Can you smell it in the air? America is back! The last plank required to complete the foundation of my “America is Back Economic Recovery” model was for the 10-year yield to start trading in the range of 1.33% to 1.60%, and as of Feb. 16, this has happened. Higher treasury yields have pushed mortgage rates higher, but will higher rates cool the housing market?

We are currently administering three different effective and safe vaccines and are on the brink of reopening our economy. Added to this, the now high savings rate will likely go higher when the next stimulus checks are delivered.

Over the weekend, the Senate passed the 1.9 trillion disaster relief package, which will go back to the House of Representatives for a vote on Tuesday. We are looking at $1,400 checks being sent, six months of pandemic unemployment insurance, rental assistance, and many more disaster relief items.

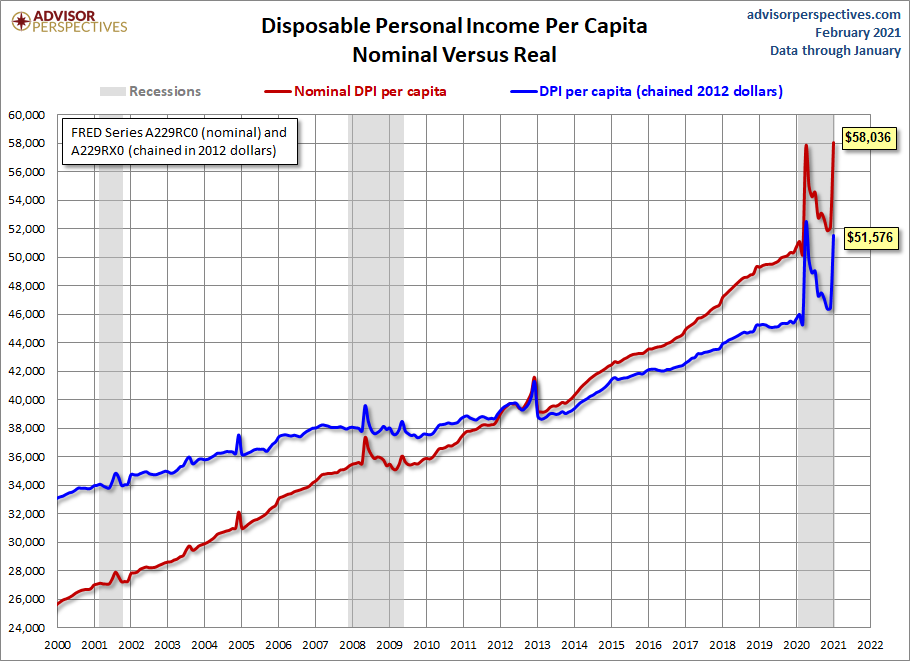

Disposable personal income per capita, too, is at an all-time high and will also get another boost shortly. We have the backdrop for a healthy amount of consumer consumption.

On top of all this, we will most likely see an infrastructure package passed, giving us another round of government stimulus at some point in the future. This will be more beneficial once we can safely walk the earth freely, which won’t be too long from now.

Once schools are open again, parents will be free to re-enter the job force: By September 2022 or earlier, we should have regained all the jobs lost to COVID-19. This is a terrible outcome for the Forbearance Crash Bros if all Americans who lost their jobs to COVID-19 get their jobs back. These positive economic factors warrant higher mortgage rates as we are no longer in recession in America. Now, we want to get all the jobs back that COVID-19 took from us.

These and other economic data lines warrant a higher 10-year yield — perhaps as high as 3% — much higher than 1.60% that is the top of our current trading range. So, we should expect higher mortgage rates, but the question is: Will that be enough to cool down the housing market?

