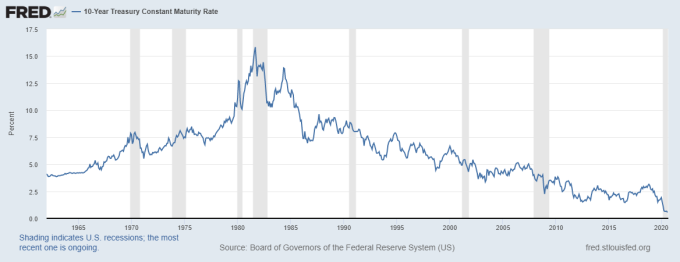

Since 2015, my forecasting models have predicted the 10-year Treasury yield would stay in the range of 1.60% to -3%. Tangential to this, the next recession treasury yields, and thus mortgage rates, would drop because lower growth would drive yields and rates lower. The four-decade prolonged downturn in the rate of growth in the economy and inflation mirrors falling bond yields and mortgage rates.

Before the pandemic, it was hard work trying to convince other economists that we would see a 30-year fixed mortgage rate drop below 3%. In 2018, a crafty photographer caught the bemused look on my face when one of my colleagues chastised me for predicting rates would go lower instead of higher.

Evangelizing a consistent thesis for years on end is a bit boring, but I would rather be dull and steady than the alternative. I admit I am a big fan of sticking to economic models that allow for reliable predictions, repetitive as they may be, until different variables change the course of the economy.

Today, in the middle of a world pandemic, my bond market model is allowing for a 30-year fixed mortgage rate to drop as low as 1.875% – but the questions remain, will it, and what will it take to get there?

Earlier this year, before the 10-year yield broke under 1%, I wrote about the one thing that could drive yields lower. In an article for HousingWire published on Feb. 3, I invoked chaos theory and the butterfly effect to explain how a virus outbreak in a faraway country could drive stocks, bonds, and GDP down in the US.

For Bankrate.com, before the 10-year yield broke under 1%, I predicted that recessionary yields would be in the range of -0.21% – 0.62%. Yes, that is a negative 10-year yield.

In the previous economic cycle, GDP went negative three times, and each time the dip was quickly reversed. It took a pandemic, the most significant health and financial crisis in recent history, to put the U.S. into a recession. It wasn’t systemic problems but an outside force that led to the collapse of the economy.

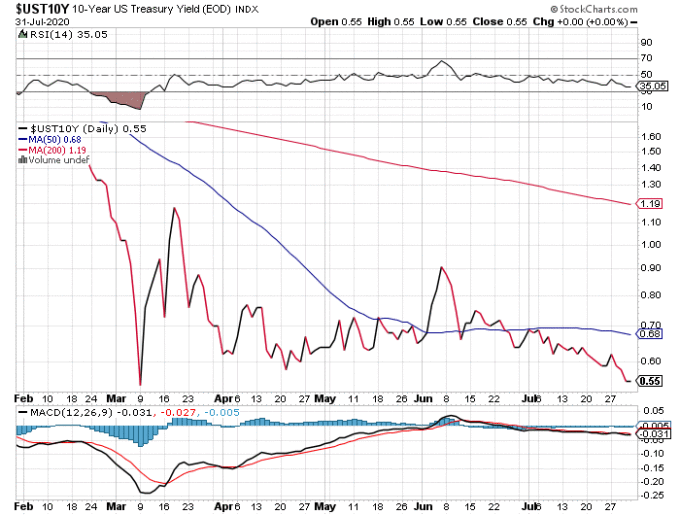

On Monday, March 9, the morning print for the 10-year yield was 0.34%. Then a massive stock market sell-off created margin selling of the bonds, which took the yield back above 1%. Since then, bond yields retreated lower to 0.53% as of last Friday. For the most part, it has been trading above 0.62% until recently as the market waits for another disaster relief package.

