I hear a lot of chatter about a boom in cash-out refinances, and the presumption seems to be that this is destined to wreak havoc on the housing market and the economy at some point. Cash-out loans have been growing over the past few years and it is also true that we have a recent history of excessive equity extraction factoring in a bust in housing. But there are several critical reasons why the recent uptick in cash-out refinancing is nothing like the cash-out boom of the early to mid-2000s.

First, the refinance boom’s main driver in the 2000s was unhealthy because of the marketplace’s speculative unhealthy lending standards. Home prices were growing at an unsustainable level from 2002-2005, leading to some excess risk-taking on inadequate loan debt structures.

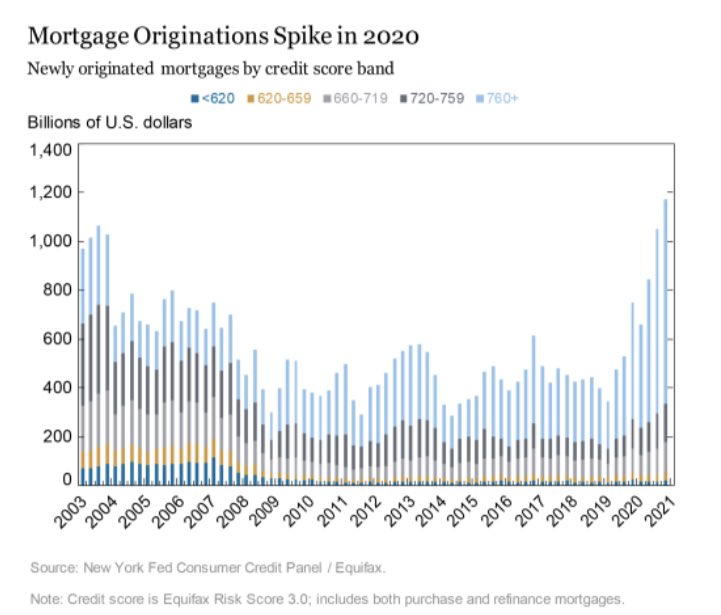

In the 2020 market, on the other hand, refinances were not driven just by an increase in equity but lower mortgage rates. Cash-out loan borrowers who increased their loan balances could get a more favorable rate than in previous years. Although mortgage refinance activity was the highest in 2020 than it has been since 2003, the reasons for refinancing and the quality of the equity loans are much different than they were in the 2000s.

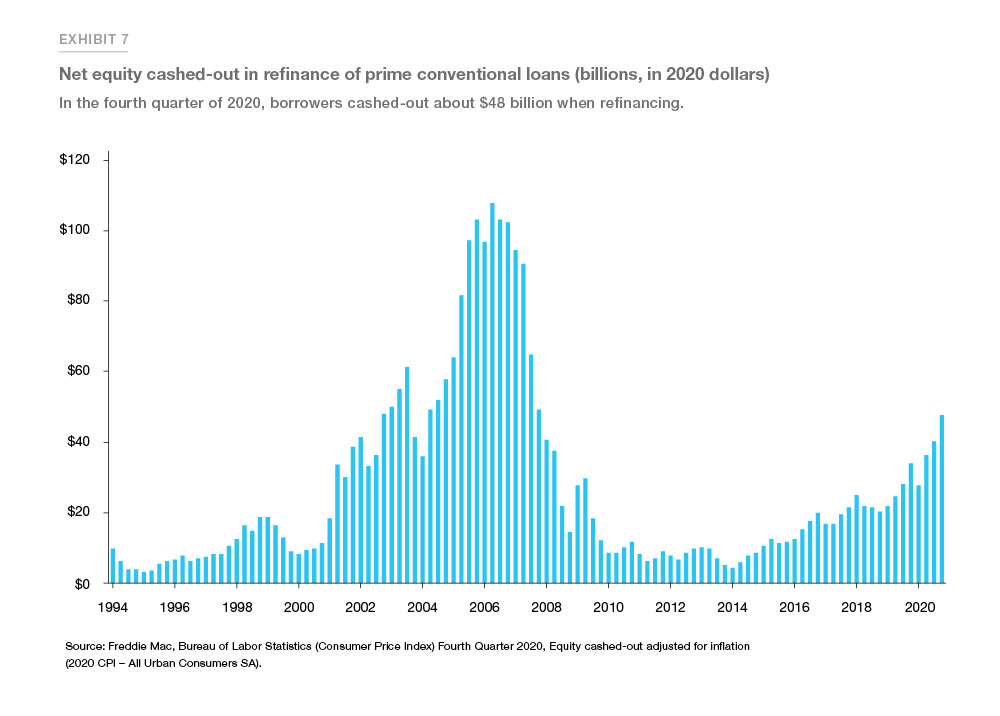

The graph below is from an article by Len Kiefer of Freddie Mac. This is an excellent article for those interested in diving into the minutiae of the 2020 refinance market.

If we dig a little deeper into homeowners’ balance sheets, we see that since 2010, cash flow and loan quality of mortgage holders were excellent.