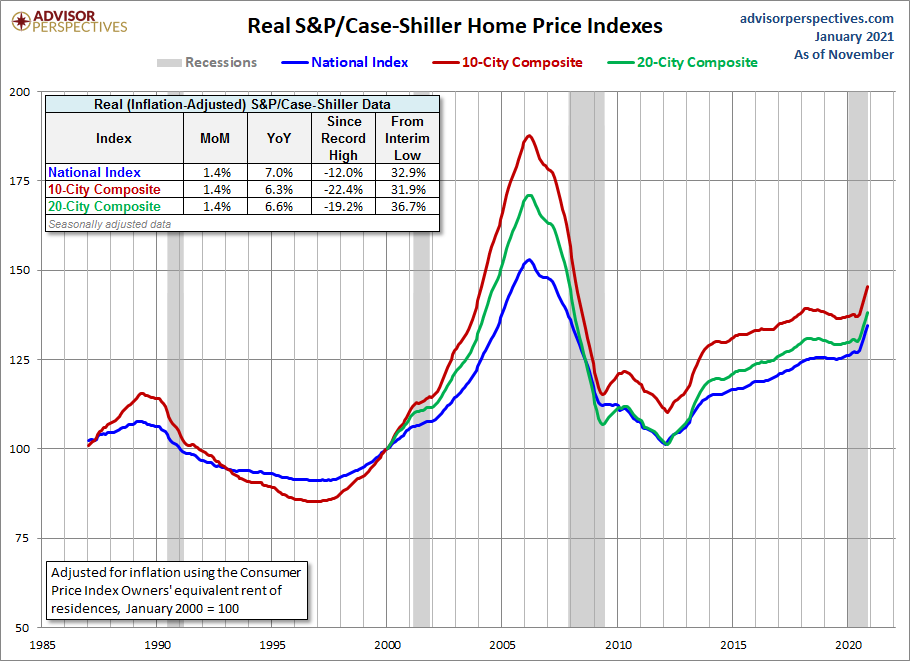

In 2013-2014, mortgage rates got to over 4%, which had an immediate suppressive effect on home-price growth. In 2018-2019, mortgage rates rose to 5%. This wasn’t high enough to bring nominal home prices negative year over year, but it cooled the existing home sales market for real home-price growth to go negative.

For 2021, I am relying on the precedent that higher mortgage rates will cool down this substantial housing demand. We should all be rooting for a cool-down to keep home prices in check. But we need to entertain the possibility that higher mortgage rates won’t be high enough to dent price growth and multiple bid situations during purchasing.

When multiple bids become the norm, home prices accelerate and begin to deviate from the trend. This type of price growth was my main concern in the years 2020-2024. This is an unhealthy housing market — not a balanced market for buyers. Even sellers are now concerned that they might not be able to purchase a home quickly once they sell their home, making the process more stressful than it needs to be. It’s not fun getting outbid, over and over again.

