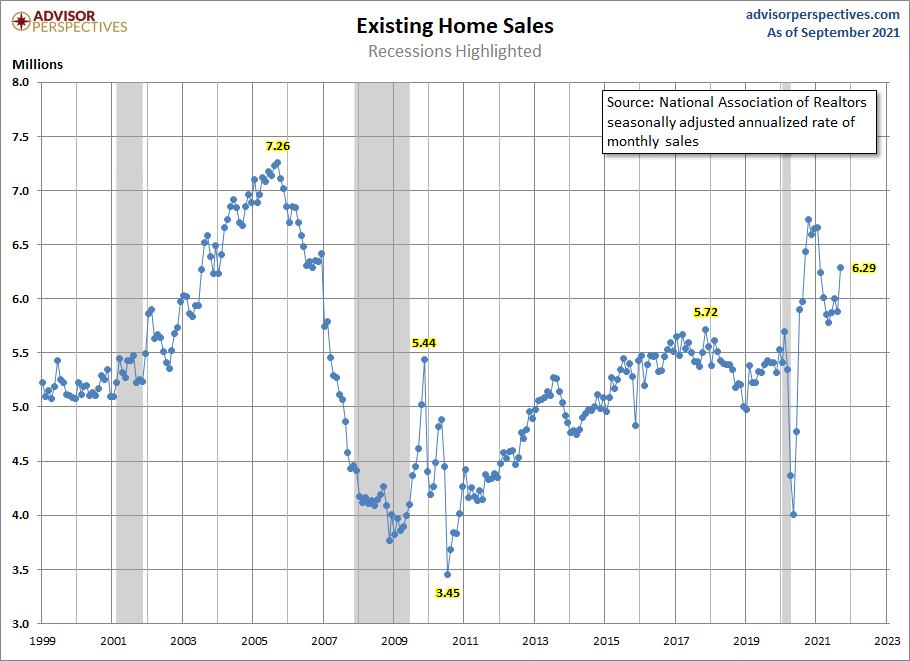

The National Association of Realtors‘ existing home sales report for September came in at an excellent beat of estimates at 6.29 million. Now that we are just 10 days away from Halloween in 2021, we can all chuckle a bit at how wrong the housing bears of 2020-2021 have been. Especially all those crazy cats on YouTube forecasting the 2021 collapse of housing due to forbearance.

Don’t worry, though, I have heard that some have moved their crash to 2022 or an undisclosed location. Remember to believe in people who believe in economic models and dare to do forecasting every year. Economics done right should be boring. Never forget: you want to be the detective, not the troll.

So far this year, every existing home sales print has been higher in 2021 than the closing level of sales in 2020, which was 5.64 million. With only three reports left in the year, we can safely say that existing home sales in 2021 will be higher than 2020 levels. Also, 2020-2021 will have more home sales from mortgage buyers than any single year from 2008-2019. This looks perfectly normal to me.

One thing about this report is that it’s better than the sales trends I was looking for in 2021. Earlier in the year, I wrote: “The rule of thumb I am using for 2021 is that existing home sales, if they’re doing good, should be trending between 5,840,000-6,200,000. This, to me, would be considered a good year for housing.”

A big theme of my work since last year was to talk about how housing data will moderate because the COVID-19 surge in demand was only make-up demand. When the data moderate, we will find a base to work from and take it from there. This happened right on cue for 2021. This type of action, for me, isn’t a surprise. I believe what happened is that many people who are typically housing crash bears saw moderation as terrible weakness and went into crash cult mode and blew it badly.

I had anticipated a few prints under 5.84 million, but we only had one report that came below that so far. So, all in all, 2021 looks good for the existing home sales market. If we don’t see any prints under 5.84 million, I would consider that a slight beat on demand this year.

