With COVID infection rates exploding and hospitalization rates rising as we go into the cold winter months, the risk this poses to our recovering housing market is a question that should be addressed. In a previous article, I identified infection rates during the winter months as one of the economy’s high-risk variables.

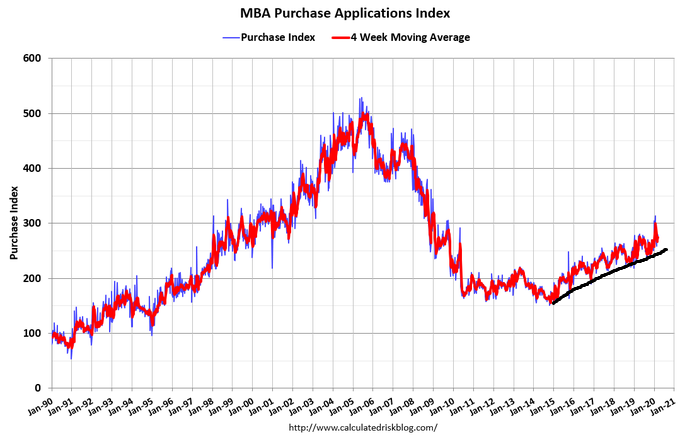

Before COVID-19 hit our shores, we were trending at 10% growth, working at cycle highs in demand. The housing heat months for the MBA purchase application data are from the second week of January to May’s first week. Typically, after May, total volumes fall as seasonality kicks in. We had double-digit growth until March 18.

Then COVID-19 hit and we had nine consecutive weeks of year-over-year declines. The fear of the virus, the stay-at-home orders, a collapsing stock market and a rising financial stress index all played a part in the market’s rapid decimation. Four weeks into the decline, the market stabilized, and the rate of decline stopped, then began to recover over the next five weeks.

We eventually turned positive on a year-over-year basis and got a true V-shape recovery, despite all the Housing Bubble Boys’ protestations calling for a crash. You may have heard whispers about a “W-shape market,” meaning a decline after the recovery. But instead, we have had 25 straight weeks of year-over-year growth, averaging over 20%.

I expected the year-over-year purchase application data growth to be moderate, but so far, it has continued on its 20% year-over-year growth trend for 25 weeks. Much of this growth can be ascribed to make-up demand for the nine weeks of declines we saw in the traditional heat months. Total volumes that would typically fall after May are finally showing some of the common seasonality factors with this data line.

In November and December, the year-over-year growth should moderate , and the surge in cases could assist in this moderation.

For the last six weeks, purchase applications have been up by double digits compared to 2019. Remember, this metric is forward-looking by 30-90 days.

+16

+25%

+24%

+26%

+24%

+22%

We always want to keep an eye on the year-over-year growth data. But, with rising cases and more restrictions being put in place, the question remains whether the housing market will be negatively impacted in the short term.

How much house can I afford to buy?

For many, the homeownership journey logically begins by trying to figure out how much house you can afford.

Presented by: Citi Mortgage

The answer is, yes, it could be negatively impacted, but two factors will keep it from looking like it did in late March and April.

First, we’ve all been here before. For the most part, we are no longer prone to panic when infection rates rise. As a country, we are learning to consume goods and services with an active virus infecting and killing Americans every day. We are not hoarding toilet paper or hunkering down in our homes, afraid to open our computers and check out what is on the market.

And second, COVID tests are more widely available, treatment for infections show great promise, and effective vaccines appear to be just around the corner.

For these reasons, the virus and society have reached a kind of detente. We still need to be wary and careful, but we no longer have the energy to maintain strict vigilance. Also, the raw shock and fear of having an active virus come into our economy, which was working from the longest economic expansion ever recorded in history, can’t be replicated.

Higher infection rates and the resumption of shut-down protocols can drive growth into single digits compared to last year, but we should still see growth.

Low mortgage rates and the most prolific housing demographic patch ever in U.S. history (ages 26-32 are the biggest in America) will soften any downturn in the market due to COVID-19. Next year, a vaccine and better treatments — once distributed — will have confidence roaring back.

The financial markets appear to agree with my assessment that housing and the economy will remain stable, despite the recent COVID-19 surges.

