On Wednesday, existing home sales collapsed near the lows we saw during COVID-19 and back in 2007 when the housing bubble burst. In addition, this is the fourth straight month of inventory declining, while days on the market are growing! Confused by this? I hear you; let’s dive deeper into today’s report.

From NAR: “In essence, the residential real estate market was frozen in November, resembling the sales activity seen during the COVID-19 economic lockdowns in 2020,” said NAR Chief Economist Lawrence Yun. “The principal factor was the rapid increase in mortgage rates, which hurt housing affordability and reduced incentives for homeowners to list their homes. Plus, available housing inventory remains near historic lows.”

One of the housing economic realities that I have been trying to stress this year is that a traditional seller of a home is typically a buyer as well. This explains why total active listing inventory data has been stable over the decades, with the exception of 2006-2011, when those forced distressed credit home sellers couldn’t buy.

Since the credit standards have improved post-2010, we shouldn’t see distressed sellers until a job loss recession happens, even if sales fall noticeably. This happened during the early months of COVID-19, and we have not seen the panic selling in 2022 like some people predicted.

Housing inventory

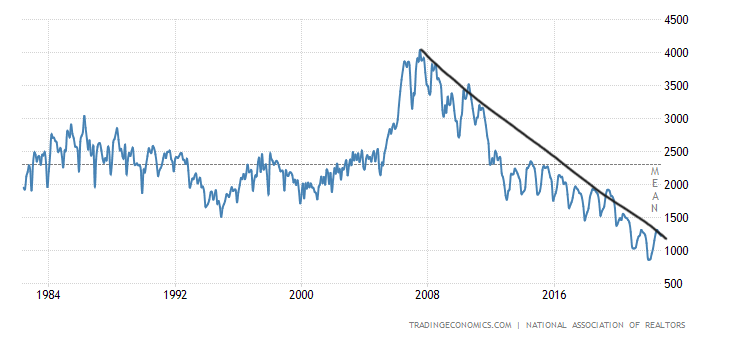

Today, inventory is almost 900,000 active listings below the lowest level of the four-decade average between 2 million and 2.5 million.

Inventory is now down again in the NAR report; this is the fourth month of inventory decline, now running at 1.14 million. The all-time lows were around 860,000 this year, and the all-time high was a tad over 4 million in 2007.

We have had two historic events that created a waterfall dive in demand recently; we now have precise data showing new listing data declining with those events, which shows how important that data line is to housing demand. This is the biggest story in housing.

For a decade, the traditional view on housing has been that when demand collapses, inventory will spike higher, which is what we saw during the years when the housing bubble burst.

I have never believed in this concept because of how the housing market credit channels work. I have stressed that inventory can grow through a weakness in demand over time. This means what we saw in 2005-2008 with the inventory spike was a historic event that hasn’t been replicated at any time in recent U.S. economic history.