The main reason why housing has done better in the years 2020 and 2021 is that we just got a simple kick in demand from the most significant housing demographic patch ever in history, as ages 27-33 are the biggest group ever. Then when you add move-up, move-down, cash and investor buyers together, we should be able to always have total home sales — both new and existing — at 6.2 million or higher. This is something that couldn’t happen in the years 2008-2019. So far 2020 and 2021 are looking just right.

Of course, like everyone who has economic models for their work, you have to look for deviations from the model. For housing in years 2020-2024, housing had the ability to outperform unlike the years 2008-2019. One area of concern was if home prices grew above the 23% cumulative growth during 2020-2024, then that would be a red flag. Of course, what we have seen in 2020 and 2021 is unhealthy home price growth, so not all is rosy in housing land. For myself, I am rooting for home-price growth to cool down, which would be the best thing for the housing market.

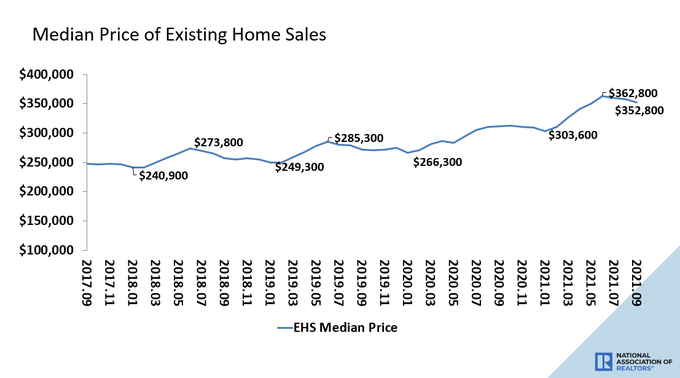

From NAR: The median existing-home price for all housing types in September was $352,800, up 13.3% from September 2020 ($311,500), as prices rose in each region.