Although homeowners built strong equity positions, they tended not to cash out on this equity as much because they simply didn’t need the money. COVID-19 changed that. What COVID-19 did was take mortgage rates below 3.5%, and that meant homeowners could, in theory, cash out on their home and have a lower mortgage rate than their current level. Remember, it took time to get rates properly lower, and for a brief while some lenders didn’t even offer favorable cash out loan rates and some credit did get tighter early in the crisis. However, in time, the downward push in mortgage rates created more demand than in the pre-COVID years for cash-out loans.

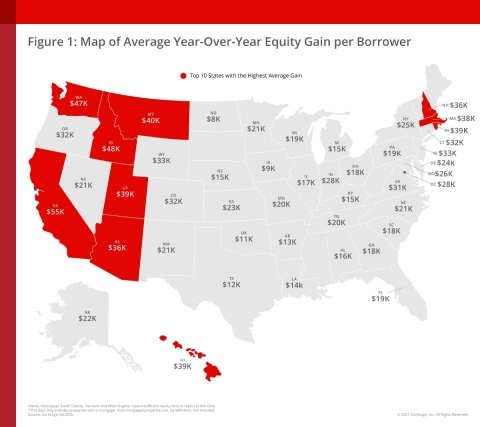

The second factor we need to consider when comparing the current uptick in cash-out refinancing and the previous boom is that today, homeowners aren’t borrowing much compared to the amount of nested equity in their homes. Per a recent report from CoreLogic, roughly 1.5 trillion dollars of equity was created by American homeowners last year alone.

The total amount borrowed in the previous year was nothing compared to the equity built. According to Freddie Mac, and here again I reference the article by Len Kiefer mentioned above: “In the fourth quarter, homeowners cashed out only approximately 0.25 percentage points of available equity through a cash-out refinance, far less that the over 0.5 percentage points extracted in 2006.

Remember, too, that current market conditions are such that we can expect mortgage rates to rise as the economy improves. When mortgage rates rise, cash-out loans and refinances will lose their appeal, so this so-called boom in the cash-out market is destined to be short-lived.

The third factor to consider when analyzing this issue is the debt structure of current mortgage loans compared to the 2000s. Fixed low-mortgage rates locked and an improving economy means we have homeowners with fixed low debt cost along with rising wages. Rising wages are one of the main reasons why those who predicted a housing collapse due to COVID-19 got it wrong.

American homeowners were financially solid prior to the COVID crisis. They had wage and equity growth and were able to refinance their debt to lower interest rates. This is why I stressed that homeowner loan profiles never looked better, because their fixed low debt cost vs rising wages just got better each year. We also just came from the longest economic and job expansion ever recorded in history. Without COVID-19 the American bears had nothing to hang their hat on.

After 2010, mortgage debt structure was very vanilla and boring. The majority of loans done post-2010 were fixed long-term loans that everyone qualified for. Exotic loan debt structures are thankfully largely a thing of the past. Today, homeowners are not forced speculators that need home prices to rise to refinance out of an exotic loan. We don’t have major loan recast rate risk vs. incomes. The people who bought homes in America post-2010 were, for the most part, legit homeowners, meaning they bought homes for shelter and stability for their family, not speculative financial assets. Boring debt might not be a sexy story. Still, it is very sexy to my eyes because it a healthy, financially responsible way to live.

In summary, the cash-out refinance boom (if you want to call it that) isn’t much of a story. Due to COVID-19 or not, some homeowners have decided to extract a relatively small amount of equity from their homes while refinancing to lower interest rates. For the overall housing market and the U.S. economy, this will not be a problem in the short, medium, or long term.

I get why the crazy crash cult housing bears are trying to turn this story into something more. As professional gifters and anti-central bank fanatics, that’s what they do. But when our learned economists and professors are caught trying to make this into some unfounded bad story, it makes me wonder if they don’t understand how solid homeowner households are that are employed. Haven’t we learned from the previous expansion that not all debt is bad?

An often forgotten fact is that the highest-income households typically have the highest debt along with the greatest financial assets. Adjusting to inflation, consumer debt really hasn’t grown much since the peak of the housing crisis, and the structure of that debt tends to be very boring and low risk.

The bottom line is that one needs to understand the debt holders’ underlying financial profiles before one makes a call regarding the short, medium, or long-term risk to the economy that these debts represent.

On a related topic, the 10-year yield recently closed at 1.64%, If you follow my work you know that this is a big deal for me. The economic model I proposed for how America would get back on track after COVID-19, which I called the “America is Back” model, required that the 10-year yield gets into a range between 1.33% – 1.60% in 2021. This range has been established this year.

The next thing is to see is if the 10-year can close above 1.64%, and get follow-through bond selling for the next day or two. If that occurs, we can see the 10-year up to 1.94%, which was the peak bond yield forecast for 2021. This can add 0.25% – 0.375% higher in mortgage rates.

Keep in mind that the economic data warrants much higher yields than 1.94%. COVID-19 is still hindering some of our sectors from really taking off. The vaccination process is going much faster now and disaster relief is hitting bank accounts. We are overdue for a stock market correction that could send yields lower. Also, bonds are short-term oversold so we can see a short-term rally in bonds and lower mortgage rates. However, the bond market is screaming from the top of the highest mountain, the Great American Bears of COVID-19 failed like all the American bears before them since 1790.

Fascinating. 2020 I couldn’t find a single general contractor to get two homes dialed in. Returned to Havasu. 🤞🏼it goes well “2021” in the Magic Valley.🛎