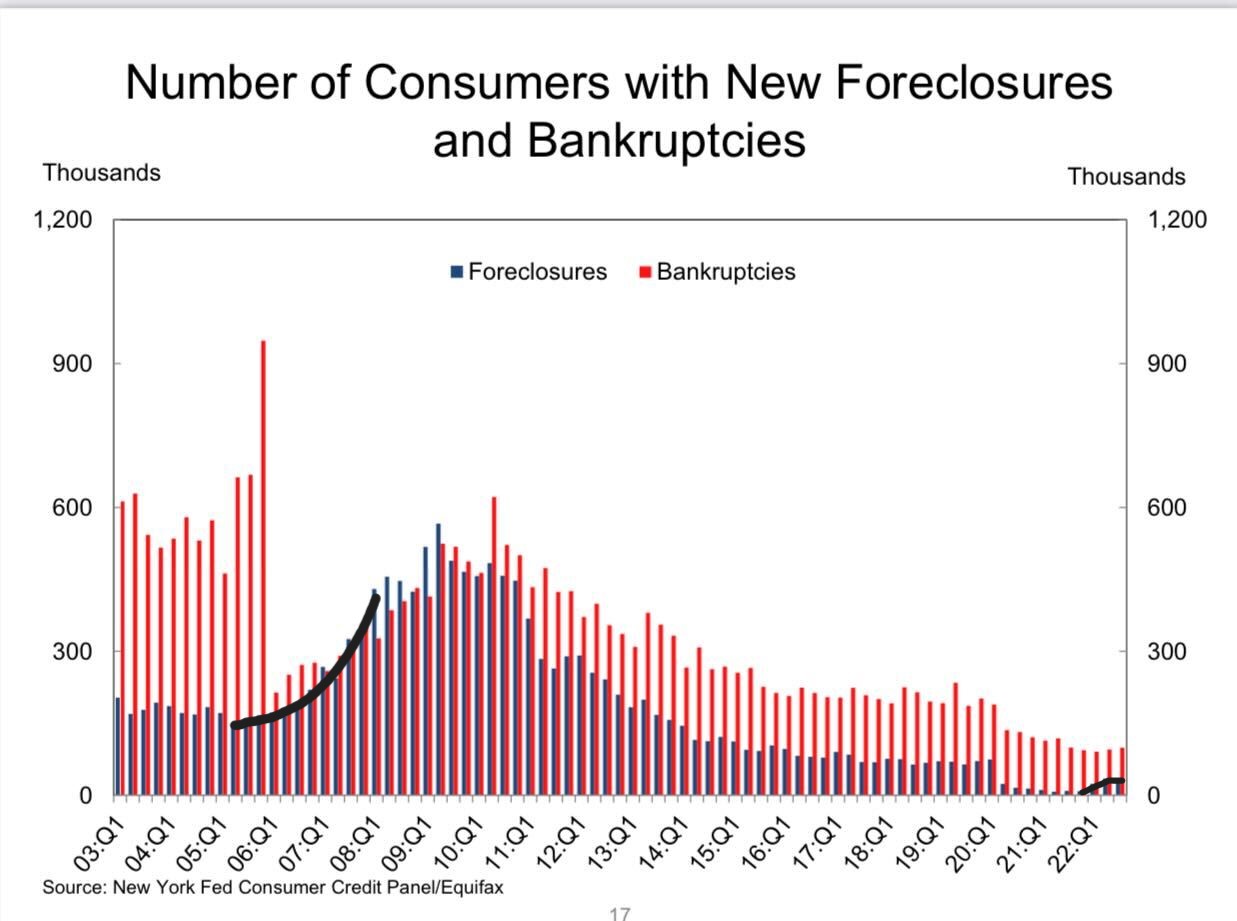

We have one data line that clearly shows the credit stress in the system, and it’s been my favorite chart at all my events (see below). Without significant credit stress in the system, we can’t ever assume we will see inventory scale spikes where sellers will not be able to buy homes because of a foreclosure or short sale.

We can believe in a forced equity seller premise, where someone loses their job and needs to sell their home to gain access to money. That is a real live talking point, but it will require a job loss recession. As we can see below, the U.S. housing market had high levels of credit stress in 2005 through 2008; then, after all that, we had the job loss recession. None of that has ever happened again since 2012.

Hopefully, this explains why total active listings are still low, and the NAR data has now shown four months of decline. We have a shot at having total active listings below 1 million over the next two months because demand is picking up during a seasonal inventory decline period.