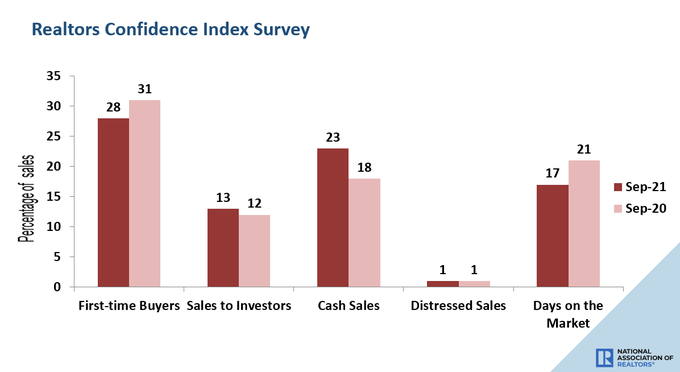

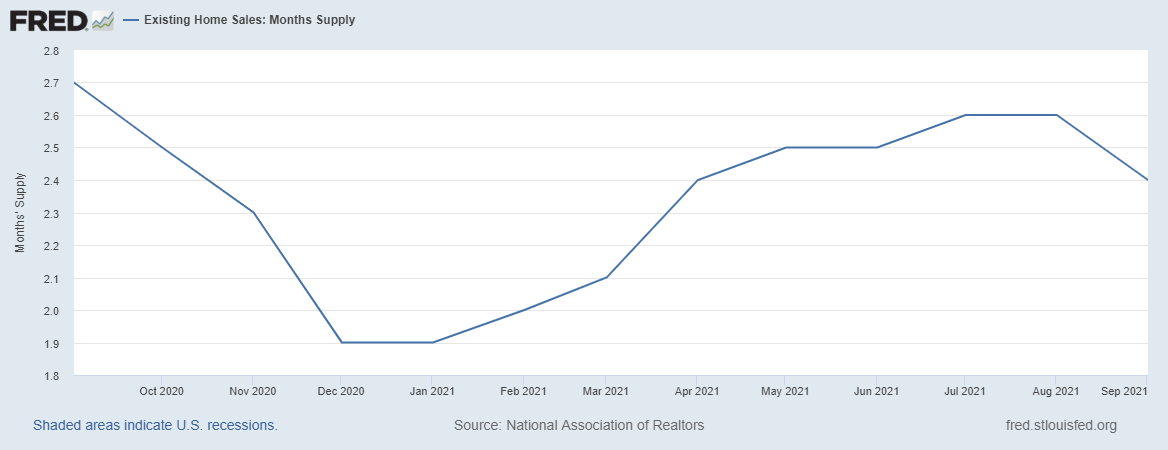

One data set I like to keep an eye on regarding progress for what I want to see in the B&B housing market (boring and balanced) is for days on the market to grow. Still, being a teenager is not a healthy sign; we want days to grow and cool down this market to give people more choices.

From NAR: First-time buyers accounted for 28% of sales; Individual investors purchased 13% of homes; All-cash sales accounted for 23% of transactions; Distressed sales represented less than 1% of sales; Properties typically remained on the market for 17 days in September.

Also, you can see above that the sales to investors grew 1% year over year. I know many people in America believe that the housing market is booming because of investor purchases. That is so cute. It’s 13% of this report. Primary resident mortgage buyers always drive accommodation; when they fade, so will housing. this is why mortgage rates rising is more important than sales to investors.

Many people pushing the investor theme are mostly extreme right-wing economic thinkers who believe the world is a nightmare because of the Federal Reserve. Also, much of the extreme left-wing think that housing won’t go anywhere because millennials can’t buy homes because of student loan debt, even though they make up the most significant percent of homebuyers in America.

Those who know me well know that I stress that the extreme left and right have been crying about America since 1790, and our country has smoked them all since 1790. These people can’t and won’t change, so they will always be ice skating uphill until the afterlife. Economic cycles come and go; these two groups went to extreme levels post-2008 and simply don’t have the financial training to track economic data without their bias showing. It is what it is.

An additional point to note from the NAR existing sales report was this phrase: “However, sales decreased 2.3% from a year ago (6.44 million in September 2020)” Remember that housing data will be negative year over year due to the high comps COVID-19 created with the surge in make-up demand last year. I believe some of this spilled over into 2021, so I don’t think we’ll have reasonable comps until March 2022 comes around. So, don’t read too much into the negative year-over-year print.

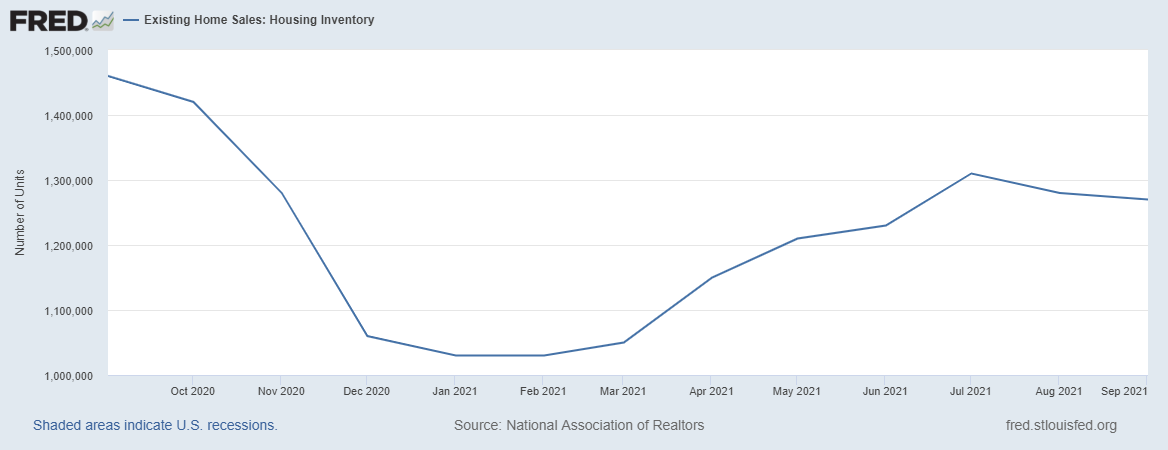

On the bad news, inventory is starting to do its regular fall and winter seasonal fade. I am rooting for inventory levels to get to 1.52 million and I’m still hoping for this to happen next year. For now, I can hope that the total inventory fade isn’t too bad for the remainder of 2021