Even with these historically low yields, we still have fixed mortgage rates drop below 3% but not below 2%. The question remains: What would it take to get the 10-year low enough to get a 1.875% mortgage rate on a 30-year fixed?

First and foremost, we would need to see negative yields stick with duration. The spread between the 10-year and mortgage rates has been wider during this crisis, as banks were dealing with their own mortgage market meltdown in March and April and needed time to rebalance their books. Only recently, mortgage rates have been getting better but still should be lower today.

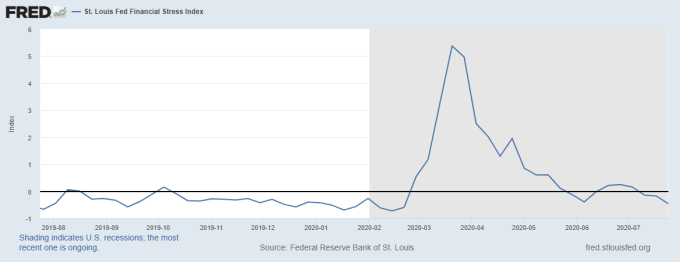

Can we expect to see negative yields with duration? The short answer is not likely, and here’s why. The U.S. economic data is getting better, and I am not just talking about the V-shaped recovery in housing. Control retail sales showed one of the best year-over-year growth prints since the year 2000. Manufacturing survey data is positive (be skeptical about PMI data for now), and the St. Louis Financial Stress index just hit a new Covid19 low at a – 0.4612%, zero is considered normal stress.

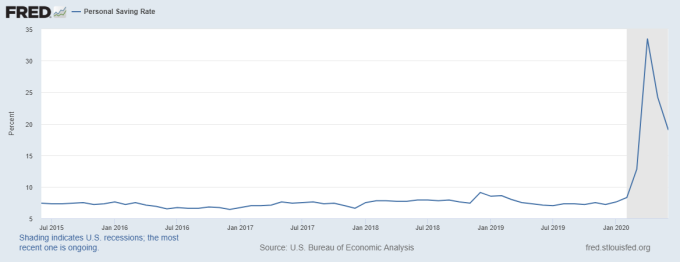

Additionally, while we still have high unemployment, we also have a savings glut due to the CARES Act and a lack of spending options early in the crisis. As retail sales grow, the personal savings rate has fallen.

Other economic data lines are also showing improvement to the extent that we are likely seeing a rebound in the GDP in the next quarter. Also, the government, both on the fiscal and monetary side, is well embedded into the economy now in August. This is much different than what happened in March. Also, the initial fear of having a virus pandemic and not knowing what was going on in March and April is slowly leaving us.

For us to see mortgage rates drop below 2%, we would need to see a retracement of many data lines that are showing the first glimmers of economic recovery. These are the factors that could drive this to happen:

1. The U.S. government stops or significantly reduces fiscal stimulus.

2. A stock market sell-off again. Since the market is near all-time highs, a pullback is not unlikely.

3. Credit stress rises again. This is a certainty if the government does not continue with its fiscal stimulus programs.

4. A terrible winter that increases infection rates and deaths. This is the wild card for America right now. We made good progress on flattening the curve initially, and then we got sloppy. We are trying to reopen schools, have an election, and will be dealing with the natural uptick in cases due to winter sickness. Coping with the second wave of infections this winter could seriously dampen our economic progress. (I am holding out hope that by Sept. 1 the new-case growth should be down noticeably from recent highs) From this level, we have a better footing to deal with the winter. However, we need to be mindful that winter is really coming, and this isn’t a show about dragons we can choose not to watch.

It would take a lot of bad news to push mortgage rates below 2%, and that is why I am rooting against this from happening. The AB (America is Back) economic model states that we want to see the 10-year yield above 1%. In time with more consistent growth, we will get there.

So mask up and be smart. Let’s all help this recovery take off again and hope we don’t see a 30-year fix at 1.875%.