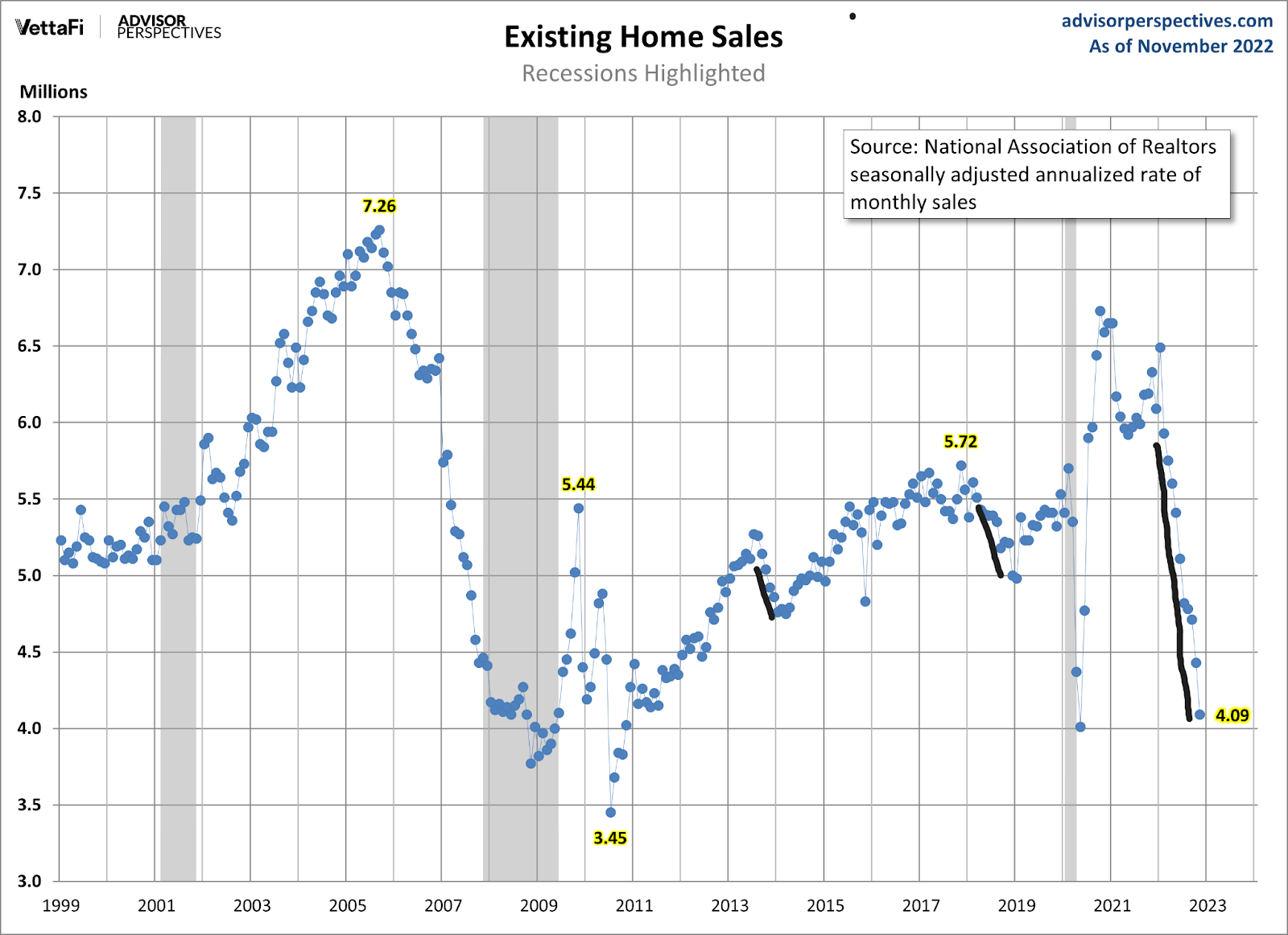

Below, you can see the decline in sales data, which is not as sharp and short as we saw during COVID-19 but a waterfall dive in demand nonetheless. Mortgage rates spiked in March, and then the new listing data started to decline at the end of June. My line in the sand has always been 4 million on the monthly existing home sales prints because it’s been a rare event that sales go below that level post-1996.

We have broken under 4 million existing home sales only twice post-1996. First was the tail end of the housing bubble bursting in 2008, and second was in 2010 in the aftermath of the homebuyer tax credit when sales were pulled forward and then collapsed.

