August is upon us, and the growth in the rate of new infections appears to be slowing. Vaccine development is progressing with some promising early results. The time has come to start thinking about what life will be like on the other side of this crisis. What can we expect post COVID-19?

Lead Analyst

Some things will not have changed. I already hear murmurs from the fear-mongering housing bears that once the forbearance plans expire, we can expect to see a collapse of the housing market in America like we haven’t seen since the bubble years. This is the same sorry song the bubble boys have been singing for the last eight years, with just a new verse.

But there are several economic conditions today that were not present before the previous housing collapse that almost ensure that a catastrophic failure will not happen.

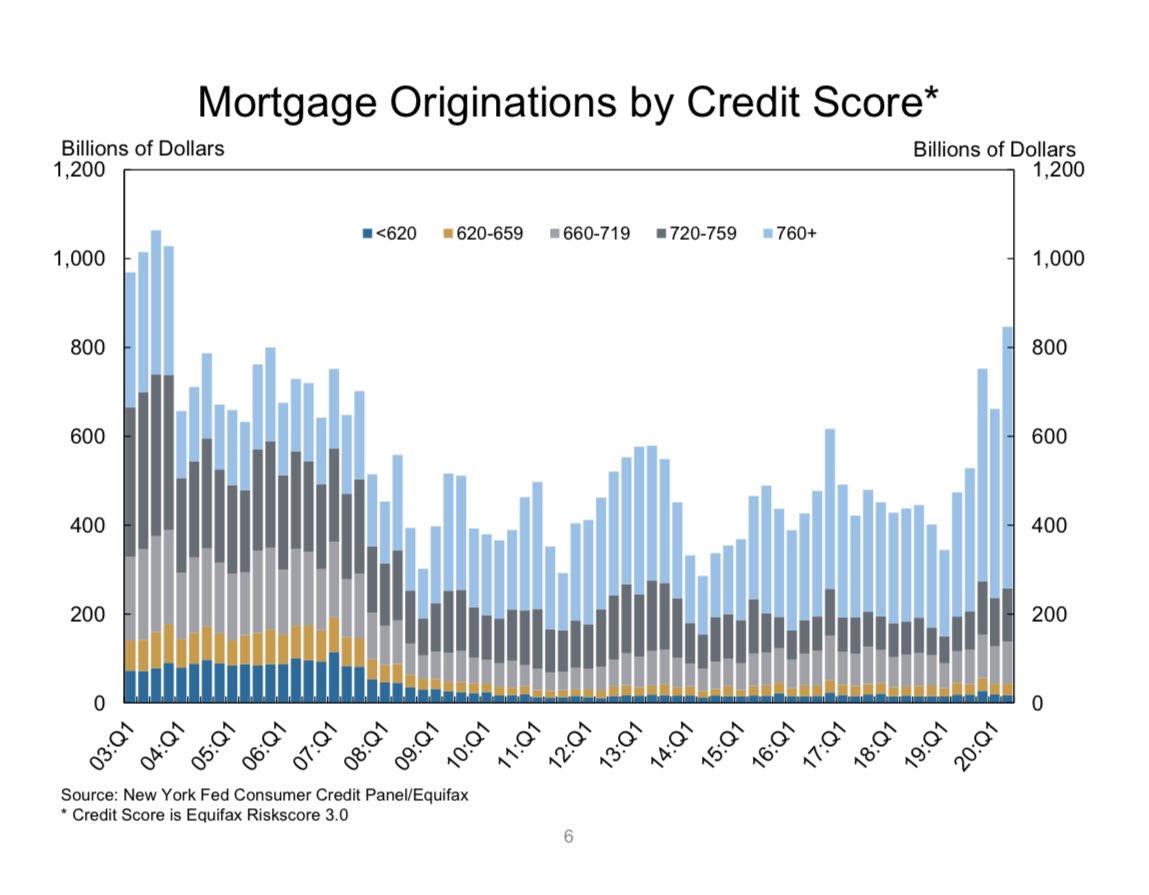

First and most importantly, the loan profiles in the previous record-breaking expansion from 2010 to 2020 were excellent. Borrowers had good FICO scores, and the lack of exotic loan products means that most borrowers began their loans with the capacity to own the debt. Plus, 20%-30% of all homes were bought with cash in the last 10 years. We didn’t have a boom in cash-out loans either, so the equity has not been whittled down like what we saw from 2003-2006.

These borrowers were actual homeowners, not speculators looking to flip homes to make a quick buck. Everyone who bought a home post-2010 can own the debt, and most have refinanced to a lower rate. These conditions are very different than those that preceded the last financial crisis and housing collapse.

