Today’s inflation data has shown that the peak growth rate of inflation is behind us. This should also mean mortgage rates have hit their highs. The key phrase I have stressed since I wrote about the case for mortgage rates to go lower on Oct. 27 is thinking 12 months out. The trend is your friend, and the month-to-month data has cooled off noticeably.

That cooling happened even with the biggest inflation component — shelter inflation — still rising in the lagging CPI data. This means shelter inflation isn’t being properly accounted for versus the real-time data.

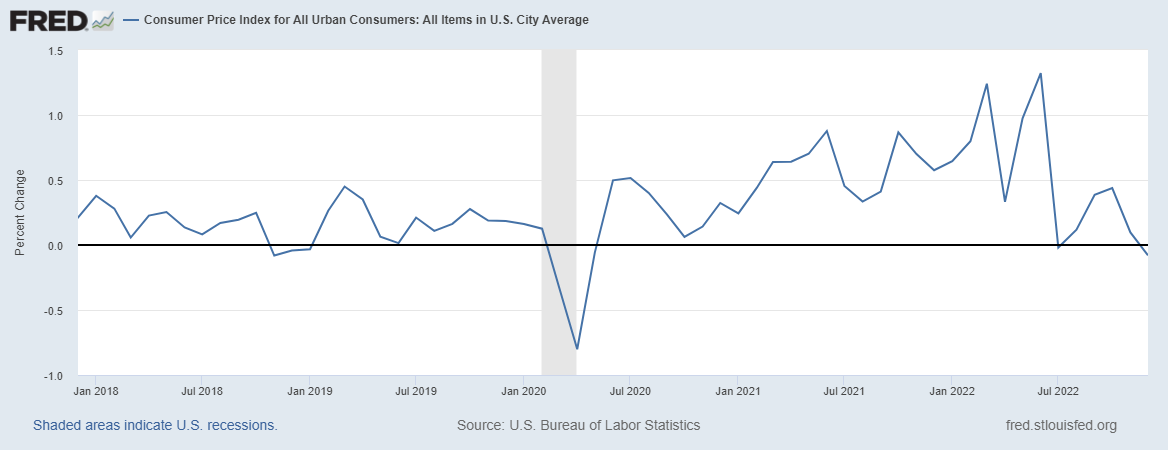

The Consumer Price Index month-to-month readings show that inflation has peaked, as seen below.

If it weren’t for the lagging CPI shelter index, the biggest component, the headline core print, would be lower today on a year-over-year basis. It’s a positive thing that most people have gotten the memo on this reality about shelter inflation because it shows how the headline year-over-year prints are lower as we speak.

While still hot, the year-over-year inflation growth rate is falling, see below.

All this is happening with the labor market still very tight, which means the Fed doesn’t need to create a job-loss recession to bring inflation down. The best way to fight inflation is to add more supply, demand destruction is not the most effective way, and it will impact future production.

The jobless claims data on Thursday, as you can see below, was still solid and running at 205,000 for the headline, with a four-week moving average of 212,500.

For those who were saying we needed an unemployment rate above 6% to bring down inflation, you must feel sick to your stomach as that advice would have meant millions of Americans would have lost their job for no reason.