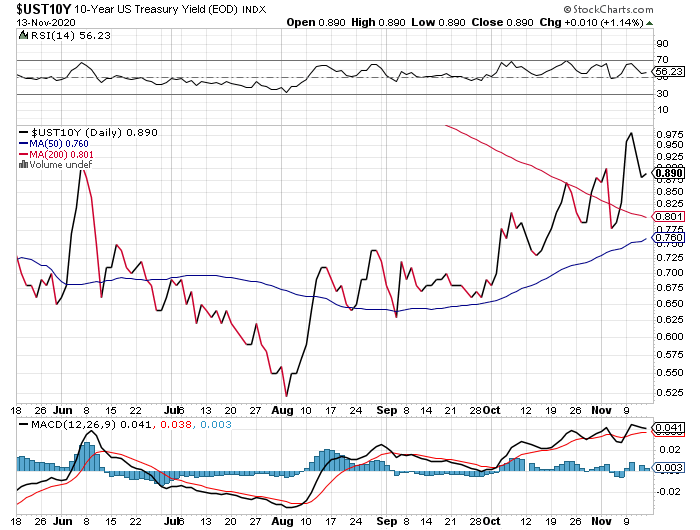

Last Friday, the stock market hit an all-time high, and last week the 10-year yield hit a recent high of 0.98% — a mere 2 basis points away from checking off the last variable of the America is Back (AB) model.

On March 9 2020, the bond market was trading at 0.32%. We are a long way from those fear-ridden days. Friday’s close showed confidence in a better future as wonderful news on an effective vaccine hit the wires last week.

Another measure of confidence, the St. Louis Financial Stress Index, has been declining after the initial spike earlier in the year. The index is currently at -0.3909%. Anything below zero indicates confidence in the financial markets. As long as this stays below 1.21%, we should be OK.

