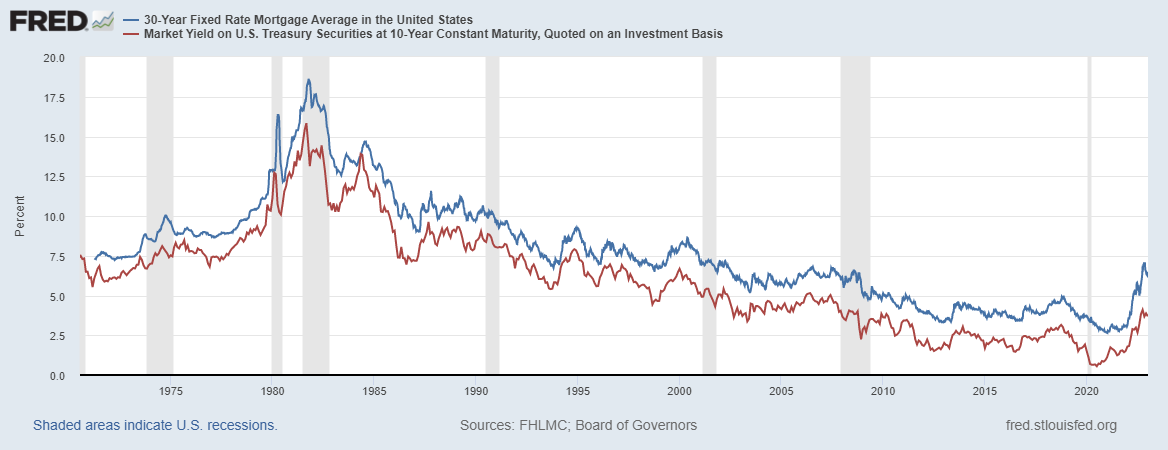

Can we have a soft landing in the economy? Friday’s job report shows there is a clear pathway to get there. Mortgage rates fell aggressively down to 6.20%, putting us at more than 1% below the highs of 2022.

The bond market saw that wage growth was cooling down, leaving the Federal Reserve with few reasons to keep the rate hike story going much longer.

We ended 2022 on a solid note as 4.5 million jobs were created last year — and we still have more than 10 million job openings and historically low jobless claims. And now, the growth rate of inflation is falling.

Bond yields fell after the report since wage inflation is cooling down, a key for the Federal Reserve‘s strategy. The Fed will not tolerate a tight labor market, or Americans on the lower end of the wage pool making more money. They believe this is a bad thing and will create too much entrenched inflation, so the fact that wage growth is cooling off is a positive sign.

If the inflation growth rate and wage growth are slowing down, the Federal Reserve doesn’t need another rate hike. In fact, the Federal Reserve needs its own reset. That is going to be a big theme of mine for 2023 if this trend continues.

However, the bigger story here is there is a pathway for a soft landing for America, and the Fed should be ashamed of itself for believing that a job loss recession is the best way to kill inflation. The inflation growth rate is already falling and the labor market is still solid.

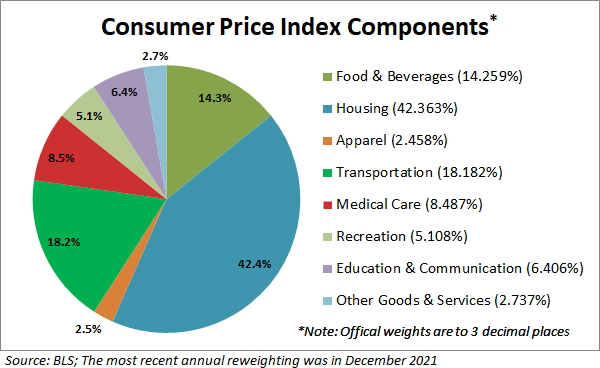

If shelter inflation had a more real-time tracking system, the headline inflation data would already be lower. Thankfully, the Fed has created its own index to account for much of the lagging inflation in the data line. This is a big deal since nearly 43% of CPI inflation is shelter inflation.

