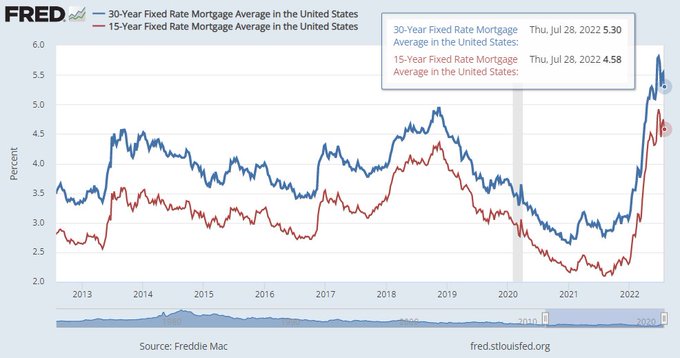

To say that mortgage rates have been on a wild Mr. Toad’s ride in 2022 is an understatement. In less than a year, we went from 2.78% on the 30-year fixed to as high as 6.28%, then recently got as low as 5% — only to have another move higher this week to 5.30%. People thought the mortgage rate drama in 2013-2014 was a lot when rates went from 3.5% to 4.5%. However, as we all know, after 2020, things are just more intense.

The question is, can lower mortgage rates save the housing market from its recent downtrend? To understand this, we need to look back into the past to realize how different this period is from what we had to deal with in the previous expansion when rates rose and then fell.

