Since the onset of COVID-19, the Twittersphere has been ripe with rumor and speculation that the financial requirements to qualify for a mortgage have become increasingly more rigorous since the crisis and this would put a damper on the housing market.

Lead Analyst

It is true that the COVID-19 crisis did temporarily wreak havoc on the mortgage market. Case in point — the week of March 9 and the mortgage market meltdown. You may recall the precipitous drop in rates which resulted in a flood of refinance requests which amplified early pay off risk, mortgage margin calls, and the rapid rebounding of rates.

Needless to say, all that drama from COVID-19 created significant stress in the mortgage market. As a result, many non-QM lenders left the market and FHA homebuyers with low FICO scores saw credit get tighter. The U.S. jumbo market loans saw some difficulty as well. Some lenders even stopped offering home equity lines.

While that all sounds pretty drastic and scary, at the end of the day this prevented only about 4.5%-6.2% of all purchase loans from closing of those that would have closed prior to the meltdown. This means that approximately over 93% of the purchase loans that could have closed during the period of the record-breaking expansion still closed during the early part of the COVID crisis. This is because after 2010, the loan profiles of mortgage seekers before and during the COVID crisis have been, in a word, excellent– the best loan profiles that I have ever seen in my 24 years of lending experience.

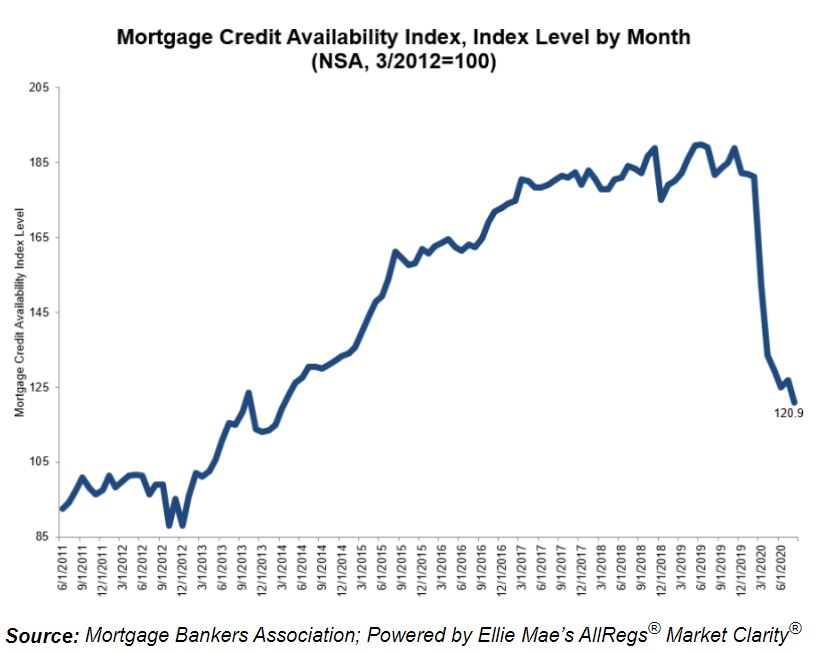

One may ask then, why, according to the recent MBA report, does look like it’s harder to get a loan?

I agree that to the novice or casual observer of housing charts, this looks to be the case according to this graph. But, here is why we see a dramatic drop in the mortgage credit availability index that corresponds to the beginning of the COVID crisis. From 2012 to 2020, marginal guideline changes were made that eased credit standards. Although these changes were marginal and did not significantly affect the basic purchase and refinance markets, they did result in a significant climb in the mortgage credit availability index.

Then, the mortgage market meltdown tightened credit in the specific sectors I previously mentioned and that corresponds to the drop we see in the index. However, the bread-and-butter loans that make up the majority of the purchase market have essentially the same standards as they did during the expansion.

And credit was never tight in American from 2008-2020, but the “tight lending” narrative was a popular dirge during those years. In my opinion, the theory that residential lending in America was tight from 2008-2019 is one of the worst economic theories of the 21st century.