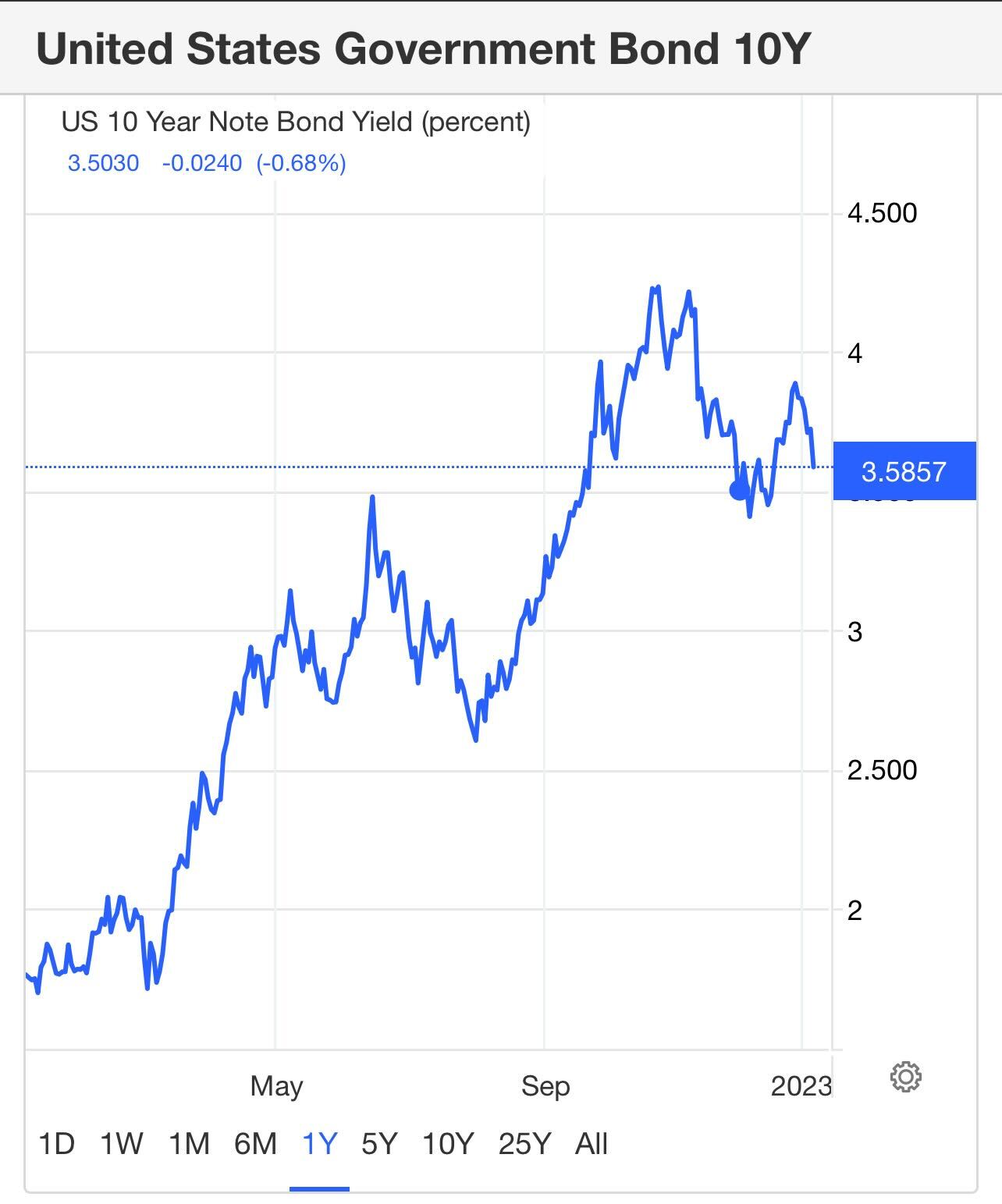

This is why Friday’s data is exciting to see and why the bond market sent mortgage rates to 6.20% and yes — we are back on 5-handle mortgage rate watch. It wasn’t that long ago (in October) that people were talking about 8%-10% mortgage rates and a big recession for the United States of America.

