Both monthly and annual adjustable Home Equity Conversion Mortgages (HECMs) reported steady draw rates in January consistent with previous months, according to the latest Reverse Mortgage Draw Index issued by New View Advisors this week.

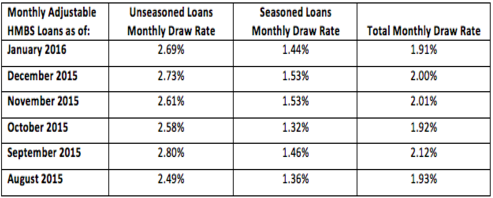

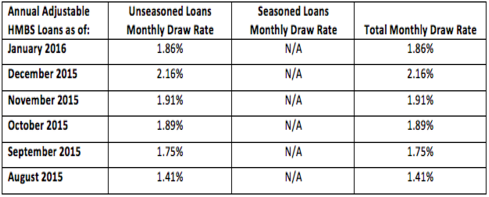

The Index, which New View Advisors compiled using publicly available Ginnie Mae data as well as private data sources, shows a Monthly Adjustable HECM draw rate of 1.91% and Annual Adjustable draw rates of 1.86% in January.

Compared to the previous month, the total monthly draw rate on Monthly Adjustable HMBS loans as of January 2015 was slightly lower at 1.91% versus 2% in December 2015.

Meanwhile, for Annual Adjustable HMBS loans, the total draw rate was considerably lower than the previous month’s numbers, with 1.86% in January compared to a draw rate of 2.16% in December.

Annual adjustable loans are a relatively new product, notes New View Advisors, with only a handful of these loans seasoned more than two years.

“However, each month a larger and larger number of annually adjustable loans reach the expiration of the restricted draw period,” writes New View Advisors in its latest market commentary. “As a result, the Annual Adjustable loan draw rates are converging with the Monthly Adjustable Rates.”

In the tables above, the index value is expressed as a monthly draw rate, equal to the amount of Line of Credit draws taken in any given month, divided by the Total Line of Credit Amount available at the beginning of that month.

The index applies to loans with a Line of Credit feature and does not include fixed monthly Term or Tenure payments. New View Advisors defines unseasoned loans as loans originated no more than two years ago, whereas seasoned loans are loans originated more than two years ago.

Each month, Ginnie Mae releases pool level and loan level data on their HECM mortgage-backed securities (HMBS), and the loans underlying those securities.

“This comprehensive Ginnie Mae data repository enables a greater understanding of the underlying loan characteristics and behavior that drive performance within the reverse mortgage industry,” writes New View Advisors. “Prepayment, Default, and Draw behavior are the Big Three of Reverse Mortgage performance indicators.”

While draw behavior depends on several factors, none is more important than loan age for investors, lenders and HMBS issuers, says New View Advisors. The draw rate affects prepayment rates, HMBS Tail issuance, as well as the frequency and severity of defaults.

“For all market participants, an accurate measure of draw rates is essential for managing cash flow, forecasting future capital needs and profitability, and measuring enterprise risk,” writes New View Advisors.

According to New View, draw rates tend to be higher in the early years of a loan, then decline to a stable plateau as the loan matures.

As a result of upfront draw limitations implemented by the Federal Housing Administration in Fiscal Year 2014, the draw amount for many HECM loans is restricted in the first year. Because of this, New View notes the overall draw rate jumps materially in month 13.

Read the New View Advisors commentary.

Written by Jason Oliva