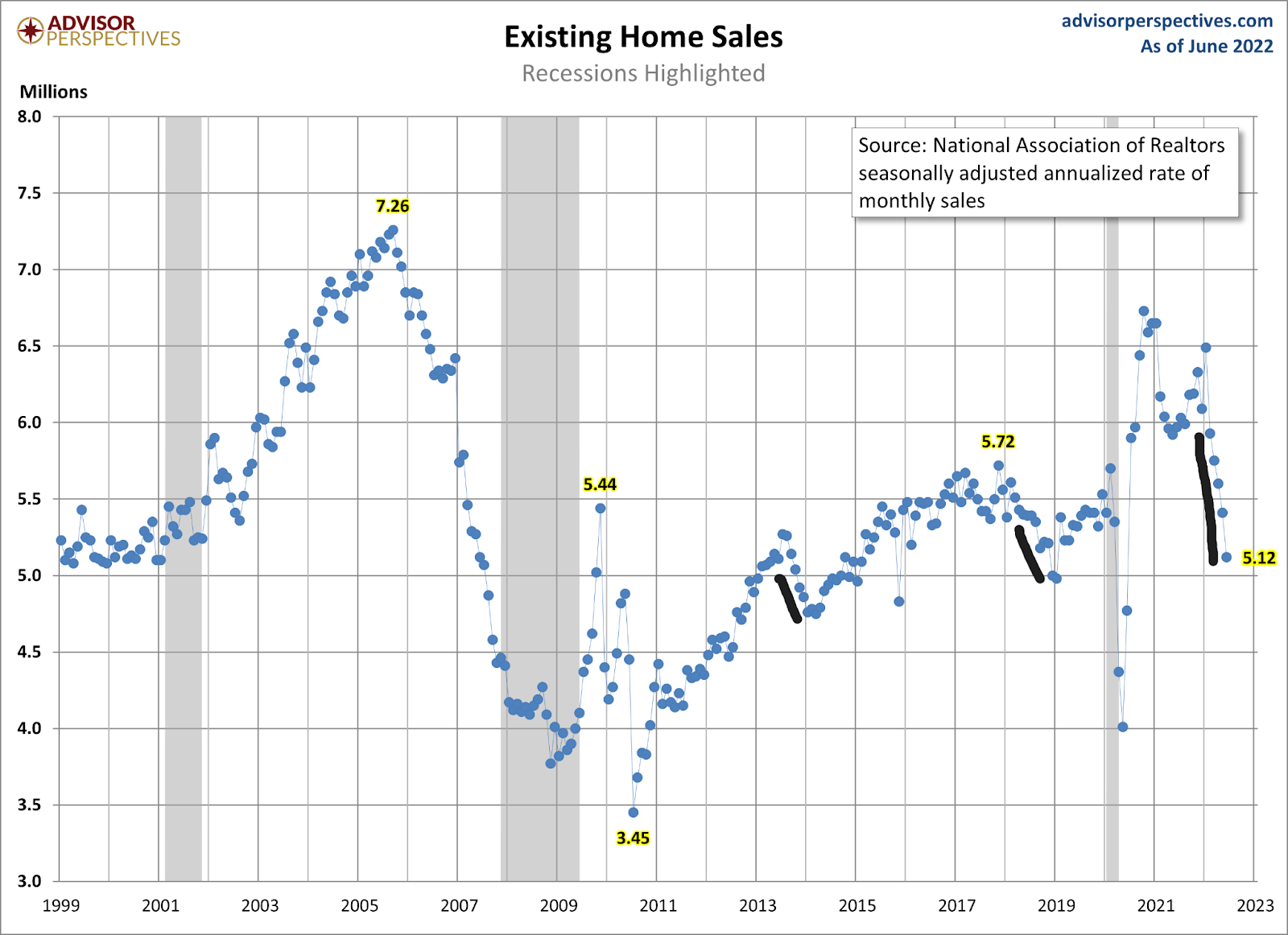

Higher rates and sales data

We can see that when rates rise, sales trends are traditionally lower. We saw this in 2013-2014 and 2018-2019. We know the impact in 2022, working from the highest bar in recent history.

The most significant difference now from what we saw in the previous expansion is that mortgage rates never got above 5% in the previous expansion. However, more importantly, we didn’t have the massive home-price growth in such a short time. It does make an enormous difference now that home prices grew above 40% in just 2.5 years.

This is why I focused my readers on the years 2020-2024, because if home prices only grew by 23% over five years, we would be ok. However, that got smashed in just two years, and prices are still rising in 2022. It’s savage man, truly savage with the mortgage rate rise. Yes, rates bursting toward more than 6% is a big deal in such a short time, but the fact that we had massive home-price growth in such a short time (and in the same timeframe) is even more critical.

While I truly believe that the growth rate of pricing is now cooling down, 2022 hasn’t had the luxury of falling prices to offset higher rates. So we can’t reference this period of time with rates falling as we did the previous expansion due to the massive increase in home prices and the bigger mortgage rate move. In 2018, sales trends fell from 5.72 million to the lows of January 2019 at 4.98 million. This year we have seen sales fall from 6.5 million to 5.12 million, and they are still falling.

Housing acts better when rates are below 4%

In the past, demand improved when mortgage rates were heading toward 4% and then below. Obviously, we are nowhere close to those levels today, barely touching 5% recently to only go higher in the last 24 hours.

Again, I stress that the massive home-price growth is different this time. However, with that said, considering the sales decline trends and that we have seen better-than-average wage growth, housing demand should act much better if rates head toward 4% and below.

I stress that higher and lower mortgage rates impact the market, but it needs time to filter their way into the economy. When I talk about the duration, this means rates have to be lower for a more extended period. People don’t throw their stuff down and buy a home in a second; purchasing a home is planned for a year. Rates would need to stay lower for longer into the next calender year to make a big difference.

Millions and millions of people buy homes every year. They have to move as well, so a traditional seller is a buyer most of the time when it’s a primary resident owner. Sometimes when rates go higher too quickly, some sellers can’t move, this takes a sale off the data line, but if rates fall quickly, they might feel much better about the process.

