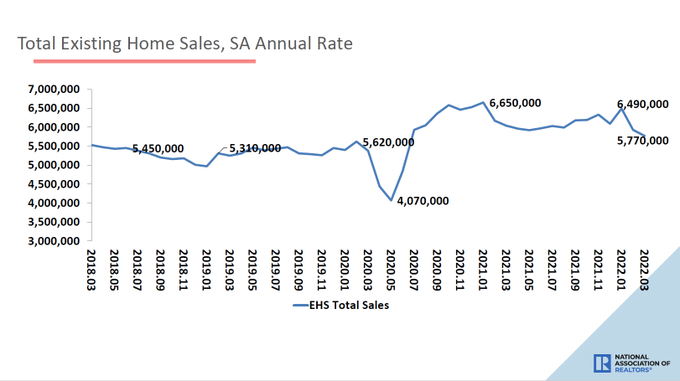

The National Association of Realtors reported that existing home sales for March came in as a miss of estimate at 5.77 million. However, the real story of 2022 is that the savagely unhealthy housing market continues as inventory is still lower than last year, sending home prices growth into double digits again. However, hope for a balanced market is real this year because, with higher rates, we should see more days on the market coming up and growth in the inventory data.

The 5.77 million sales print on Wednesday is in line with my 2022 forecast sales range between 5.74 million and 6.16 million. Last year I discussed sales levels coming back down to 5.84 million, and I am looking for more of the same in 2022, at the 5.74 million level. Like last year, I was anticipating a few prints under 5.84 million. We only got one, and the same with this year under 5.74 million.

However, unlike the previous year, we have a material change in the U.S. housing market; the 10-year is above 1.94%, something that didn’t happen in 2020 or 2021. This means higher mortgage rates, so we need to talk about the housing market in a rising-rate environment without going into housing crash mode like the professional grifters do for clicks.

From NAR: Total existing-home sales dipped 2.7% from February to a seasonally adjusted annual rate of 5.77 million in March.