Job report

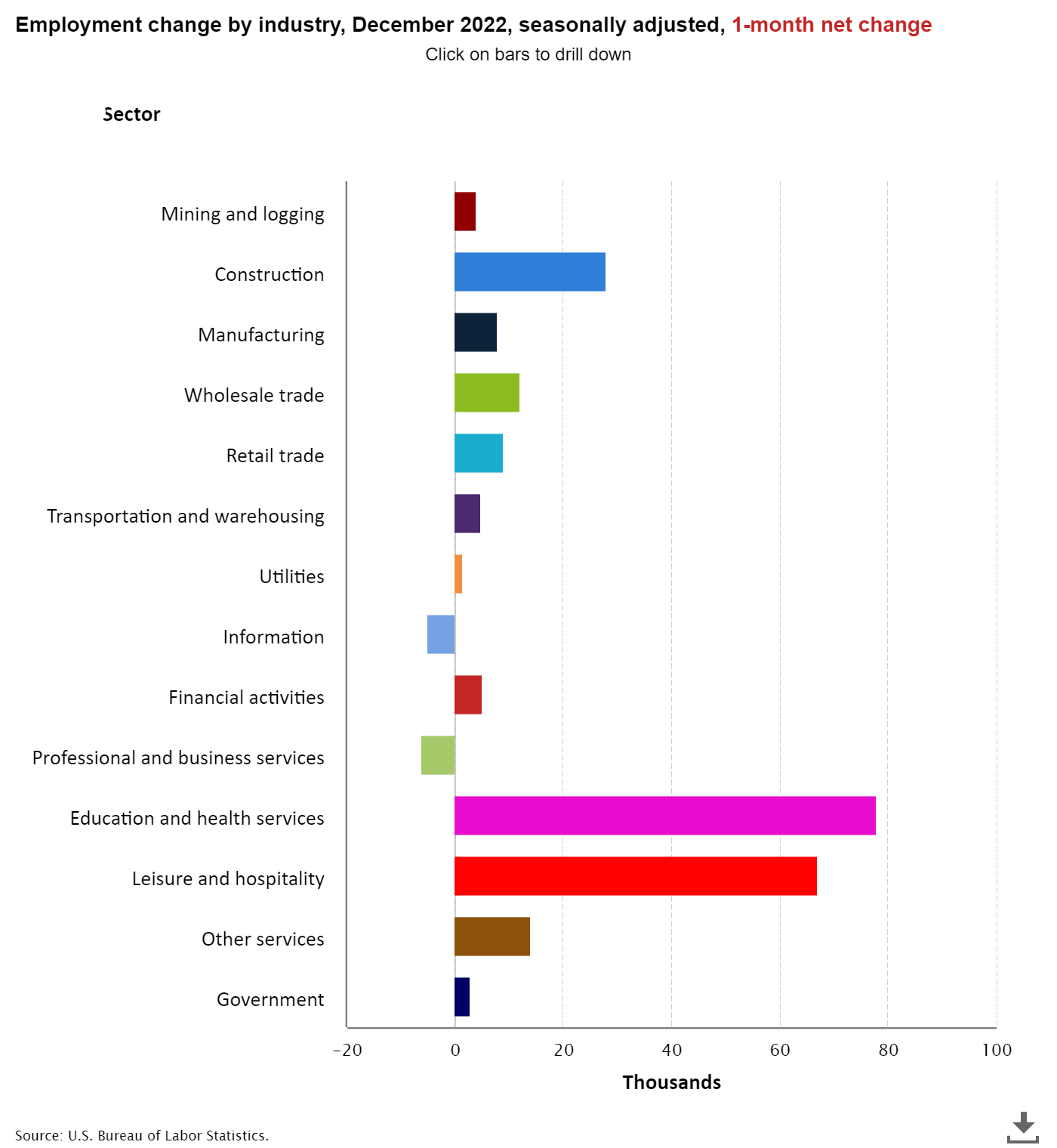

From BLS: Total nonfarm payroll employment increased by 223,000 in December, and the unemployment rate edged down to 3.5 percent, the U.S. Bureau of Labor Statistics reported today. Notable job gains occurred in leisure and hospitality, health care, construction, and social assistance

This chart shows a breakdown of the jobs created and lost. The two sectors of the economy that are getting hit are the tech sector and housing, but this is a good report for construction. The backlog of homes needing to be built has kept construction labor up until those homes can be finished. I can’t express what a blessing this is because the best way to fight inflation is always by adding more supply.

Here’s a breakdown of the unemployment rate tied to the education level for those 25 years and older.

- Less than a high school diploma: 5.0% (previously 4.4%)

- High school graduate and no college: 3.6%

- Some college or associate degree: 2.9%

- Bachelor’s degree or higher: 1.9%

As we can see above, the labor pool for college educated workers is lacking; this is a big reason the unemployment rate is below 2%. The work visa supply of labor just isn’t enough to supply this pool.