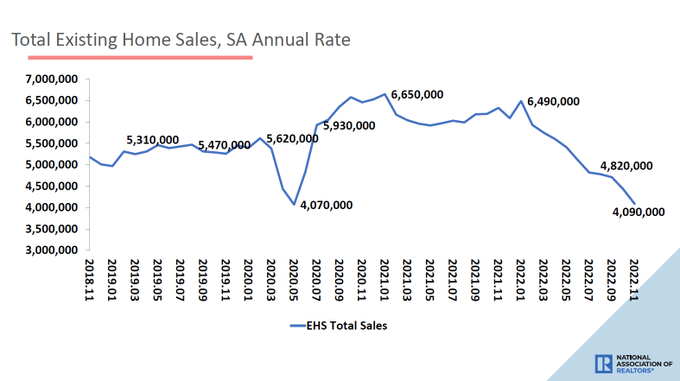

From NAR: Total existing-home sales waned 7.7% from October to a seasonally adjusted annual rate of 4.09 million in November.

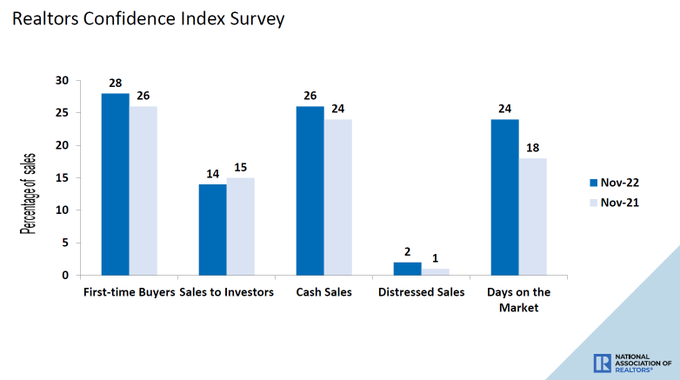

One of the most encouraging signs I see in today’s report, which I also loved in the last report, is that the days on the market are growing.

I am not, nor will I ever be, a fan of a housing market with days on the market in the teens or lower. This means we don’t have enough active listings for buyers, forcing people to bid against each other. I consider this growth year over year from 18 days to 24 days as a plus and a step toward a more normalized housing market.

NAR: First-time buyers were responsible for 28% of sales in November; Individual investors purchased 14% of homes; All-cash sales accounted for 26% of transactions; Distressed sales represented 2% of sales; Properties typically remained on the market for 24 days.

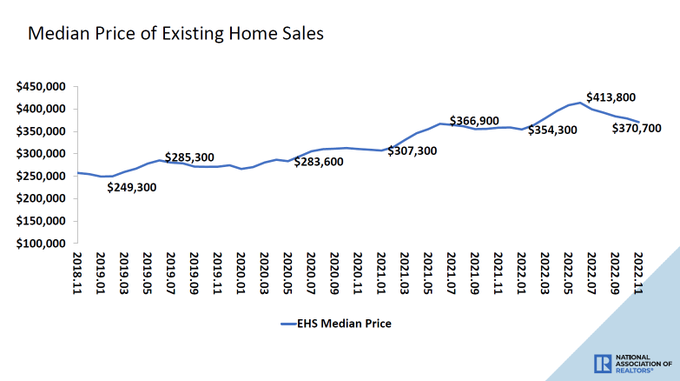

Home-price growth is cooling off dramatically, which is another awesome thing about housing this year. Yes, I know I am very biased here. Since February 2022, I have labeled the housing market savagely unhealthy as home prices have escalated well above my 23% home price growth model for 2020-2024 in less than two years.

This is why my rants of needing higher mortgage rates went into overdrive back then. However, now we are working our way back to a normal marketplace, which is good, not bad.

NAR: The median existing-home price for all housing types in November was $370,700, an increase of 3.5% from November 2021 ($358,200), as prices rose in all regions. This marks 129 consecutive months of year-over-year increases, the longest-running streak on record.