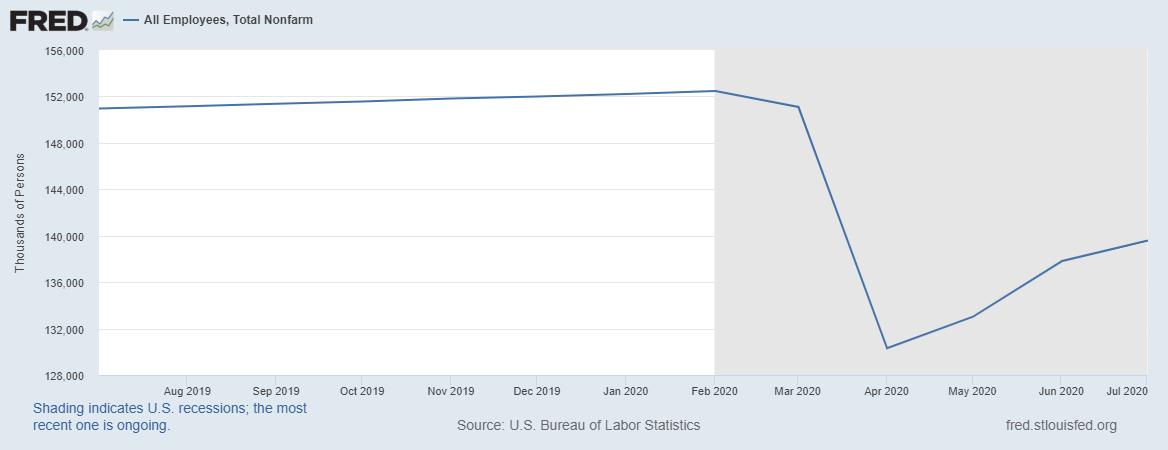

Still, many are concerned that the massive job losses in the last seven months could have significant deleterious effects on the housing market. This is a legitimate concern. But remember, we have regained 9.3 million jobs that were lost due to COVID-19, and the bulk of the jobs lost and regained are tied to those with renter financial profiles, not homeowners. To be sure, some of these job losses are related to homeowners — be it the primary or secondary wage-earner in a dual-income household. Many of these folks have taken advantage of forbearance plans to stay in their homes.

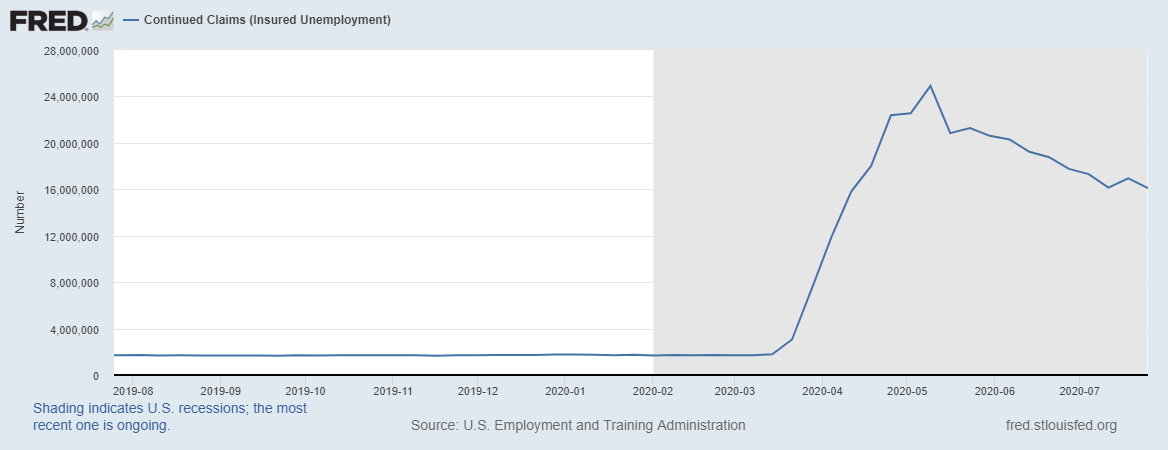

Since homeowners were able to own the debt when they took these loans, if some lost then regained full employment, we should see, after a lag period, people coming out of forbearance. With three straight positive job reports and the falling of continuing unemployment claims, I expect increased discontinuation of forbearance over the next 8-10 months.

Some homeowners do need a dual-income household to be able to make their payments. Jobs must come back as a second wage-earner is critical to keeping the home for some families.