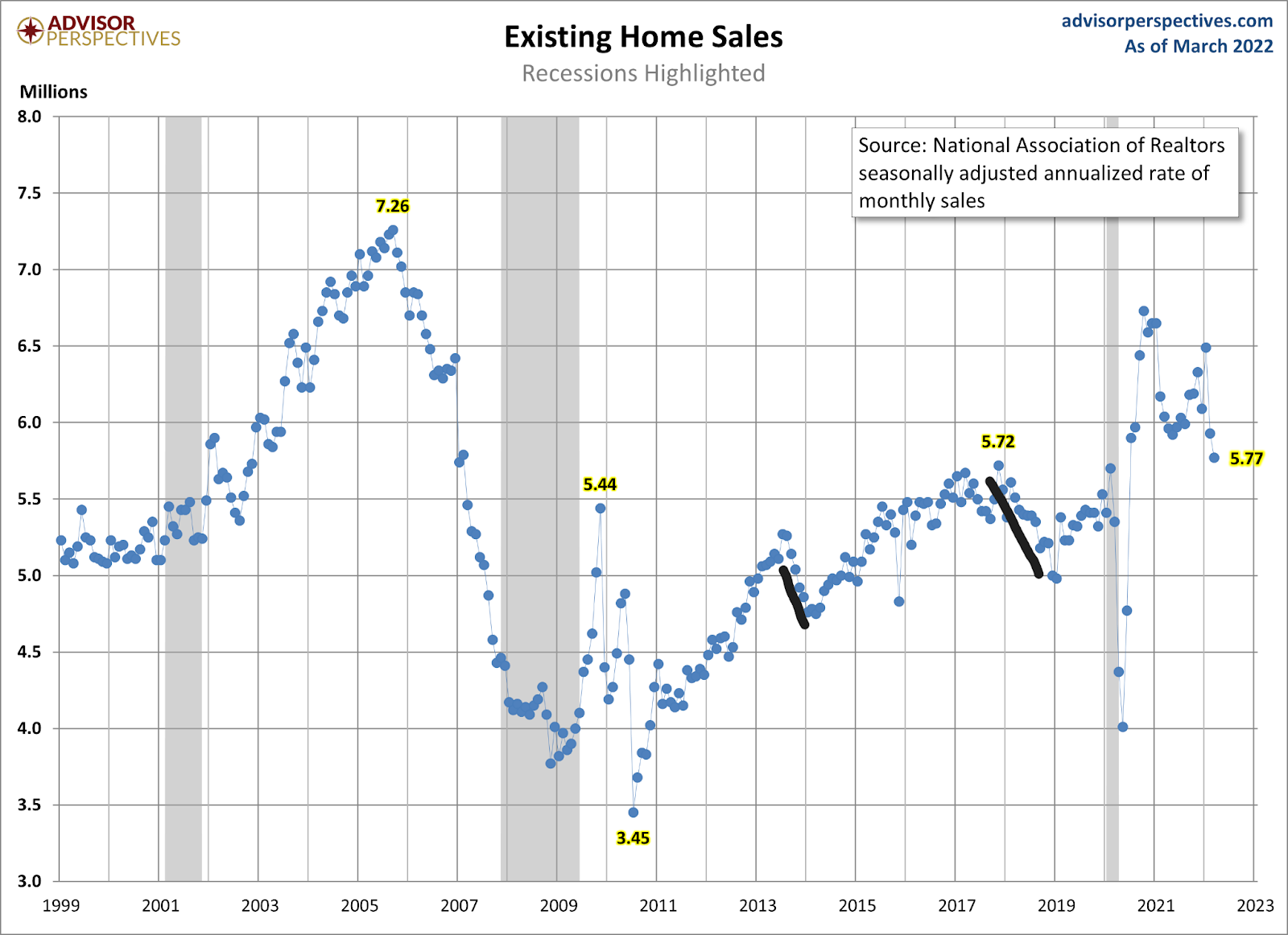

Housing demand has been stable for the past few years; we have never had a credit boom in demand since 2002-2005. So, we never had a credit bust as we saw from 2005 to 2008. However, post-2010, we have had times when housing demand has gotten softer with higher mortgage rates.

In 2013-2014, rates rose, and you see the lower trend in sales back then. Demographics and employment levels were much different at that time, so it isn’t the best comp to use compared to 2020-2024, which has the most significant housing demographic (ages 28-34) running at 32.5 million.

In 2018 when mortgage rates rose, we saw existing home sales trend lower from 5.72 million to 4.98 million in January 2019. Even though total existing-home sales didn’t do much in 2018 and 2019, we see how higher rates impacted the demand curve. The housing data we got yesterday with housing starts are backward-looking. The same should be thought about today and going out in the future.