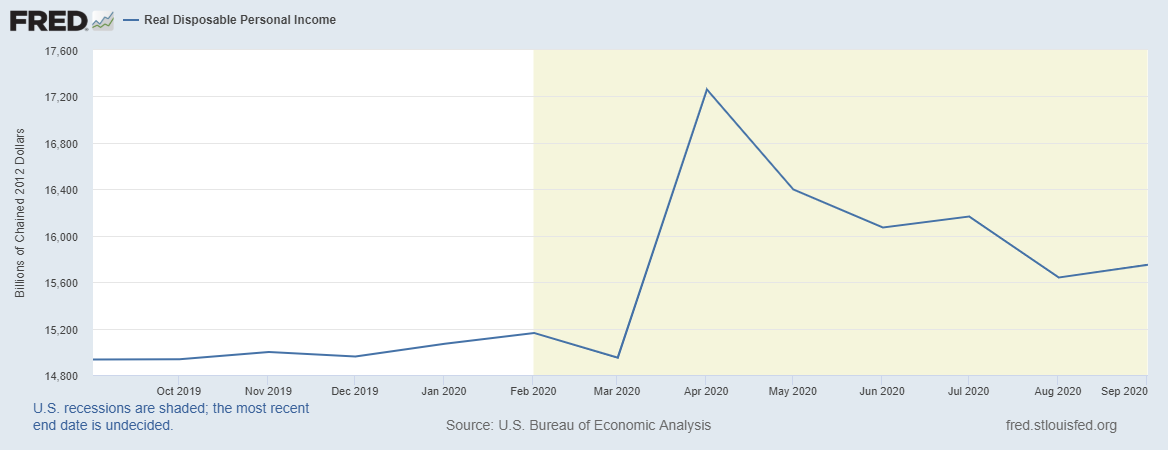

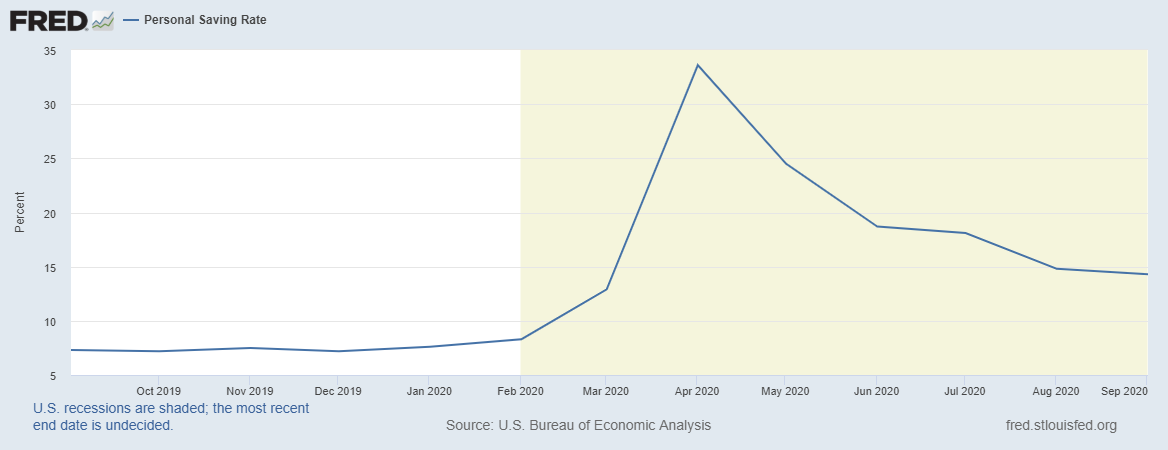

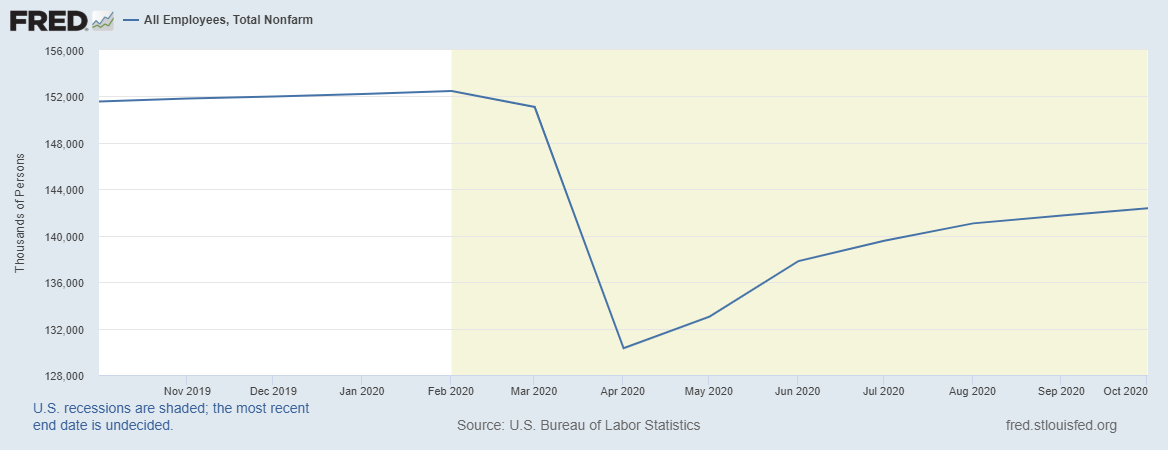

The bond market, the stock market, and stress indicators all held up OK with the second surge of infections we had a few months ago. So far, they have also held up during the current surge with winter coming. We still have higher real disposable income levels and savings rates than the pre-COVID-19 era. Any more disaster relief, which should have already happened, would just add to these positive data lines. Also, to note, we have regained 12 million jobs in the past few months.

Even if we had not experienced an increase in COVID-19 cases, I would expect housing data to moderate. The parabolic growth in some of the housing metrics isn’t normal. So we could see more moderation in the year-over-year growth for the purchase application data to bring these numbers back to the pre-COVID-19 trend.

Be careful of housing bears trying to bestow their housing crash and W-shaped theories when this occurs. Don’t get too concerned over any slowing down of the economy as long as the 10-year yield is above 0.62%. This has been my main rule of thumb since this crisis started.

We are almost through this. I still believe with my heart, mind, and soul what I wrote on April 7, 2020 – our victory may be delayed, but it is still within our grasp:

“I believe the months of April and May are going to tell an epic story of America’s start in defeating this virus. If we do this right and document the cause and effect of our efforts, future generations will be able to look to this period in time for how to handle a global pandemic. My faith in America winning has never let me down because I always believe in my people and country. I can tell you now, this virus isn’t changing my view on that.”