The financial and housing markets are still trying to sort out the banking crisis and whether we have seen the last Fed rate hike in this cycle. These events led to lower mortgage rates and increased purchase application data last week, but decreased housing inventory.

Here’s a quick rundown of the last week:

- The 10-year yield had a Lord of Rings battle at a critical technical level, pushing mortgage rates lower at the end of the week with no real break in the bond market.

- Active inventory fell 1,109, and new listing data made a lovely comeback week to week but was still noticeably down year over year.

- Purchase applications rose for the third straight week as rates have fallen, taking back the three weeks of negative data we saw when rates rose from 5.99% to 7.10%.

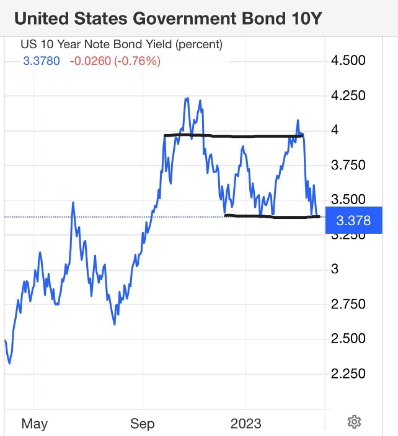

The 10-year yield and mortgage rates

Over the last week, I’ve watched the bond market attempt to break lower through a critical level that I have dubbed Gandalf’s line in the sand where the 10-year yield shall not pass. To Gandalf’s credit, he has been able to hold off Balrog for another week. As you can see in the chart below, the bottom black line tied to the 3.37% rate has been hard to break.

On these crazy days in the financial markets, I stress to people, it’s not how the trading day goes that matters; it’s the final closing number. Like a magnet, the 10-year yield has tried to break below this crucial level many times over the last five months, only to shoot back up to close at a level that wouldn’t warrant a pass.

As you can see in the chart below, this played out again on Friday when bond yields fell hard during the early trading hours, only to close back at that line.

In any case, mortgage rates were 6.75% on March 21 and 6.38% on March 24; the recent highs were 7.10%. If the mortgage market wasn’t so stressed, mortgage rates should be at 5.99% today. In a regular market, they would be closer to 5.25%. The Federal Reserve has made the housing market into an orphan left in the rain with no home to go to because there isn’t much inventory out there, so the markets are simply too wild up and down.

In my 2023 forecast, I said that if the economy stays firm, the 10-year yield range should be between 3.21% and 4.25%, equating to 5.75% to 7.25% mortgage rates. If the economy gets weaker and we see a rise in jobless claims, the 10-year yield should go as low as 2.73%, translating to 5.25% mortgage rates. This assumes the spreads are wide, as the mortgage-backed securities market is still very stressed.

And now we have a new variable, a banking crisis which the Fed and some others believe could lead the economy into a faster recession, which the Fed has been pushing for some time now. In some ways, the banking crisis helps the Fed do their job because aggressive rate hikes have been unpopular and the Fed broke the regional banking system and now even a few global banks are in trouble too.

With this new variable, I am looking at the economic data differently to see whether we get the credit contraction the Fed wants to see to stop inflation, or if they have the tools to keep the banking crisis at bay so the economy can expand, making their fight against inflation harder. We will look at the data each week to determine the answer.

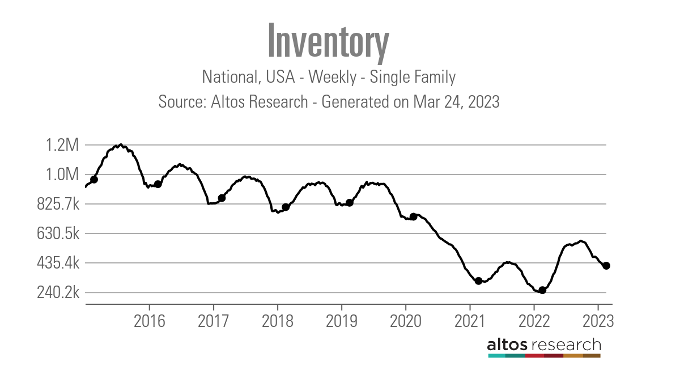

Weekly housing inventory

Looking at the Altos Research data from last week, the big question is whether we are finally starting to see the seasonal increase in spring inventory. Last week I was hopeful that the inventory increasing slightly would be the start of the spring rise, but this week we saw a slight decline.

- Weekly inventory change (March 17- March 24): Fell from 414,278 to 413,169

- Same week last year (March 18- March 25 ): Rose from 245,776 to 251,522

- The bottom for 2022 was 240,194

As you can see from the chart below, we are far from the normal levels we enjoyed in the previous expansion.