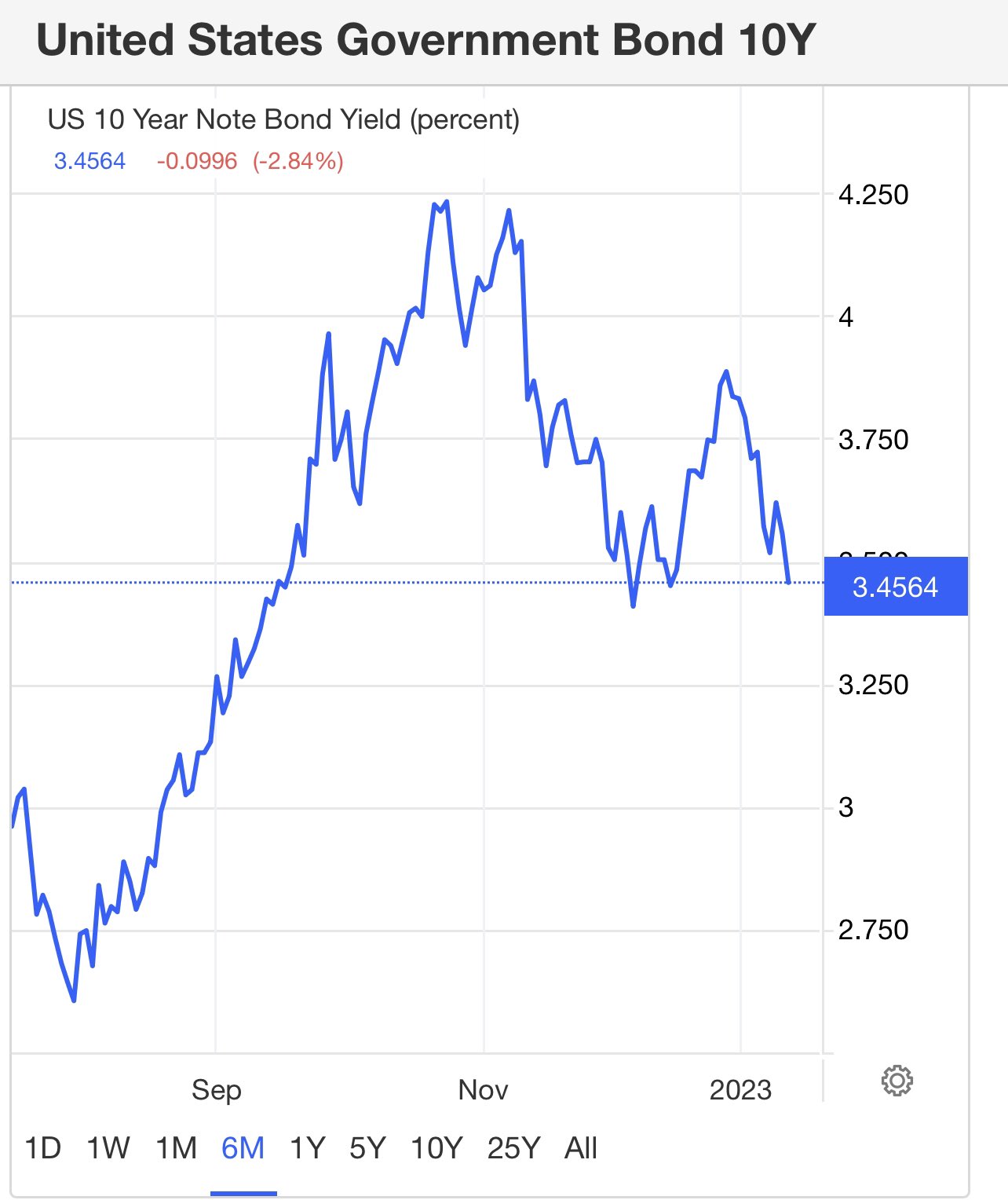

How did the bond market react to this inflation data? It was a mild day compared to what we saw back in November of 2022. However, as I am writing this, the 10-year yield is at 3.45%, which is the third time we are trying to lower this area.

This does mean mortgage rates should be getting better today. We are getting closer to a five-handle in mortgage rates and farther away from the 8%-10% mortgage rates people were talking about late last year when rates peaked at 7.37%.

Digging into the inflation data

From BLS:

The Consumer Price Index for All Urban Consumers (CPI-U) declined 0.1 percent in December on a seasonally adjusted basis, after increasing 0.1 percent in November, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 6.5 percent before seasonal adjustment. The index for gasoline was by far the largest contributor to the monthly all items decrease, more than offsetting increases in shelter indexes. The food index increased 0.3 percent over the month with the food at home index rising 0.2 percent. The energy index decreased 4.5 percent over the month as the gasoline index declined; other major energy component indexes increased over the month.

Breaking down some of the internals is key to understanding the CPI data. Of course, the biggest component of inflation is housing. I stressed in late 2020 that shelter inflation was going to take off, but the opposite is the reality now. However, the CPI data lags badly here.

Thankfully, the Federal Reserve understood this and created its own index in December to account for the lag. Back in September, on CPI inflation day, I talked about how this would be a positive story in 2023. I said by January or February, it would be evident that the growth rate of shelter inflation was falling, and people have gotten the memo. I could not have asked for a better outcome than where we are today.