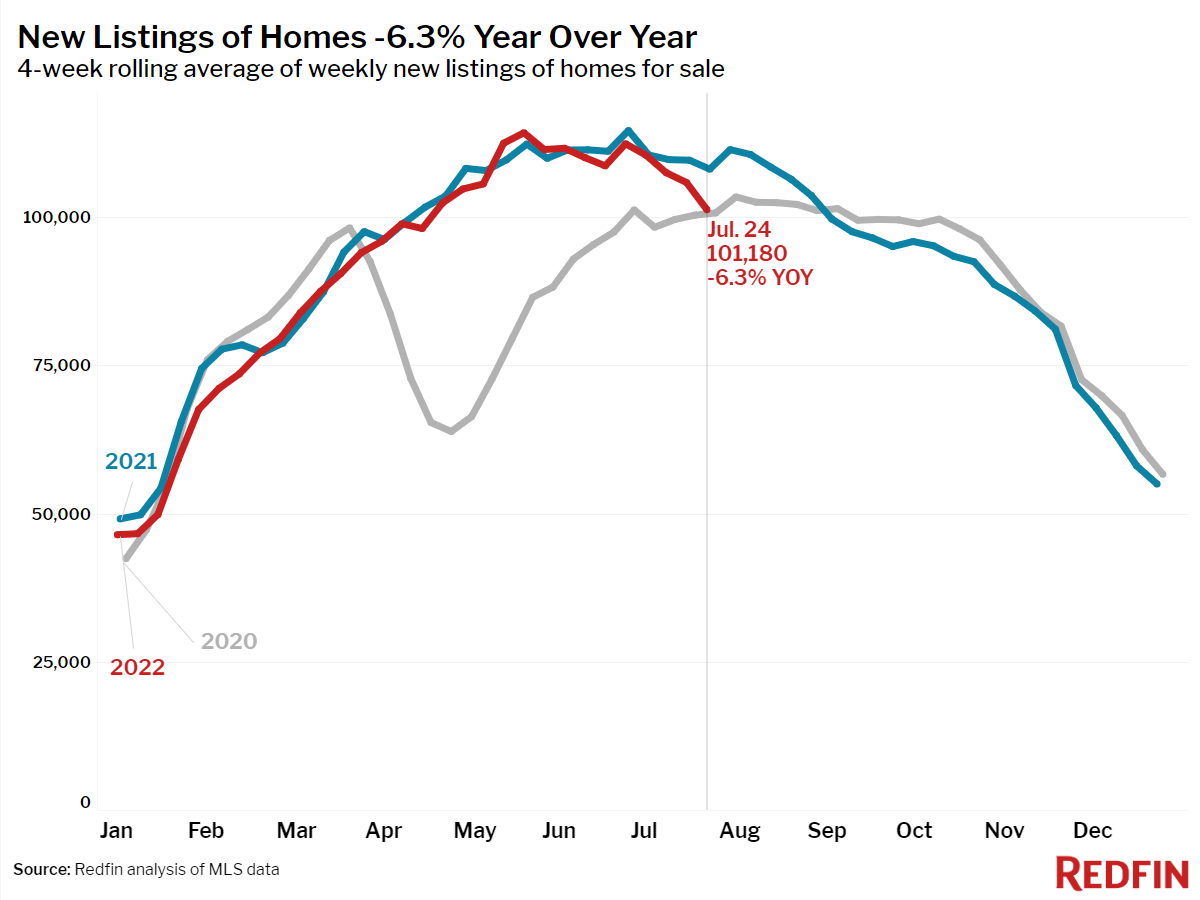

The downside of rates moving up so quickly is that some sellers pull the plug until rates are better. We see some of this in the active listing data as new listings are declining. Lower rates may pull some of these listings forward as people feel more comfortable with rates down; time will tell.

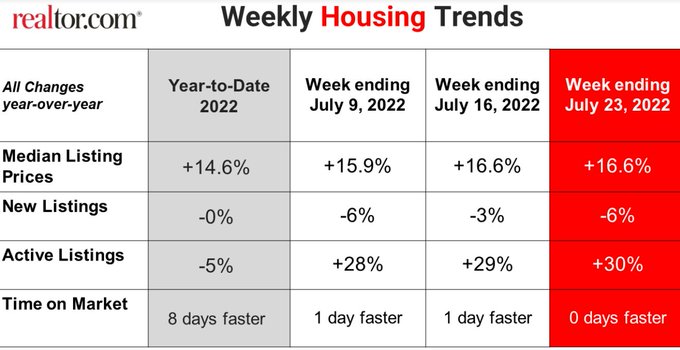

From Realtor.com

From Redfin:

Of course, a 1% move lower in rates matters, but keep in context where we are coming from and how much home-price growth we have had in just 2.5 years. This isn’t like the previous expansion where home prices were working from the housing bubble crash and affordability was much better back then.

When to know when lower rates are working?