All in all, this is a better-than-expected report demonstrating a better-than-expected sales trend. Since this is above my sale level trend after the moderation of the data has already happened, I will always look at any number above 6.2 million existing home sales as a beat. As long as people know that we don’t have a housing sales credit boom, then a lot of the data in 2020 and 2021 will make sense.

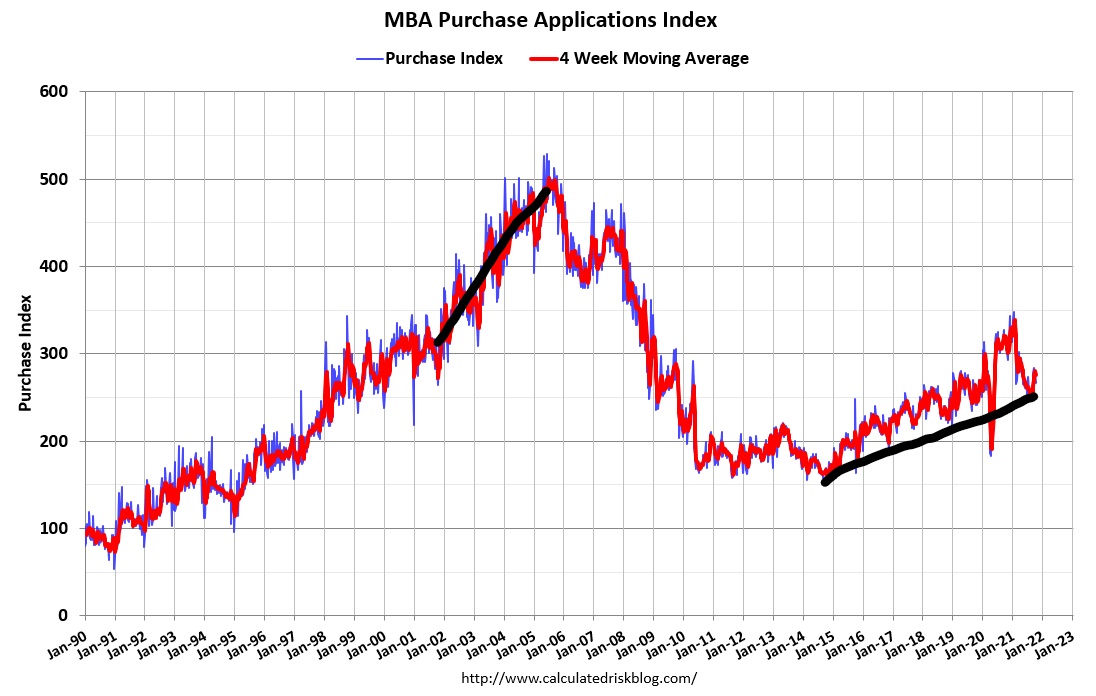

As you can see below, we just flexed our demographic muscle a bit more this year and last as we finally breached above the 300 level on the MBA index, something that I don’t believe could have happened from 2008-2019. As you can see below, this market doesn’t look similar to the demand boom push we saw from 2002-2005. This is why I love the idea of a demographic replacement buyer demand rather than a boom.

I know the 10-year yield has been rising recently; my peak 10-year yield forecast is 1.94%, so we still have a way to test my crucial level. When mortgage rates get to 3.75% and above, the housing discussion should change. However, that wasn’t past of 2021 forecast as the highest rate level range I had was only 3.375% -3.625%