing market period as early as February of 2020. The existing home sales report at that point was trending at 300,000 above my highest sales range for the year. To a casual observer that might not seem like a big deal, but February was the biggest single month in housing this century in my view – and the start of things to come.

During the summer of 2020, I wrote that, based on the February existing-home sales data, if we didn’t end the year with 5,710,000 – 5,840,000 in existing home sales then, it would be because the COVID crisis prevented some sales from happening. I believe we are still making up for lost demand and this is why the monthly sales data are still so high. This means that we can expect existing-home sales data to moderate in the coming months, even getting back to 6,200,000 on these monthly prints, once this makes up demand is exhausted.

The key is not to overreact to this drop. If we don’t get to 6,200,000 or lower in the 2021 monthly sales print, then demand is better than I thought.

Also covered in the NAR report was housing inventory. Inventory is at all-time lows of 1.9 months. For context, inventory does tend to fall toward the end of the year and stay low until spring. However, even accounting for that we are at all-time lows. Compared to the previous year, days on market fell dramatically from 41 days to 21 days. Cash buyers and sales to investors also fell compared to the same month of the previous year. Mortgage demand picked up in 2020.

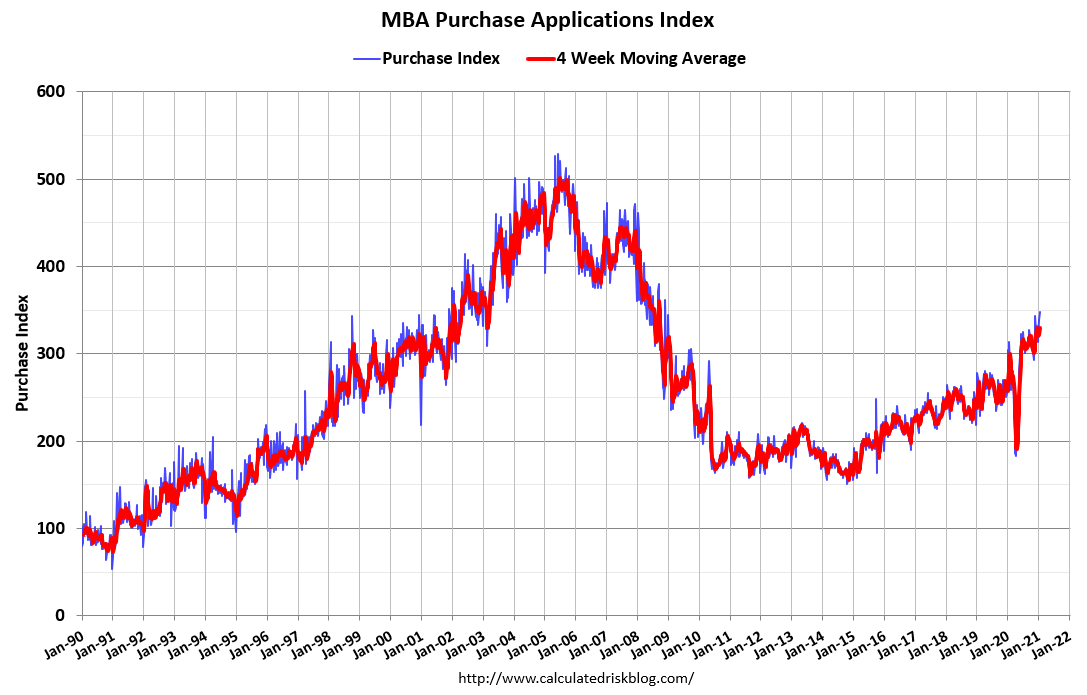

The MBA’s purchase application data for the last three weeks have shown nothing but positive growth compared to the same period last year. This week’s report has shown growth of 15%, and the previous two 10%, and 3%. I am looking for trend growth to be between 1%-11% year over year so for now, everything looks about right. Anything above 11% trend growth I would considered housing is outperforming again in 2021.

Just remember that the year-over-year data is going to look abnormally strong after March 18 because that was the period last year when the market was essentially frozen due to COVID. So, adjust your take on housing to those nine weeks after March 18. All in all, this report shows a good year in 2020, even with COVID-19, mother demographics and low mortgage rates prevailed.