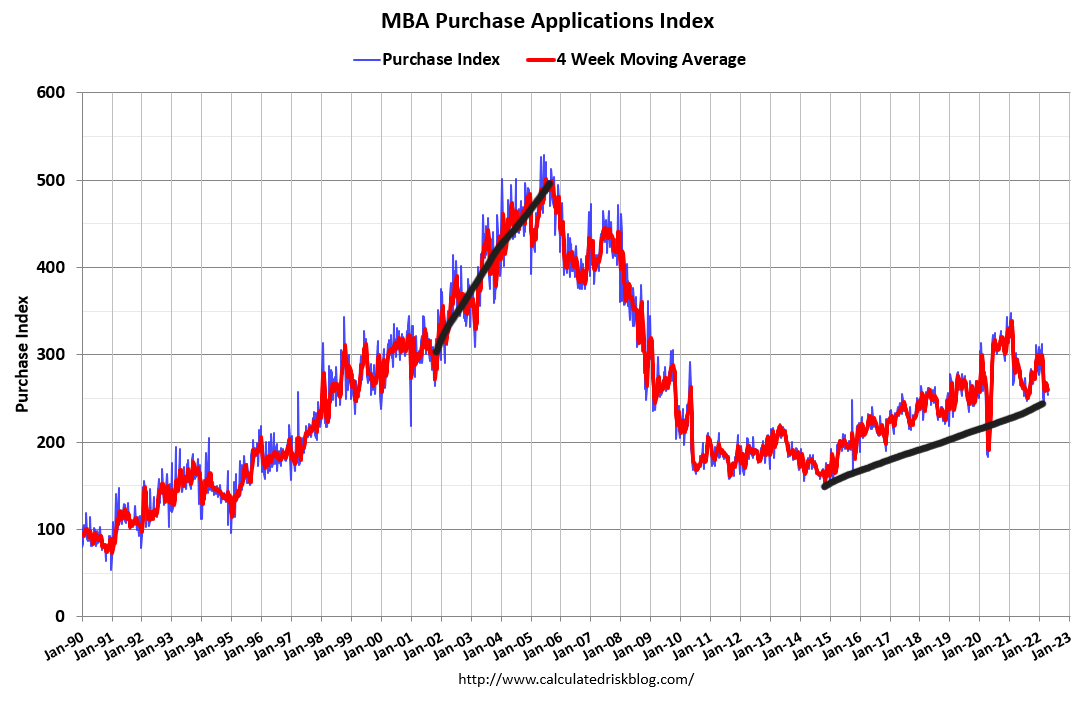

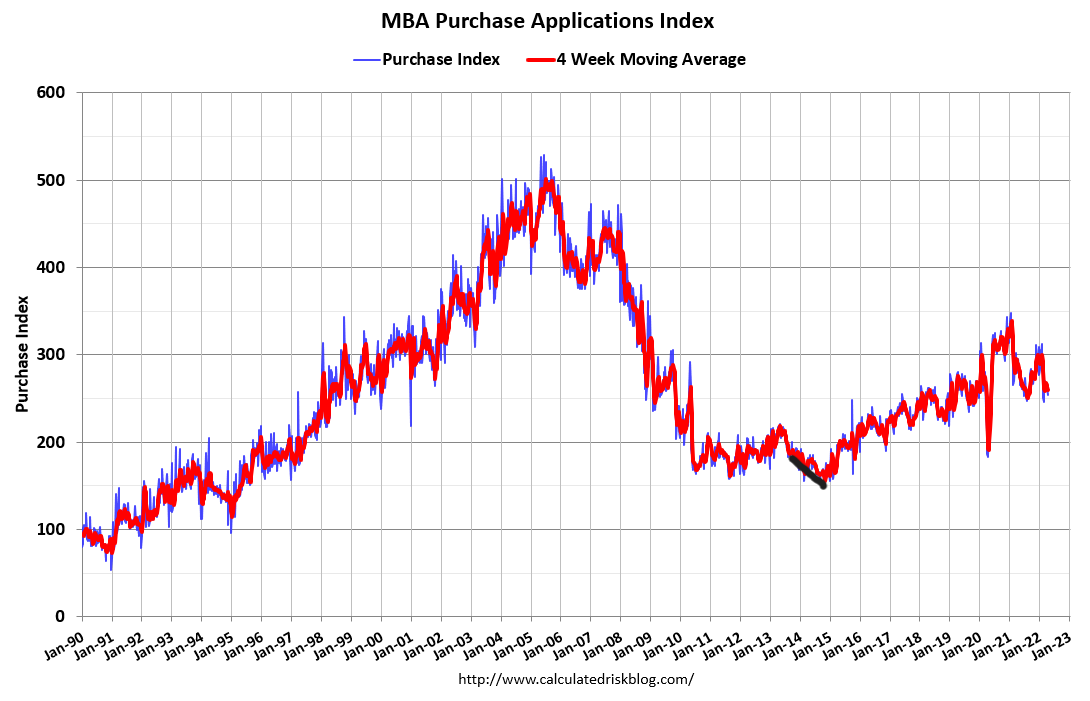

How does application data look? Due to COVID-19, I needed to make severe adjustments because the year-over-year data has been out of whack. This data line has been negative since June of 2021. With proper adjustments, you can tell what is going on.

2022 is looking to be the first actual negative year-over-year purchase application year since 2014. However, the decline is mild so far.

—Week to week: -3%

—Year over year: -14%

—4 week moving average YoY: -9.75%

The week-to-week action has produced two mild positive and two mild negative prints for four weeks. I believe the COVID-19 comps ran out by mid-February this year. So the year-over-year data is good to go. We are between what we saw in 2018 — with a mild response to higher rates — and 2014, where the reaction was much more severe. When it moves, this data line moves up and down 20%-30%. So the four-week moving average, while a noticeable weakness, isn’t anything too big yet.