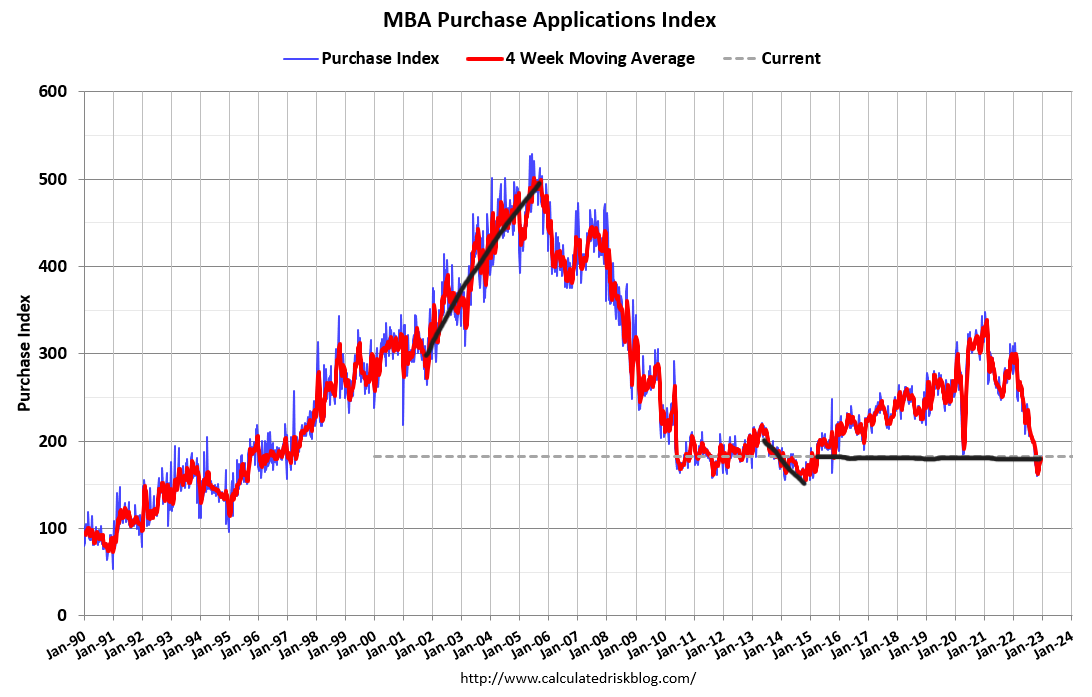

Purchase applications

The other housing news of the day, the forward-looking purchase application data, had another positive trend data line report. The week-to-week action saw a slight 0.1% decline, but now the year-over-year decline is 36%. As crazy as this sounds, that is 10% above the lows we had this year when this index was down 46% year over year.

Now, we need to add some context to this data line.

During the months of October 2021 to January 2022, we had a rare volume rise in the purchase application data, which took existing home sales toward 6.49 million in January of this year. This meant that all housing data, especially purchase application data, would have extremely hard comps to work with this year from October to January.

When I saw where trend sales data was going, I was anticipating that purchase application data would be down on average between 35%-45% year over year from October to January. So far this year, we have been down 36%-46% during this period. So, the data looks normal to me, as I was anticipating this.

What I didn’t anticipate was how well the market reacted to mortgage rates that went 1.25% lower in a short amount of time. This sent this data line positive for seven straight weeks, making us rise from the bottom decline of 46% year over year to now just 36%.

This means, for now, we have found a bottom in the data and bounced off the lows with positive trending data. This means in a few months, the existing home sales data should look better as this data line looks out 30-90 days.

The big takeaway in today’s existing home sales report is that we need to see new listing data grow in 2023 to get more home sales. Some people might believe that new listing data being negative is good for the housing market because it means inventory is stable. I believe this is the wrong way to look at the housing market. We want to see people list their homes and move when they want to. That is just a function of life; not everyone sits in the same home for 18 years like me.

Hopefully, in 2023, when we see the traditional inventory rise, this will come with new listing data growth, and we can get the total national inventory levels back to 2019 levels, which I will be very happy to see.

The housing market couldn’t take the shock of mortgage rates moving from 3% to 7.375% in one year, and this forced some people to change their minds about selling their home since they will have to buy another one. Hopefully, a more stable mortgage rate market means new listing data can grow in 2023.

Outstanding analysis as always. Thanks for the clarity.

With exisitng home sales, it’s always about purchase application data looking forward; whenever we see a waterfall dive or spike higher in the data, there is an inflection at some point. However, for now, it’s just a stabilization factor.