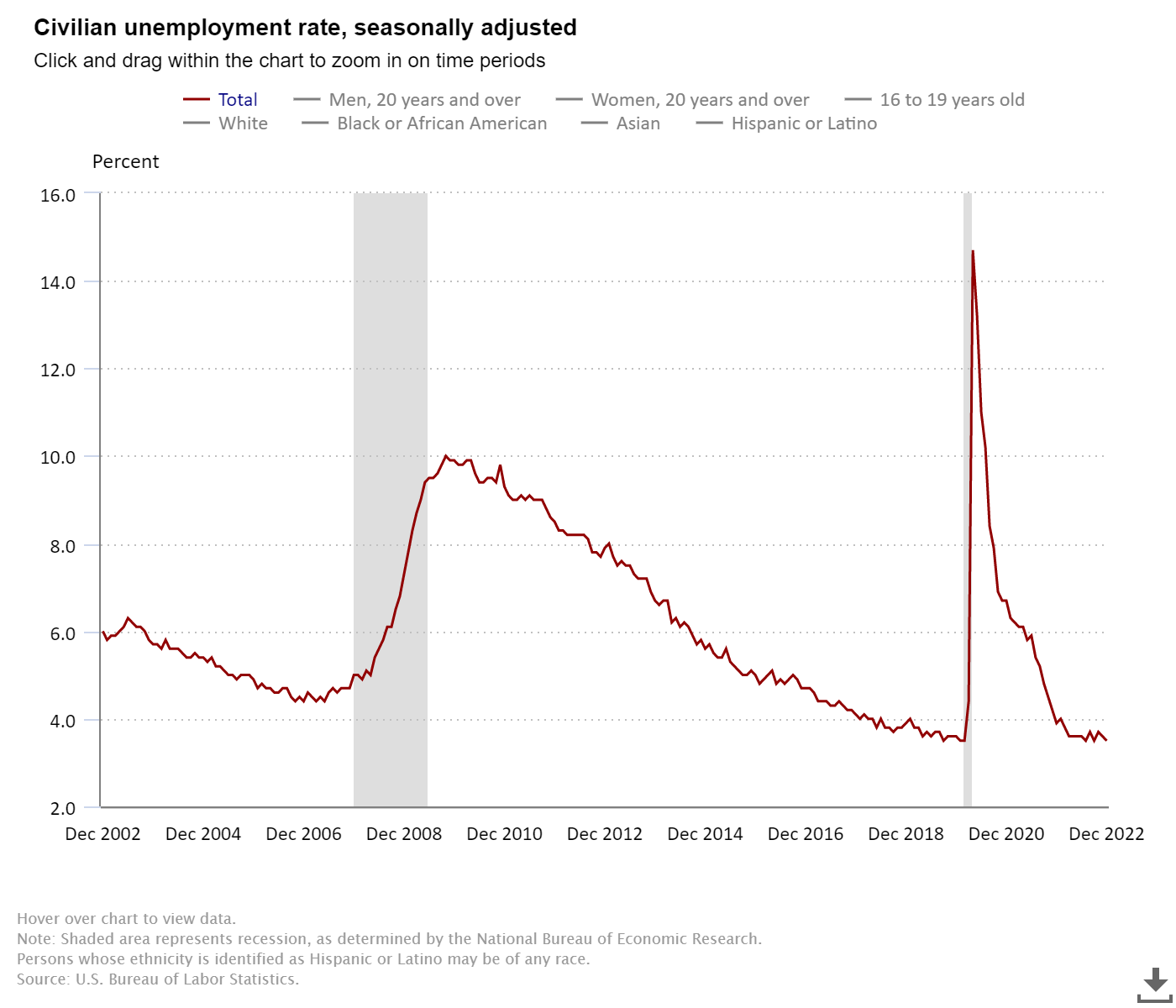

The unemployment rate has found a bottom of around 3.5%, and I want to remind people that the growth rate of inflation is falling even with the unemployment rate still at 3.5%.

You don’t need to create a job-loss recession to bring inflation down. I understand why some people believe this. However, before COVID-19 happened, we didn’t have breakaway inflation in the 21st century, either here or in other mature economies where population growth is slowing.

Inflation and bond yields

The real story of today is that bond yields are again getting ahead of the Federal Reserve. No matter how many Fed people talk about needing financial conditions tighter for months now, the bond market is saying otherwise.

The Fed’s premise that a job-loss recession is needed to bring down inflation should be pushed back by everyone. If the growth rate of inflation was still running out of control with wage growth exploding higher, then we would be having a different conversation. However, I truly believe that the bond market was always telling us that this wasn’t the 1970s.

The 1970s saw higher inflation and higher bond yields, and the inflation back then was more entrenched. The 10-year yield, as I speak, is at 3.58% Friday, even after all we have gone through. The growth rate of core PCE inflation, which the Fed wants back down to 2%, should have a three-handle this year.

I made a case for lower mortgage rates on Oct. 27, 2022, and then wrote about how we could still avoid a job-loss recession in November. In both articles, one factor was key: the growth rate of inflation falling. This is happening now, even with a labor market that still has over 10 million job openings.

The second key is falling bond yields; I am not even discussing cutting rates yet. First things first, the growth rate of inflation falls, and the bond market yields fall with it.

For now, both things are falling from their recent peaks. The Fed can’t control Russia, OPEC, or the bird flu, and the U.S. dollar isn’t collapsing. However, any rate hike at this point is on them. They have expressed their beliefs about moving the Fed funds rate to where core PCE is, and if the trend of inflation continues as it is, the 10-year yield is more correct than the Fed today.

To sum it up, we had another solid jobs report Friday: the unemployment rate is low, job openings are high and jobless claims are historically low. I truly believe that at this economic expansion stage, the Fed doesn’t need to continue its path of sounding like a hawk because we already see evidence of inflation falling.

Let’s not forget the biggest driver of inflation for the CPI report is shelter inflation, and that is already cooling off dramatically.

The Fed should think about becoming a dual-mandate organization again at some point since they front-loaded so many rate hikes early on. They should let that stick and watch the data get better. I don’t know if they’re this clever or know that they can take the victory lap. However, what we have seen in the last few months has been very encouraging for those who don’t want to see a job loss recession.