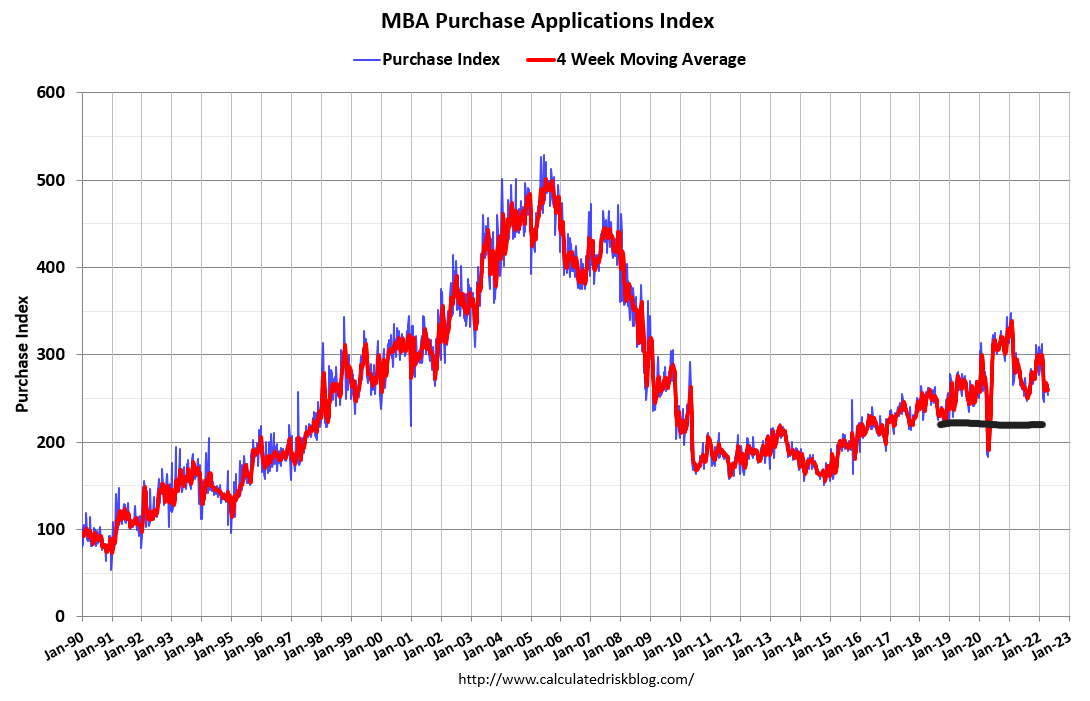

As you can see, the 2018 purchase application data didn’t show much of a reaction; it only had three very mild negative year-over-year prints and stayed true to the seasonal volumes declines we typically see after May.

When rates rose in the middle of 2013, we saw a clear downtrend in purchase application data, and in 2014 we saw a 20% year-over-year decline trend.

2014 was the last year total inventory grew. Sales went down that year, and the growth rate in pricing cooled off. Let’s hope for a similar response in 2022.

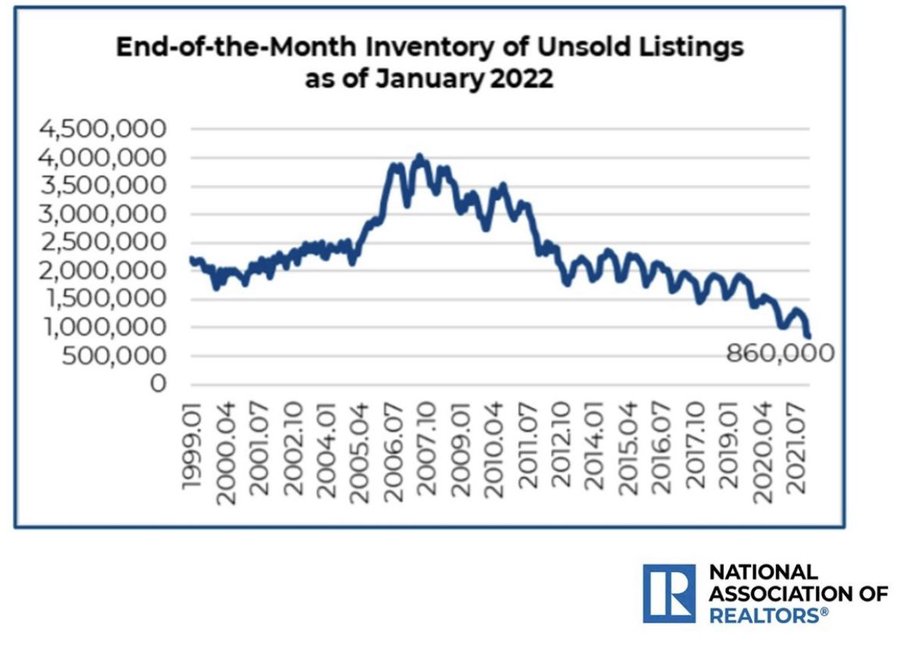

NAR: Total housing inventory at the end of March totaled 950,000 units, up 11.8% from February and 9.5% from one year ago (1.05 million). Unsold inventory sits at a 2.0-month supply at the present sales pace, up from 1.7 months in February and down from 2.1 months in March 2021.