My American bear friends might counter to say that the enhanced jobless benefits are keeping these homeowners afloat, and once this extra payment ends, we can expect to see a glut of distress sales that will create a bubble crash in home prices. To these people, I say, “Why always assume the worst, even when the evidence doesn’t support it?”

The nested equity position of current homeowners in a rising home-price year doesn’t mean a massive foreclosure distress market is just months away.

Be the detective, not the troll.

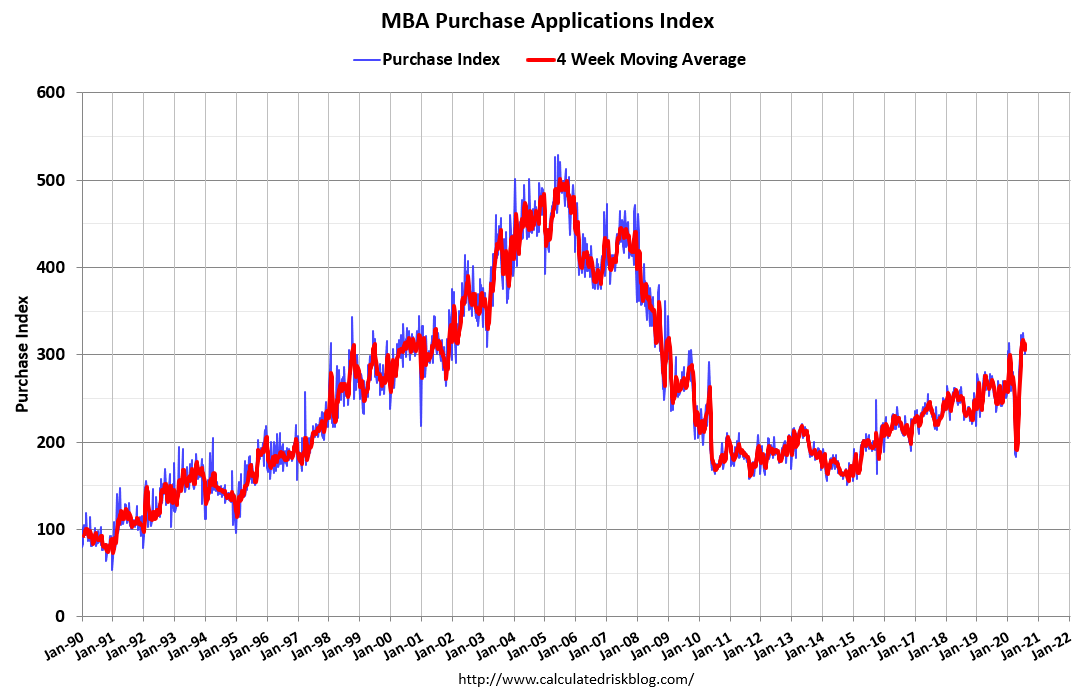

The U.S. housing market has strong fundamentals despite the current crisis. Amid the most significant health and economic crisis in recent history, housing was the first sector to bounce back. Mortgage Banker Association Purchase Application data has had year-over-year growth for the last 11 weeks, with double-digit growth for 10 of those weeks.

I will be watching the forbearance data for the next 12 months. If we regain most of our jobs back, then the bears have absolutely zilch to support a 2021 bubble home price crash. There is a big difference between home price growth slowing down, a slight decline year over year, and the epic bubble crash.

Before the 12-month forbearance plans expire, I expect some people to voluntarily discontinue their participation. With the current low mortgage interest rates, some may want to get out so they can refinance. The waiting period for refinancing after forbearance has recently been reduced to three months from 12 months.

In December of 2020, I will take another look at the supply risk from forbearance. However, for now, you have some data lines to track to make your own assumption for 2021 and 2022. Keep an eye out for the job data and the forbearance data to see if we can see a clear trend that people are getting off this program because they do have the capacity to own their home payment.

I agree with this article for the majority of households – most of which are driving the health of the housing market. Wtih that being said, I think the impact on low-to-moderate income borrowers/neighborhoods will be more significant than some may expect. Our forecast shows purchase originations to LMI borrowers dropping as much as 35-40% from 2019 to 2020, with a much slower road back in 2021 and beyond.

Even if your estimate of supply risk due to forbearance is significantly off the mark, the fact that inventory levels (in San Deigo 92106 for example) being a minimum of 300% less today than they were during the Great Recession of 2009, will prevent any hemorrhaging of values as it pertains to Real Estate.