WinWater Home Mortgage is set to launch its second jumbo residential mortgage-backed securitization. The company, which refers to itself as “a residential mortgage conduit aggregator focused on opportunities in the non-agency jumbo sector,” is bringing WinWater Mortgage Loan Trust 2014-2 to market.

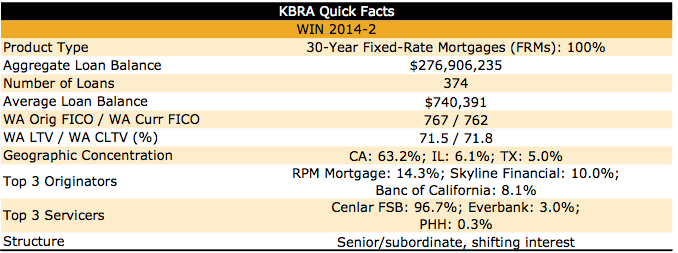

The securitization’s aggregate loan balance is $276,906,235 and it consists of a pool of 374 loans. The average loan balance is $740,391 with an average original FICO score of 767 and an average loan-to-value ratio of 71.5%.

WIN 2014-2 is WinWater’s second jumbo RMBS. Its first jumbo RMBS, WIN 2014-1, launched in June and carried an aggregate loan balance of $249,465,638.

All of the underlying mortgagees in the WIN 2014-2 mortgage pool are 30-year, fixed-rate mortgages.

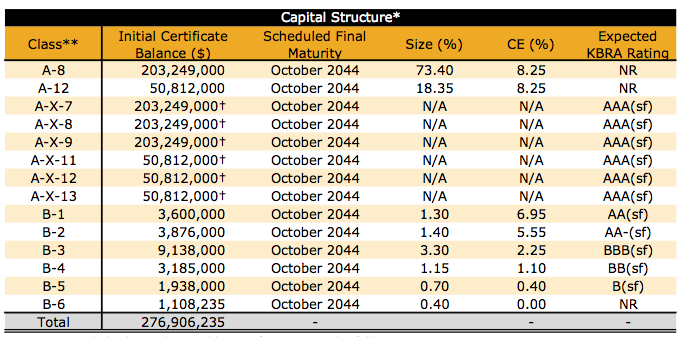

Kroll Bond Ratings Agency has released its presale report on the offering and awarded AAA ratings to the largest tranche of the deal.

Click the image below to see a breakdown of Kroll’s presale ratings.

In its presale report, Kroll noted the high quality of the collateral as a positive. “The WIN 2014-2 collateral pool consists of high quality, prime mortgage loans that exhibit significant borrower equity,” Kroll said in its presale.

“It should be noted, however, that the weighted average LTV and collateralized LTV ratios for this transaction are among the highest for any of the post-crisis, prime jumbo RMBS transactions that Kroll Bond Rating Agency has rated.”

Click the image below for a breakdown of the deal’s features.

Kroll also recognized the high credit ratings of the underlying borrowers as a positive of the deal. “Despite the fact that borrower incomes are relatively high, most loans bear prudent debt-to-income ratios, with a weighted average DTI of 32.6%,” Kroll said. “Additionally, income and assets for all borrowers have been well-documented and verified.”

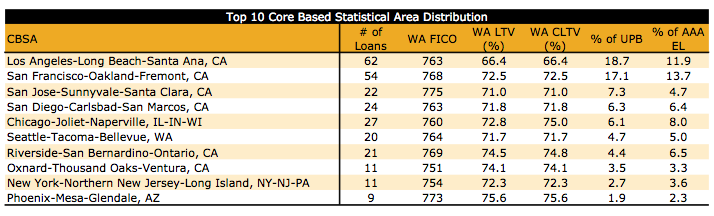

As with most jumbo securitizations, the majority of the loans are located in California, given the state’s high cost of living. “Non-conforming prime mortgages are most frequently originated in those regions of the country where home prices are highest,” Kroll said.

“As a result, the geographic concentration in pools of jumbo loans tends to be high, with significant exposure to assets located in California as well as a number of other major metropolitan areas.”

According to Kroll’s report, 63.2% of the underlying loans are located in California, with Los Angeles (18.7%), San Francisco (17.1%) and San Jose (7.3%) making up the three largest metro areas in the deal.

Click the image below for a geographic breakdown of the deal.

“To account for the risk associated with geographic concentration, the expected loss levels were adjusted upward based on KBRA’s methodology,” Kroll said. “This resulted in an increase of 1.2% at the ‘AAA’ level, a change of 23.3% over the base level.”

Kroll cautions on WinWater’s inexperience as a mortgage loan aggregator, given that the company was founded in 2013, and its lack of a track record with securitizations as concerns of the deal.

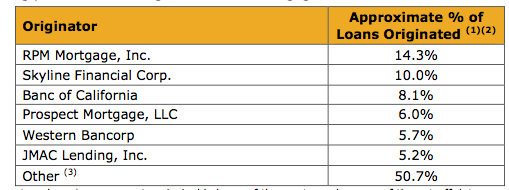

Kroll also cites the deal’s multiple loan originators with limited performance history as a concern.

"While originator diversity is common and may help reduce geographic concentration, it also increases exposure to the underwriting standards and processes of originators with limited jumbo mortgage loan performance history,” Kroll said.

“Differences in loan origination processes, or in the operations and infrastructure among loan originators, may cause divergent performance outcomes in RMBS pools that otherwise have similar loan characteristics. In addition, some of the originators may lack sufficient financial resources to fulfill their repurchase obligations if there was a breach of a loan-level representation and warranty.”

Click the image below to see the loan originators of the deal.