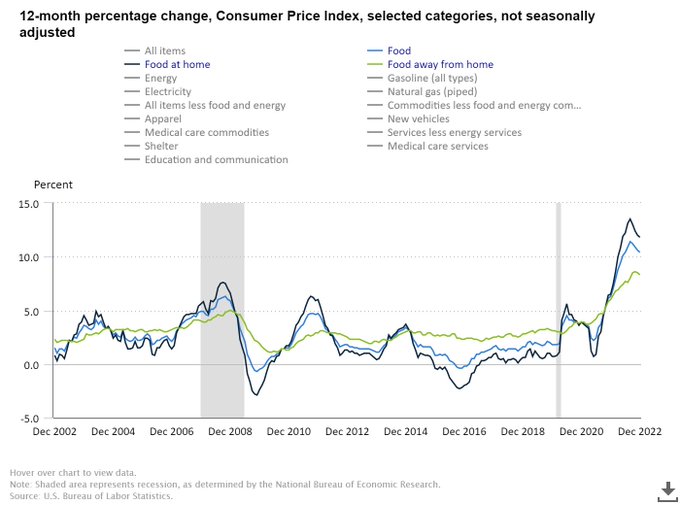

Shelter inflation will always lag; let’s wait until October of 2023 to see when this data line will finally show some peaking and follow the more current data. When that starts to happen, core CPI will fall more noticeably. As we can see in the graph below, the growth rate is still hot here with shelter data.

The growth rate of food inflation looks like it’s peaking; we all know the drama the bird flu has done to egg prices, and there is nothing the Fed can do about that. Food inflation is part of headline inflation, which tends to have wild swings up and down, and this is why it’s not something the Fed looks at.

We all know the massive car inflation story post COVID-19, a lack of production and chips have boosted inflation here badly. However, this is rolling over too.

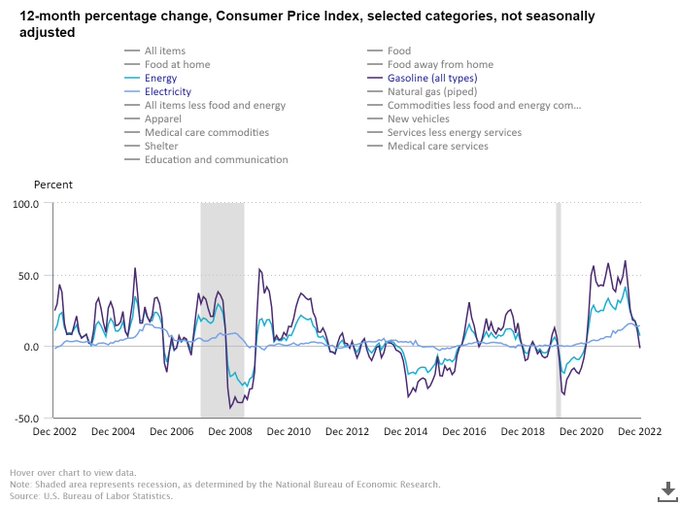

The energy fall is well known as oil prices have fallen noticeably since the spike from the Russian invasion of Ukraine. Oil is a weapon of war in this modern age and we have fought back on this front with our reserves. But what happens when the reserves run low, and China returns from its COVID-19 shutdowns and starts driving cars again? Something to think about in the future.

The CPI report came in line with what most people were expecting, so there is no real shocker news here. However, the bigger story is the trend, and if you’re hoping for the Fed to keep over-hiking and put the U.S. in a massive recession, today wasn’t a good day for you.

I saw one discussion on Twitter where an analyst was claiming the Fed needs to take the Fed’s fund rate to 7% or 8%. This was the hope for bearish Americans — that maybe the Fed still hadn’t got the memo that the fear of 1970s inflation just isn’t going to stick in this modern-day economy without supply shocks at this stage.

The bond market, as always, had gotten ahead of the Federal Reserve, and maybe the Fed will eventually get it. However, for now, rates are going lower, and the fear of 8%-10% mortgage rates for the spring of 2023 is slowly dying a good death, like the fear of 1970s inflation.

If you want a soft landing, this is the inflation data you want to see, something I talked about last year, even on recession watch. It’s a good day for the United States of America and the housing market.