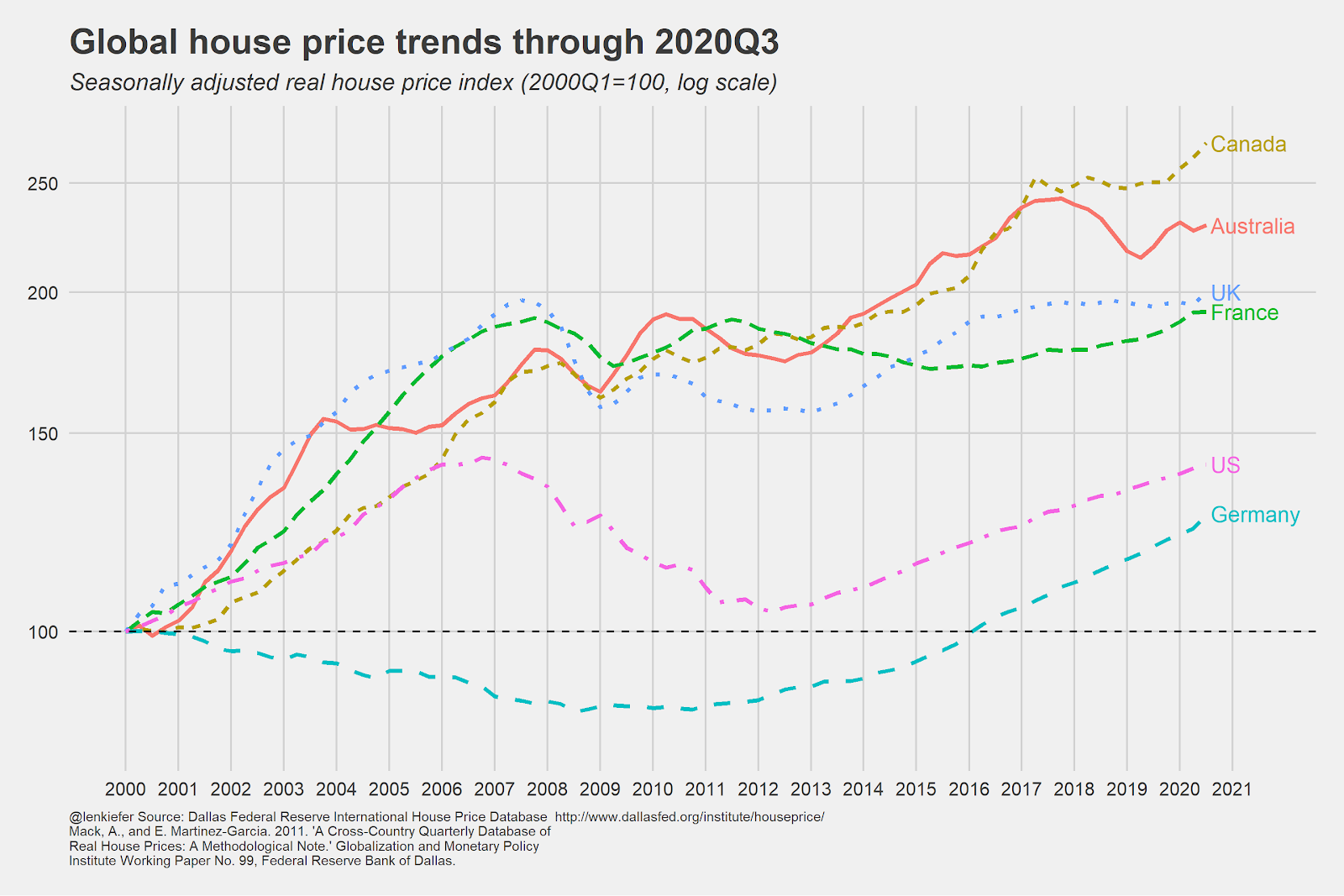

With all this talk of home-price growth, it is essential to remember that the U.S. housing market is nowhere close to the real home-price growth levels of Canada, the UK, France, or Australia. These markets have had out-of-control price growth for years now, with no bubble crash insight.

The U.S. housing market has better housing demographics (especially vs. France), so demand could be even hotter. Will the U.S. housing market go the way of these other countries by entering into years-long (or decades-long) acceleration of home prices?

From Freddie Mac economist Len Kiefer:

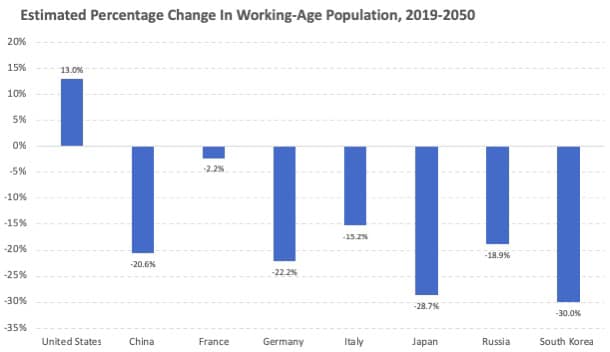

As you can see below, many countries lack working-age population growth. For us, in America, it’s not just the millennials but Gen Z too. We have a lot of people that need somewhere to live. From Census:

For another context check, remember that current real home price growth is nowhere close to what it was at the peak of 2005. Today mortgage rates are lower than they were then, and housing demographics today are better.

From 2002-2005, speculation debt was driving the housing market, and that couldn’t be sustained. In a low credit quality, debt speculative-driven housing market, we overbuilt housing in relationship to demand. We then ran into a weaker demographic patch and demand just fell off a cliff. Also, credit itself in connection to what kept market-moving along got very tight. The existing home sales data was too high, and demand started to fall from the peak of 2005, leading to the great financial crisis of 2008.

Everything that I said above is the opposite today. When we consider demographics, the excellent loan quality in the previous expansion, and the expanding jobs market, we are in the sweet sport for housing. But, with all these accelerating factors, there is reason to be concerned about real home price growth getting out of control from 2020 to 2024. Don’t forget, existing home sales only ended 2020 130,000 higher than 2017 levels, so we aren’t looking at a booming speculative home sales demand cycle.

With that said, I am still hoping that higher mortgage rates cool the housing market. Last year I talked about keeping an eye on the housing data if the 10-year yield got 1.94% or higher. That was assuming that mortgage rates would get to 3.75% and higher. Remember, since 1996, it has been sporadic to have total home sales under 4 million in a year.

We had a month here and there when the monthly home sales went under 4 million for the existing home sales market, but it is rare. People buy homes each year for shelter. It’s a necessity. Our useful demographics mean we have built-in replacement buyers, more now than any period in U.S. history. Total home sales (existing and new homes) should be 6.2 million and higher every year in 2020-2024.

But higher mortgage rates do matter, and we should welcome them in hopes that they will cool down demand. Right now, demand is too hot, and it is resulting in an unhealthy, unbalanced market that can only be moderated with higher rates.

If I am wrong and higher mortgage rates don’t cool down the housing market, and days on the market don’t rise from the current 21 days — in 2020 it was running at 43 days— then we are stuck with this price growth, which isn’t that easy to remove. We are leaving the recession mortgage rates behind us, as we should because America is back, and hopefully, this can create some breathing room in the housing market.