In recent articles, I have written that although current sales data for the U.S. housing market has outperformed expectations, I expected these upward trends to moderate. Growth in home sales in recent months, I proposed, was primarily due to the catch-up demand from the stalled sales during the worst weeks of COVID-19.

Today, the National Association of Realtors reported a 2.5% decline in existing home sales compared to last month, which I guess could be considered moderation. But the bigger picture is this: We have had three consecutive months of more than 20% growth, year over year—and this is compared to the more robust sales in the second half of 2019.

From NAR : Total existing-home sales, completed transactions that include single-family homes, townhomes, condominiums, and co-ops, decreased 2.5% from October to a seasonally-adjusted annual rate of 6.69 million in November. However, sales in total rose year-over-year, up 25.8% from a year ago (5.32 million in November 2019).

The strong February existing home sales report set a precedent for the rest of the year, despite COVID-19. If we don’t end the year at 5,710,000 – 5,840,000 total existing home sales, it will be because COVID-19 temporarily paused housing activity. I expect those delayed sales to be shifted into early 2021.

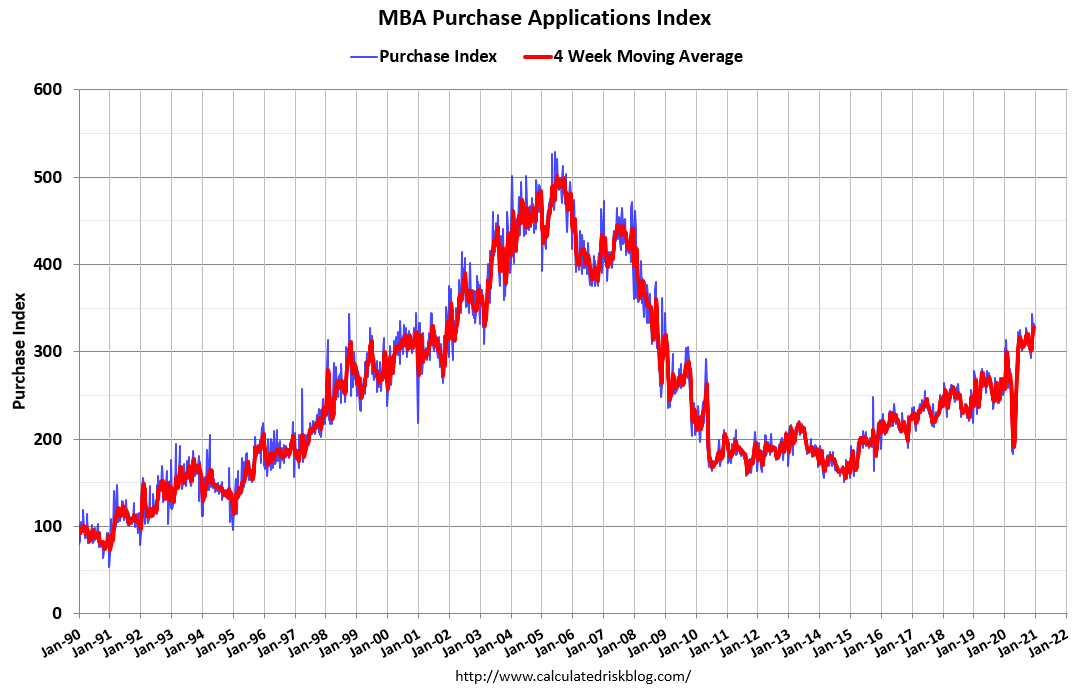

We see hints of this delayed home sales shift in the Mortgage Bankers Association’s purchase application data. We have had 30 straight weeks of over 20% growth on average, compared to last year. The cooling in purchase application volume that typically occurs after May, due to seasonality, did not happen in 2020.

In the last four weeks, year over year, growth in purchase applications has been: 26%, 22%, 24%, and 26%. Because this data looks out 30-90 days, we can get from these numbers that the market is still in make up demand mode. At some point in the future we will see moderation, but it hasn’t happened yet!

Because housing demand is at pre-cycle highs, we can infer home prices are not an issue for most buyers. However, this does not mean that real home prices may grow at an unhealthy pace in the years 2020-2024. This is my biggest concern for the market going forward. If we have greater than 4.6% nominal home price growth every year for the next several years, affordability will be an issue for some buyers.

The silver lining is that unlike in the previous cycle from 2002-2005, homeowners are in a much better financial position. Housing tenure at 10 years, all-time lows in mortgage rates and the best demographics for housing ever recorded in U.S. history all can facilitate unhealthy price growth if mortgage rates stay this low.

In the short term, existing home sales and housing data will moderate to a more normal trend. And this will be a good thing, so don’t buy into any doom and gloom forecasts based on some moderation of the “not-normal”: parabolic data. Keep in mind that the years 2020-2024 have the best housing demographics ever recorded in history, which means we have a healthy number of replacement buyers. Only higher mortgage rates can cool off demand – and that could be a good thing because the best housing market is a stable one.