Mortgage rates fell slightly this week, according to Freddie Mac’s latest Primary Mortgage Market survey.

“This stability is much needed for home sales, which have crested because of the multi-year run up in prices, tight affordable inventory and this year’s higher rates,” Freddie Mac Chief Economist Sam Khater said. “Going forward, the strong economy will support the housing market, but with affordability pressures mounting, further spikes in mortgage rates will lead to continued softening in home price growth.

A recent report from Fannie Mae revealed that both renters and homebuyers feel pessimistic about affordable housing availability, which could potentially explain the 3% drop in mortgage applications according to the Mortgage Bankers Association.

“There continues to be a steady rate of job creation, but as we’ve seen throughout most of this economic expansion, wage growth is not meaningfully increasing above inflation,” Khater added. “With home prices still climbing and mortgage rates up from 3.9% a year ago, some prospective buyers are definitely feeling an affordability crunch.”

According to the latest Employment Situation Summary report from the U.S. Bureau of Labor Statistics, jobs continued to increase in July, dropping the unemployment rate to 3.9%. However, Americans still have not seen a significant increase in their wages.

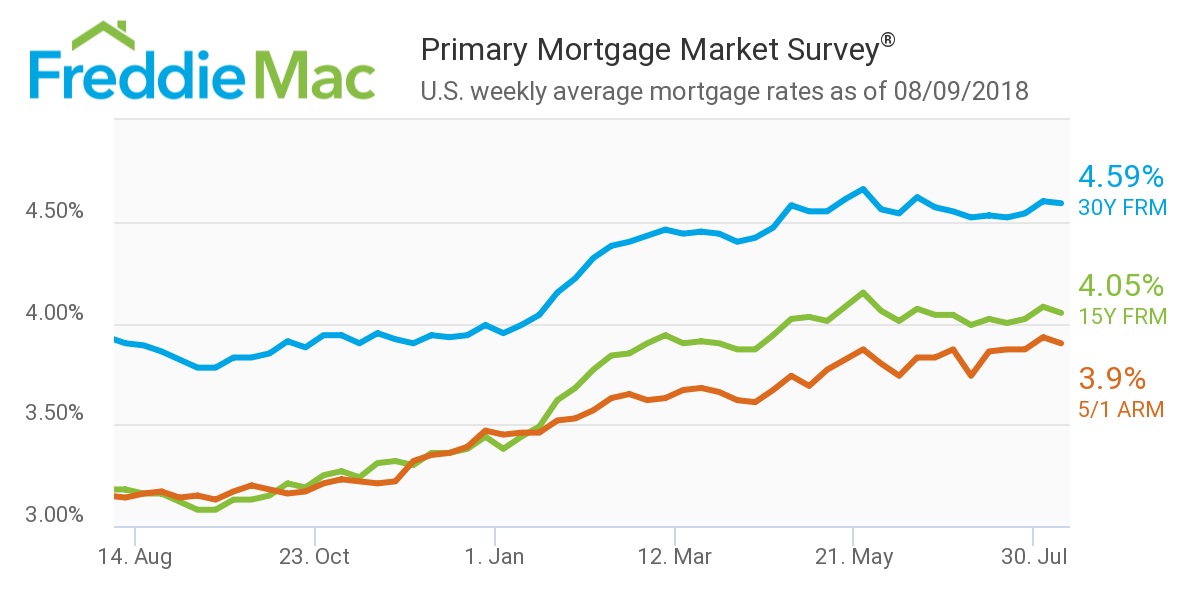

(Source: Freddie Mac)

According to the report, the 30-year fixed-rate mortgage averaged 4.59% for the week ending August 9, 2018, down from 4.60% last week, and up from 3.90% last year.

The 15-year FRM inched backward to an average 4.05 this week, down from last week when it averaged 4.08%. This time last year, the 15-year FRM was 3.18%.

The five-year Treasury-indexed hybrid adjustable-rate mortgage averaged this week at 3.90%, down from 3.93 last week, but still up from this time last year when it was 3.14%.