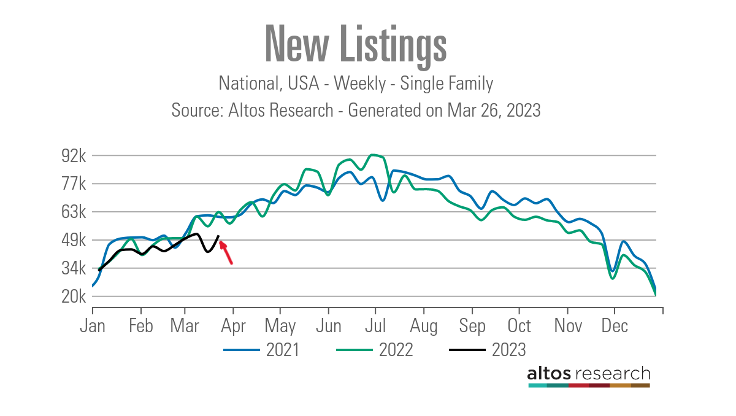

One piece of good news last week was that the new listing data, which saw a significant collapse two weeks ago, rebounded excellently to return to a usual trend. I was hoping that week’s new listing data was just a one-off in the data line and not a more significant trend of new listing falling, and that looks to be the case now.

This made me very happy because the last thing the housing market needs is for new listing data to decline more than it has been this year. Of course, new listing data is down noticeably year over year, but last week’s increase made me feel a lot better about the year. This was the weekly listing data during the COVID years:

- 2021: 60,177

- 2022: 62,548

- 2023: 50,800

Compare that weekly listing data to the pre-COVID-19 levels:

- 2015: 108,685

- 2016: 76,109

- 2017: 79,676

As you can see, we had more new listing data back then, even though mortgage rates were higher than in 2021.

Last week’s existing home sales report from NAR shocked many people, excluding me, for the big rebound in sales. That report didn’t show any inventory growth and we are still below 1 million active listings.

So we have had the biggest one-year sales decline in history and a significant rebound in sales for one month. During this entire period — from 2022 through 2023 — this is where we are on total inventory levels: 980,000, far from the historical norms of 2 million to 2.5 million.

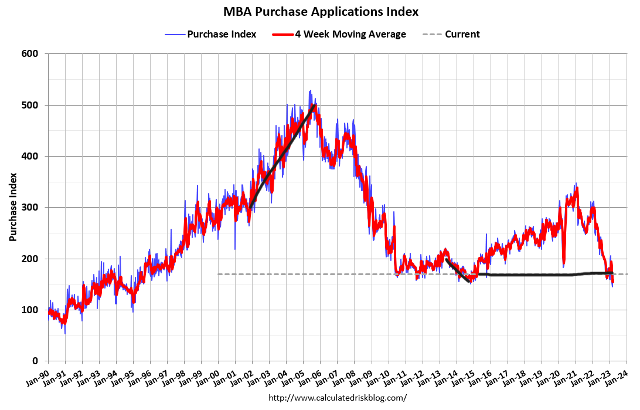

Purchase application data

We had another positive print on purchase application data, 2% week-to-week. When mortgage rates rose from 5.99% to 7.10%, we had three weeks of negative data and now we have had three weeks of positive purchase application data.

Overall, since Nov. 9, 2022, purchase applications have had more positive than negative data, something I talked about on CNBC last week.

Since we have a shallow bar in this data line, it tends to be very sensitive to rates, and mortgage rates themselves have been wilder than what we are accustomed to in the previous decade, where we had a range between 3.25%-5%.

Imagine the housing market if rates were in the low 5% range for a long time, not this wild Mr. Toad’s ride we see. Outside of that, it’s hard to get a mortgage rate shock like last year when rates moved from 3% to 7.37%. What happened last year will go into the record books.

The week ahead

Of course, all eyes are on the financial markets and what might come out of the woodwork next.

As I write this on Sunday night there are reports that First Citizen Bank will likely be the buyer of Silicon Valley Bank. I will closely monitor the 10-year yield to see if we can break that Gandalf line in the sand or if it will reverse course as we have in the past. Remember to focus on the closing on the 10-year yield more than the intraday trading actions.

This week we don’t have too much economic data, but the home price report will come out on Tuesday and pending home sales on Wednesday. The pending home sales data might reflect some of the negative three weeks of purchase apps we endured when mortgage rates moved from 5.99% to 7.10%.

Also, later this week, I will write an article on how to look at housing economics if the Fed gets its job-loss recession and how and why we shouldn’t compare it to the 2008 period or the COVID-19 recovery period. I can already see some people making the same mistakes they made with the COVID-19 recession.

Some Federal Reserve members are discussing a recession due to the banking crisis, so it’s time to discuss what housing will look like if this happens. For this week, keep an eye on the financial markets and the closing of the bond yield. If we see some weakness in pending home sales, that will relate to when rates spiked.

As always, one day, one week at a time, we will look forward, not backward, with this Housing Market Tracker.

Love your insights!

Nerds have their uses in society

Hey, you sleeping in today? I didn’t see a 4/3/23 update. See what happens when you get us hooked on data? Need my fix Logan.

Hi Joshua,

We just published today’s tracker, sorry for the delay!

https://www.housingwire.com/articles/housing-market-tracker-still-no-spring-inventory-lift/

Best, Diego