Certain dynamics shaping the housing market have led the occasional forecaster to predict a boom in home equity lending.

As mortgage rates rise, some homeowners may be reluctant to relocate and forfeit their current low rate, providing a solid incentive to stay put to renovate their nest instead.

Plus, home prices are appreciating, totaling an aggregate $5.9 trillion in equity for American homeowners to tap, according to recent data from Black Knight.

So does this mean 2019 will see a boost in home equity lending? HousingWire asked three economists to weigh in, and the feelings were mixed.

Mark Fleming, chief economist at First American, said he does predict an uptick in home equity lending in the year ahead.

“The best way to access that home equity without losing the low rate on your primary mortgage is with a home equity loan,” Fleming said. “Rising rates create the incentive to take out home equity loans, because one can keep the low rate on their primary mortgage.”

Frank Nothaft, chief economist at CoreLogic, agreed, pointing out that homeowners are living in their homes longer than they did a decade ago, amassing considerable equity in that time.

“Compared to 10 years ago, the typical homeowner has owned their home four years longer.” Nothaft pointed out. “Since the trough in home prices in 2011, the CoreLogic Home Price Index was up 58% for the U.S. through October, building home-equity wealth.”

The desire to stay put has fueled ambitions to renovate, Nothaft added.

“To finance these alterations, they often choose a cash-out refinance of their first lien or opt to take out a second-lien home equity loan. Thus, we expect an increase in home improvement home equity lending in 2019,” he said.

But Aaron Terrazas, senior economist at Zillow, disagreed.

“We expect home equity lending will be flat in 2019,” he said, pointing to the fact that homeowners have been disinclined to tap it in the past.

“Over the course of this economic recovery, American consumers have been more reluctant than in the past to tap home equity for consumer spending,” Terrazas said. “I don’t expect that trend will meaningfully shift in 2019.”

Terrazas acknowledged that homeowners have turned to equity to finance renovations in recent years as for-sale inventory has been scarce, but he suspects that might shift in the year ahead.

“With inventory now increasing, there may be less of an imperative to renovate as opposed to buying.”

Nothaft said that recent tax laws will likely impact homeowners’ decisions to borrow as it restricts interest deducibility to home equity lending.

“Today, mortgage interest on a second lien is deductible only if the proceeds are used for home improvement purposes and the sum of the first and second loans is no greater than $750,000,” he noted.

This likely means that most home equity loans will be used for home improvement purposes, Nothaft said, rather than to consolidate debt or pay for education – other popular uses for home equity.

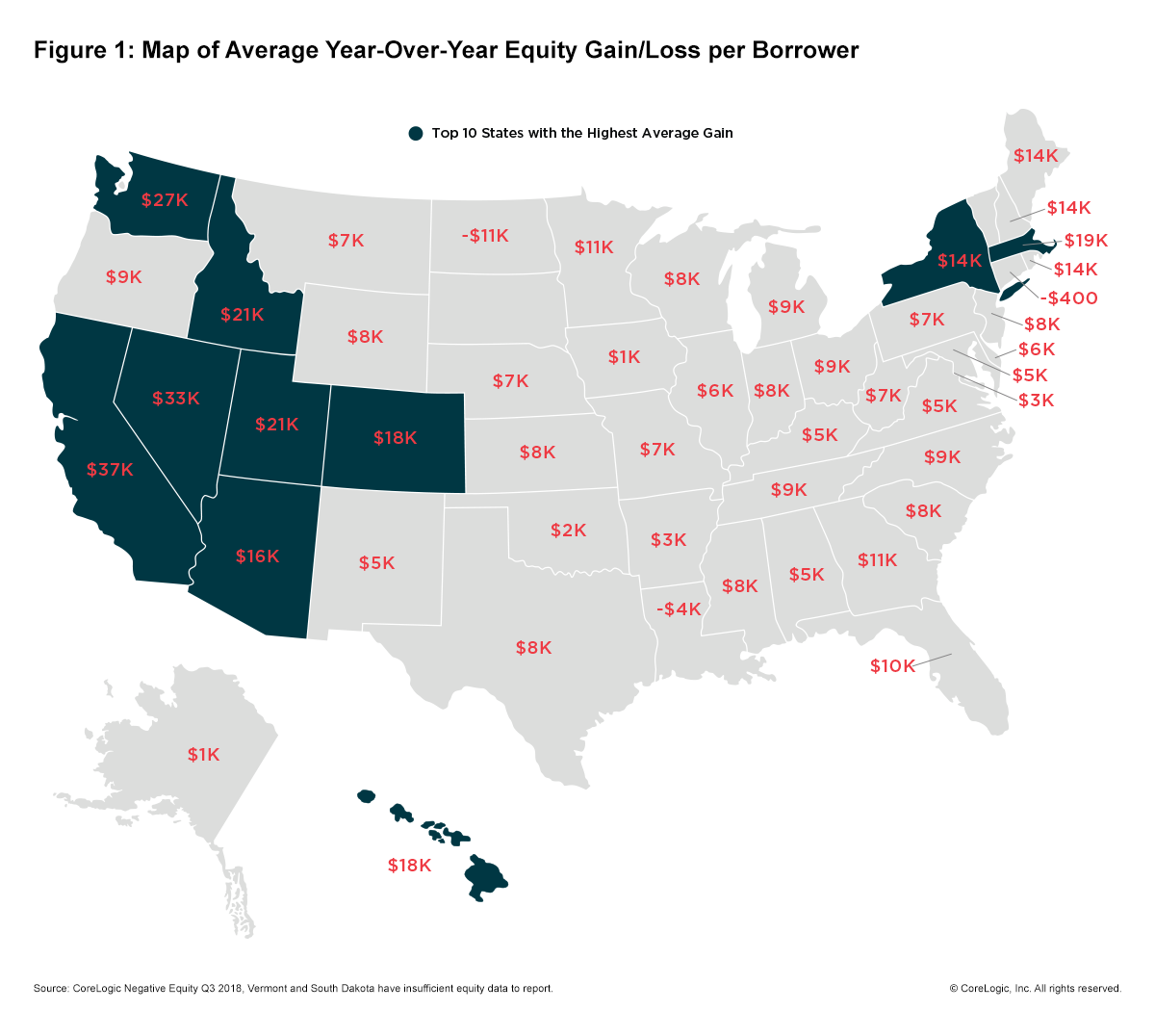

Nothaft also pointed out that equity growth has been uneven nationwide, meaning that home equity lending is most likely to occur in areas that have the greatest equity gains, like California and Nevada, which gained more than $30,000 in home equity in the past year.

While Fleming is bullish on home equity lending in the year ahead, he warns that fears of a looming recession could dampen activity.

“The risk of a recession, this year or in the years ahead, may cause homeowners to think twice about extracting equity,” Fleming said.

Terrazas said an economic downturn would make it harder for homeowners to access this source of wealth, even if they wanted to.

“The most obvious risk to home equity is lending standards,” he said. “If financial markets take a tumble in 2019 – or if lenders fear that the housing market is poised for a downturn – that could prompt lenders to tighten their standards for home equity lending.”

{kind=link}