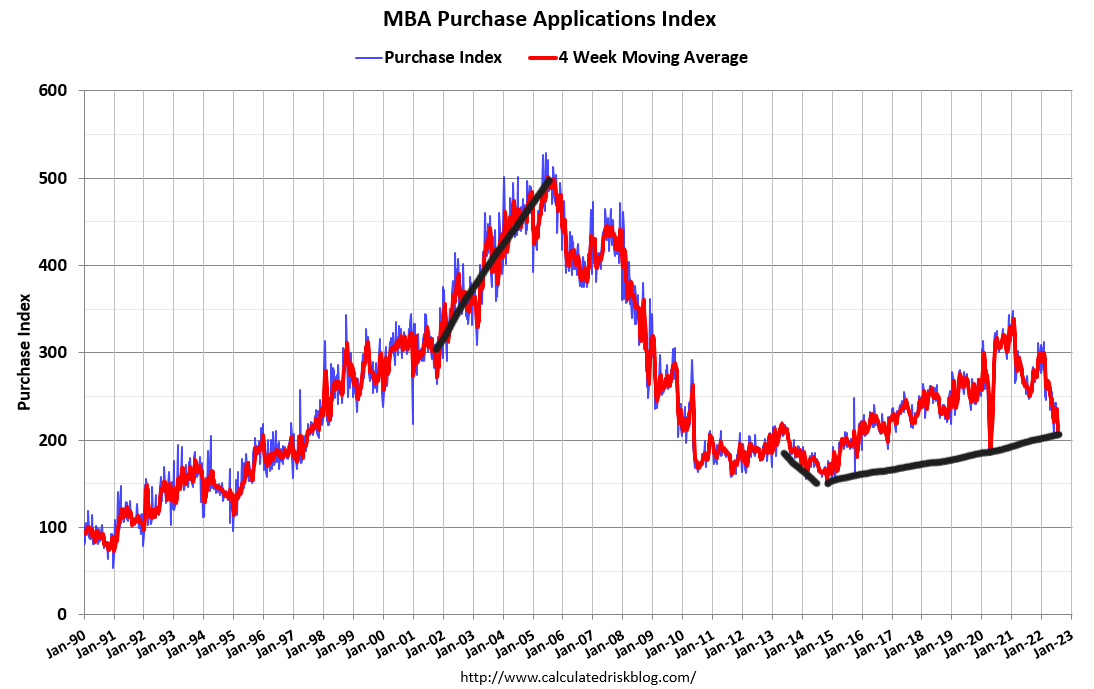

The best data line to see this take place is purchase application data, which is very forward-looking as the fastest data line we have in housing. Let’s take a look at the data today.

Purchase application data was positive week to week by 1% and down 16% year over year. The 4-week moving average is down negative 17.75% on a year-over-year basis.

This is one data line that has surprised me to a degree. I had anticipated this data to be much weaker earlier in the year. However, I concluded that 4%-5% mortgage rates didn’t do the damage I thought they would do. But, 5%-6% did, as I was looking for 18%-22% year-over-year declines on a four-week moving average earlier in the year. So, this makes me believe that if rates can get into a range of 4.125%-4.50% with some duration; the housing data should improve on the trend it has been at when rates are headed toward 6%. Again, we aren’t there on rates yet.

The builders would love rates to get back to these levels so they can be sure to sell some of the homes they’re finishing up on the construction side. Now assuming rates do get this low; what would the purchase application data look like? Keep it simple, the year-over-year declines will be less and less, and then when things are improving, we should see year-over-year growth in this index.

A few things about purchase apps: the comps for this data line will be much more challenging starting in October of this year. Last year’s purchase application data made a solid run toward the end of the year, which led existing home sales to reach 6.5 million. Next year we will have much easier comps to work with, so we need to keep that in mind. However, to keep things simple, the rate of change in the purchase applications data should improve yearly.

To wrap this up, lower mortgage rates should be looked at as a stabilizer first, but for them to change the market, we will need much lower rates for a more extended period. Also, we have to consider that rates moving from 3% to 6% is historical, and if rates fall, we have to look at housing data working from an extreme rise in rates that happened quickly. However, sales levels should fall if purchase application data shows negative year-over-year prints on a double-digit basis.

Since home prices haven’t lost this year, you can see why I used talked about this as a savagely unhealthy housing market. The total cost of housing had risen in a fashion that isn’t comparable to what we saw in the previous expansion when rates went up and down due to the massive increase in home prices. Also, we have to know that we aren’t working from a high level of inventory data as well. Traditionally, total inventory ranges between 2 to 2.5 million. We are currently at 1.26 million.

NAR total inventory data

We shall see how the economic data looks for the rest of the year and if the traditional bond and mortgage rate market works as it has since 1982, then mortgage rates will head lower over time. However, as of now, it’s not low enough to change the dynamics of the U.S. housing market.

Logan, are you still team higher rates?

Diego; Part of being team higher rates early in the year was that inventory levels weren’t getting better, and forced bidding was getting worse early on. If rates didn’t rise 3%, home price growth easily would have stayed 18%-24% year over year. The pricing power that home sellers and home builders have had is gone now, with rates higher. So, higher rates have done thier thing. The market dynamics have shifted.

Now, on the economic side, with my six recession red flags up, since housing is in a recession on the builder’s side of things, I know the limits of how much higher rates can go with economic data getting weaker. Traditionally post 1982, before a recession happens, bond yields and mortgage rates find their peak, and then they fall into a recession.

So, while I haven’t even reached my total inventory goal of 1.52 -1.93 million, I know if I keep on saying higher rates with the economic data getting weaker, then that would be going against all my work with the bond market, mortgage rates, and recessionary financial position.