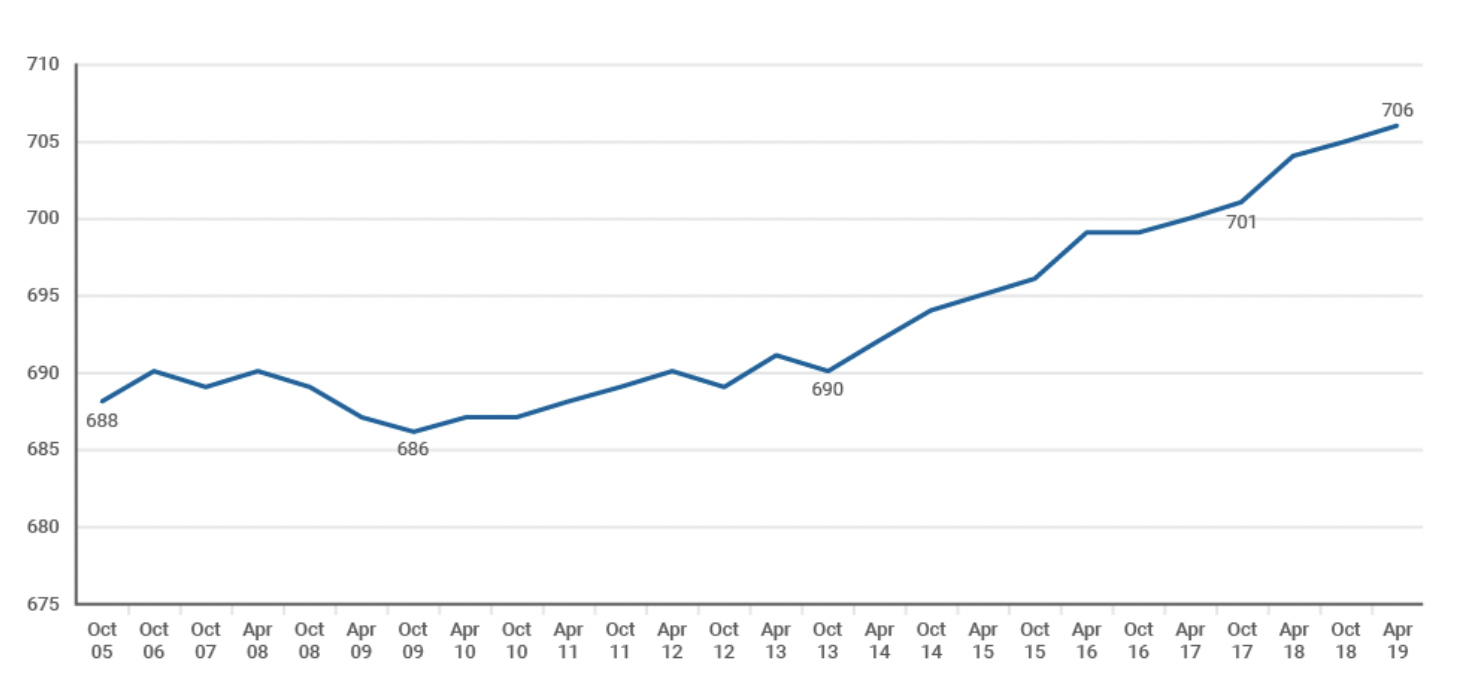

The average FICO score stands at 706, a record high, said Ethan Dornhelm, vice president of scores and predictive analytics at FICO. That compares with 686 at the 2009 end of the Great Recession and it eclipses the 690 at the 2006 height of the housing bubble.

The key drivers are U.S. economic expansion that has propelled job growth and an increase in consumer education about protecting and improving scores, Dornhelm said in a blog post. In addition, the passage of time is helping to remove the credit scars from events that happened during the financial crisis, he said.

“Consumers who suffered financial misfortune during the Great Recession have over the past few years had the associated missed payments from that time period purged from their credit file, in accordance with the Fair Credit Reporting Act,” he said.

Measuring different credit events, the biggest improvement between April 2009 and April 2019 was the timeliness of mortgage payments, Dornhelm said. A decade ago, 7.2% of the population had been 90 days or more late on a mortgage payment within the last two years. By April, it had dropped to 2.8%.

Also showing big improvement was the percentage of the population who had been 90 days or more past due on a credit card in the last two years. A decade ago, it was 13%, and in April it was 8.6%.

The jump in FICO scores was due to “score improvement, not score inflation,” Dornhelm said.

“Significant improvement in the overall population’s credit profile has been the key driver of the 20-point increase in national average FICO score over the past decade,” he said. “These improvements are reflective of improving consumer financial health, as would be expected during a period of economic expansion.”

Economic data signaling the chance of a looming recession has increased uncertainty in the credit-scoring realm, he said.

“The average FICO score will continue to change, but in what direction?” Dornhelm said. “Trade talks with China, the possibility of a `no-deal Brexit,’ and Fed interest rate decisions loom large as concerns of a recession persist.”

(Image courtesy of FICO)