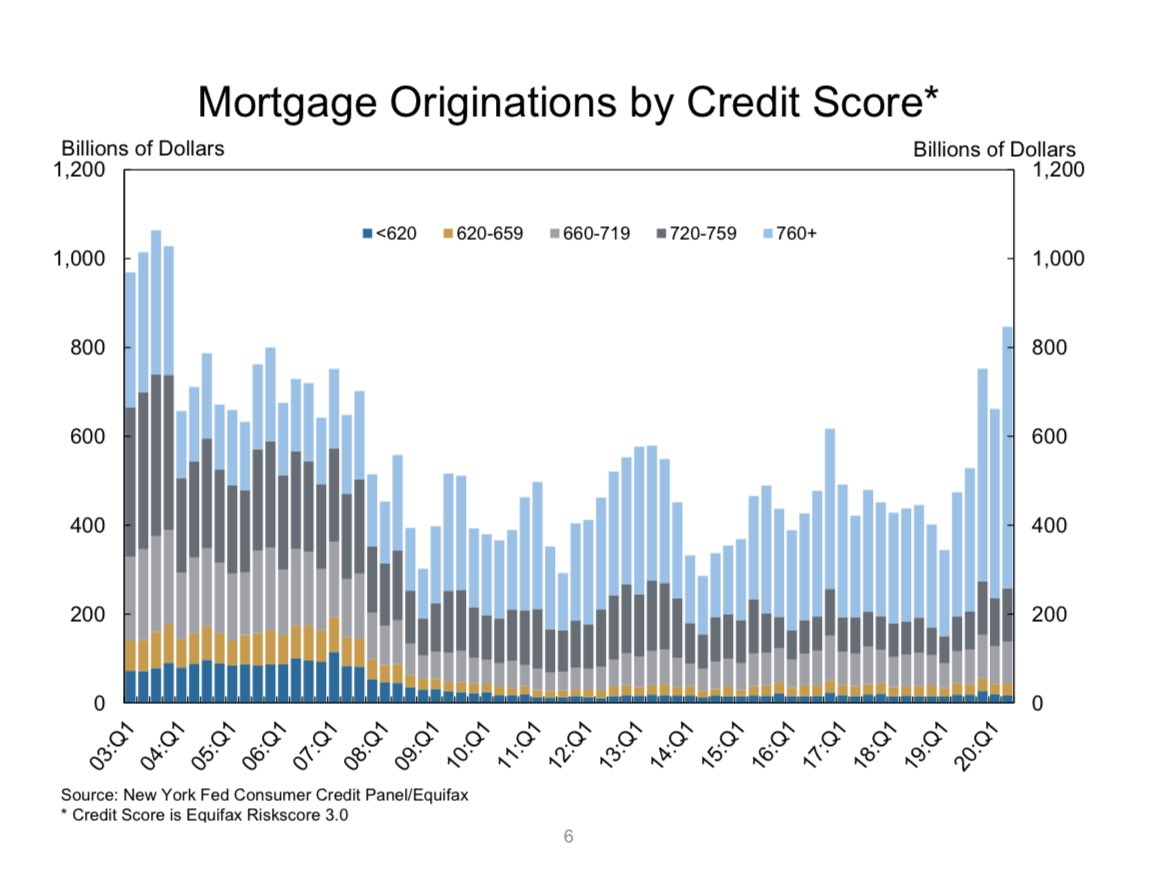

What happens when you lend to the capacity to own the debt is that Americans who are struggling with cash flow, who typically have low FICO scores, don’t buy homes. Nothing is abnormal about this and we should be proud as a country that our home-loan profiles look this good. As you can see below, we have taken down the sub-620 FICO score homebuyer since 2010, while the 700 and up FICO score homeowner makes up a higher portion of the market. This means that Americans go into the home-buying process with better cash flows.

Credit wasn’t tight then and it is not tight now. We currently have precycle highs in lending when you combine purchases and refinances. Would this happen — in the middle of the COVID crisis — if credit was too tight?

In 2020 we have seen home sales heading higher after the COVID-19 dip, which means nominal home prices will have another year of being positive. Higher home prices mean that homeowners have more nested equity added on their financial balance sheets. This is especially important for FHA mortgage households because those borrowers start with little equity and thus are the greatest risk for foreclosure during a personal or national economic downturn.

The homebuyer profile that would be at the highest risk for foreclosure is always going to be recent FHA homebuyers who purchased a home before home prices fall during a job loss recession — especially those with lower FICO scores.

Recent FHA homebuyers aside, most American mortgage households have good equity positions and had good cash flow when the loans originated. Not to mention another wave of refinancing in 2020, which means lower fixed debt cost vs rising wages plus more equity. Just whistle folks, it doesn’t get any sexier than that.

Thankfully, too, the GSEs have remained in government conservatorship. Having these giants protected from the vagaries of the stock market with government backing when this crisis hit has been a huge benefit to the American people. The GSEs’ responsible actions during this crisis will go down in history as a huge benefit to the American people and thus never should be forgotten. Remember this time when you believe that these giants should be publicly traded companies with no government backing and their fiduciary duties are to shareholders first.

A lot of bearish housing folks — from the anti-central bank boyband troll camps to the housing bubble boys turned forbearance crash bros — have been hoping that the COVID-19 crisis would crash home prices. One of the favorite lines among this crowd is that credit is getting tight, and this will destroy the housing market. But, it is just not true folks. To be fair, almost none of these people have a residential financial background and this lack of experience shows itself in 2020. Stay safe, my friends.