Inventory levels are always seasonal; rising in the spring and summer and fading in the fall and winter. The goal is to get higher inventory data on a year-over-year basis in 2022, and higher rates should do it. Even if we get some positive year-over-year prints, the housing market is still working from all-time lows. However, we have to start somewhere.

My goal has always been the same; we want inventory to get back into a range of 1.52 – 1.93 million. We have a lot of work to do to get back to those levels.

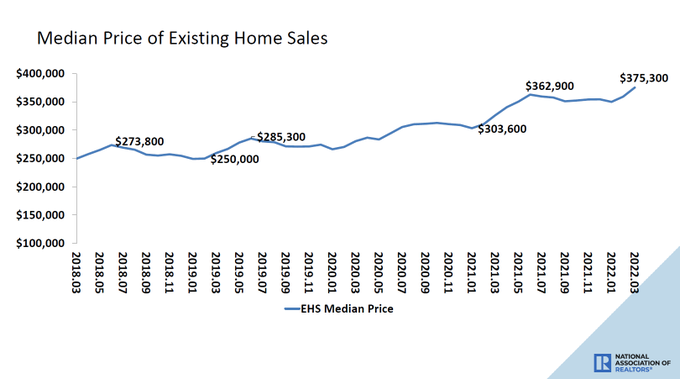

This year, I am “team higher mortgage rates” because the writing was on the wall for another year of unhealthy home prices. We are showing negative year-over-year data in inventory even this week. Since we blew past my 23% home-price growth model for five years in just two years, I need to adjust how I looked at the housing market once rates rose.

For example, if home prices grew 3% a year in 2020, 2021, and 2022, mortgage rates rising wouldn’t be a big deal. However, in 2020 alone we had 10% home-price growth. I create models to keep us in line with the data and not run into hypothetical situations.

As long as home prices grew at 23% cumulative for five years of total home sales, both new and existing homes should be 6.2 million or higher. However, since we broke that in two years and are still showing 15% home-price growth in 2022, we risk demand being hit harder than usual when rates rise. Well, this is what is happening in 2022.

NAR: The median existing-home price for all housing types in March was $375,300, up 15.0% from March 2021 ($326,300), as prices rose in each region. This marks 121 consecutive months of year-over-year increases, the longest-running streak.

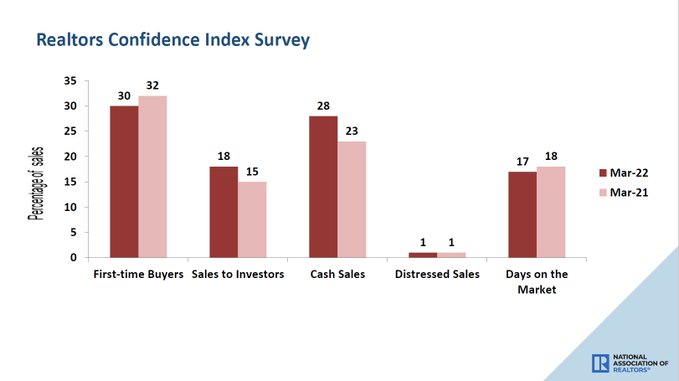

A big theme of my work regarding higher rates is that we need more days on the market. Higher rates didn’t create more inventory in 2018, but they did generate more days on the market and gave people more choices and time to buy a home. I can’t express enough how savagely unhealthy housing is when days on the market are still running at teenager levels.

NAR: First-time buyers were responsible for 30% of sales in March; Individual investors purchased 18% of homes; All-cash sales accounted for 28% of transactions; Distressed sales represented less than 1% of sales; Properties typically remained on the market for 17 days.

All in all, we still have a savagely unhealthy housing market. However, there is some hope of higher rates creating balance. Wednesday’s existing home sales report and Tuesday’s housing starts data are backward-looking and don’t account for a 5% plus mortgage world. Continuing a years-long trend, the inventory crisis got worse in America in 2022, and we are paying for it in much higher home price costs for homebuyers that don’t have a significant down payment; their cost of shelter just got a lot more expensive than last year.

On the other hand, homeowners are chilling like villains in their lovely homes with their fixed payment loans and enjoying life. It should be an exciting year ahead of us.