The Silver Tsunami home price crash thesis was introduced in 2008 when the first baby boomers started turning 62 years old.

Now, more than a decade later, those first baby boomers are turning 74, and this thesis is reemerging as news again.

So what is the Silver Tsunami home price crash thesis?

In short, it says that older Americans are poised to sell their homes en masse, leading to a massive influx of inventory. At the same time, since Millennials are burdened with a large amount of student loan debt and have no savings, there won’t be any demand to absorb the excess inventory. As a result, housing prices will crash, leading to a devaluation of the dollar and hyperinflation. The only safe bet in these circumstances, as the theory goes, is to invest in gold.

Columnist

A lot of financial marketing is based on the fear of home prices crashing, so I get why this could resonate with some people.

Putting the scare tactic aside, let’s unpack the assumptions of this thesis to see if it has any merit.

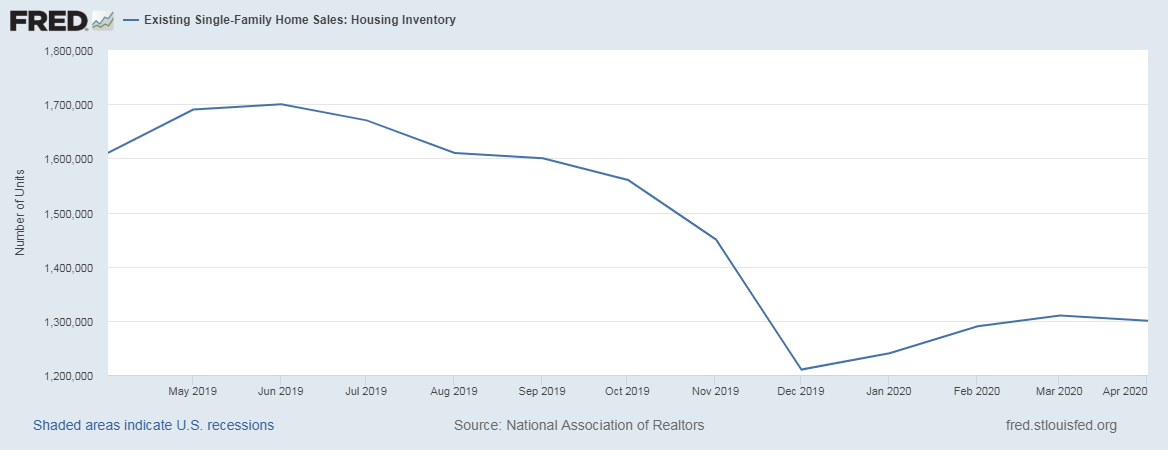

First, housing inventory currently sits near all-time lows, with the COVID-19 crisis having some part to do with this. Would-be sellers are holding back from listing homes and are delisting homes already listed. Inventory should somewhat increase when the economy opens up more, and homeowners become more comfortable with having strangers enter their houses for viewings. However, there is no evidence that there is a glut of homes waiting in the wings to be listed by baby boomers.

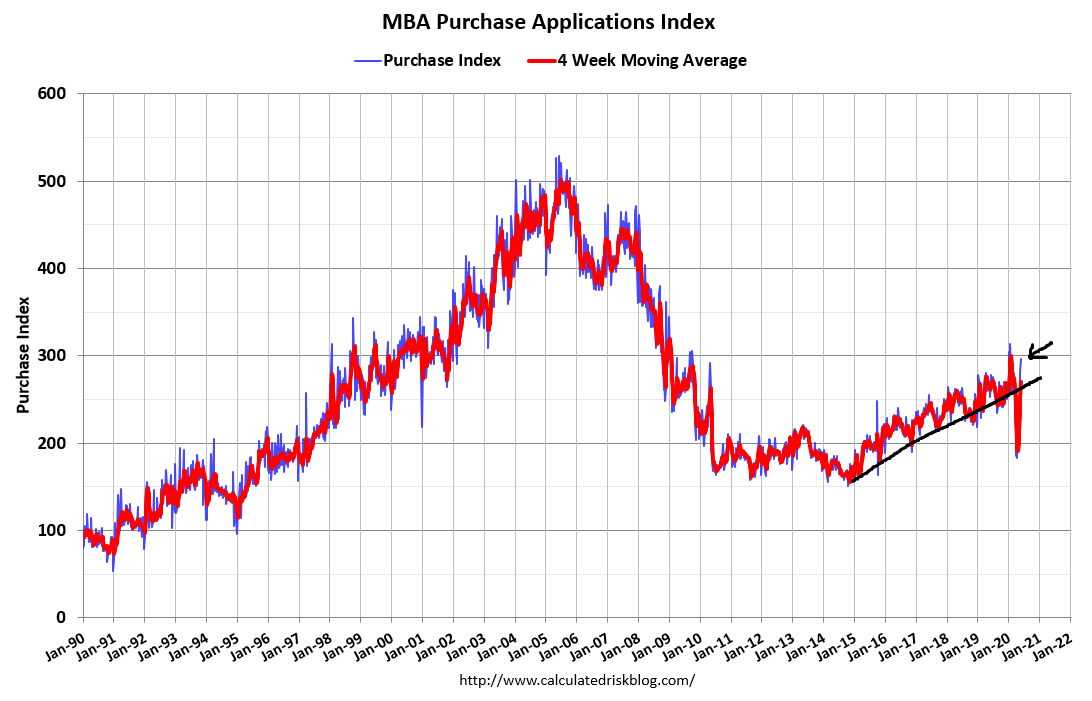

Secondly, when it comes to demand, the Mortgage Bankers Association’s latest data on purchase applications shows that despite a temporary pause due to the shutdown, demand is back on track to continue the uptrend that has been going on since 2014.

This means there’s no evidence for a potential massive rise in inventory or a waterfall drop in demand, so a Silver Tsunami home price crash in 2020 is unlikely. It’s time to move the home price crash thesis to 2021.

Next time the Silver Tsunami home price crash thesis comes up, ask these four questions to evaluate the theory.

1.What are builders doing? Home builders are in the business to make money. New homes have to sell at a specific price to make it financially worth it. Every decade that goes by adds to the existing-home inventory and increases the competition for new homes. If builders are still building, you can rest assured that there is not a brewing inventory glut. While housing tenure used to sit at an average of 5 years from 1985-2007, it is now more than 10 years, which is also keeping a lid on inventory.

2. How is demand? If the MBA’s purchase application data is negative year over year for 12 months straight, we could expect to see a noticeable increase in inventory. But until that happens, there is no need to buy into a speculative theory that is solely designed to sell gold to frightened consumers.

3. Where are mortgage rates? When mortgage rates reach 4.5% or higher, we can expect to see a hit on demand. Housing demand weakened twice in the previous expansion when the 10-year yield went above 2.62%. However, mortgage rates today are at all-time lows.

4. Who is trying to sell the idea of a housing crash? One of the doomsday crowd’s favorite marketing gimmicks is to foment fear of a housing crash. In truth, there is greater risk of a housing price increase due to a lack of inventory. This is the one aspect of housing I don’t like this year. Home prices are rising too fast, and we need them to cool down as soon as possible. Last year, prior to the crisis, I was thrilled to see real home prices go negative on a year-over-year basis. Steady home price growth is what we should be rooting for in order to maintain an affordable market.

This is housing, not the stock market. The main drivers for housing are demographics, mortgage rates and housing tenure. Homeowners need a reason to sell. They are not over-leveraged stock traders getting margin calls and needing to sell at any price.

Housing prices may collapse someday, but when this happens, we will see the data first. Until then, “party on Wayne.”