Mortgage rates have been slowly dropping recently, which has caught some people off guard. With inflation data that is still higher than the Federal Reserve‘s target, the recent decrease has left many intrigued. Was it the recent inflation reports or the last batch of labor data that played a significant role in this shift? The Fed’s recent hawkish stance, refraining from rate cuts and advocating for extended higher rate language, adds to the mystery.

My stance has remained unchanged since 2022: the Fed won’t pivot until they see the labor market break. However, the bond market will get ahead of the Fed if they believe the economy is weakening. The 10-year yield has fallen from its recent high of 4.72% on April 25 to a low this morning of 4.36% and mortgage spreads have been improving too. So, was this last move about inflation data or labor?

Today, the CPI inflation data missed estimates slightly, meaning it is just a bit cooler than what people were looking for, so bond yields went down right after the report.

Below: U.S. core CPI inflation inflation, running at 3.6% year over year

From BLS:The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.3 percent in April on a seasonally adjusted basis, after rising 0.4 percent in March, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 3.4 percent before seasonal adjustment.

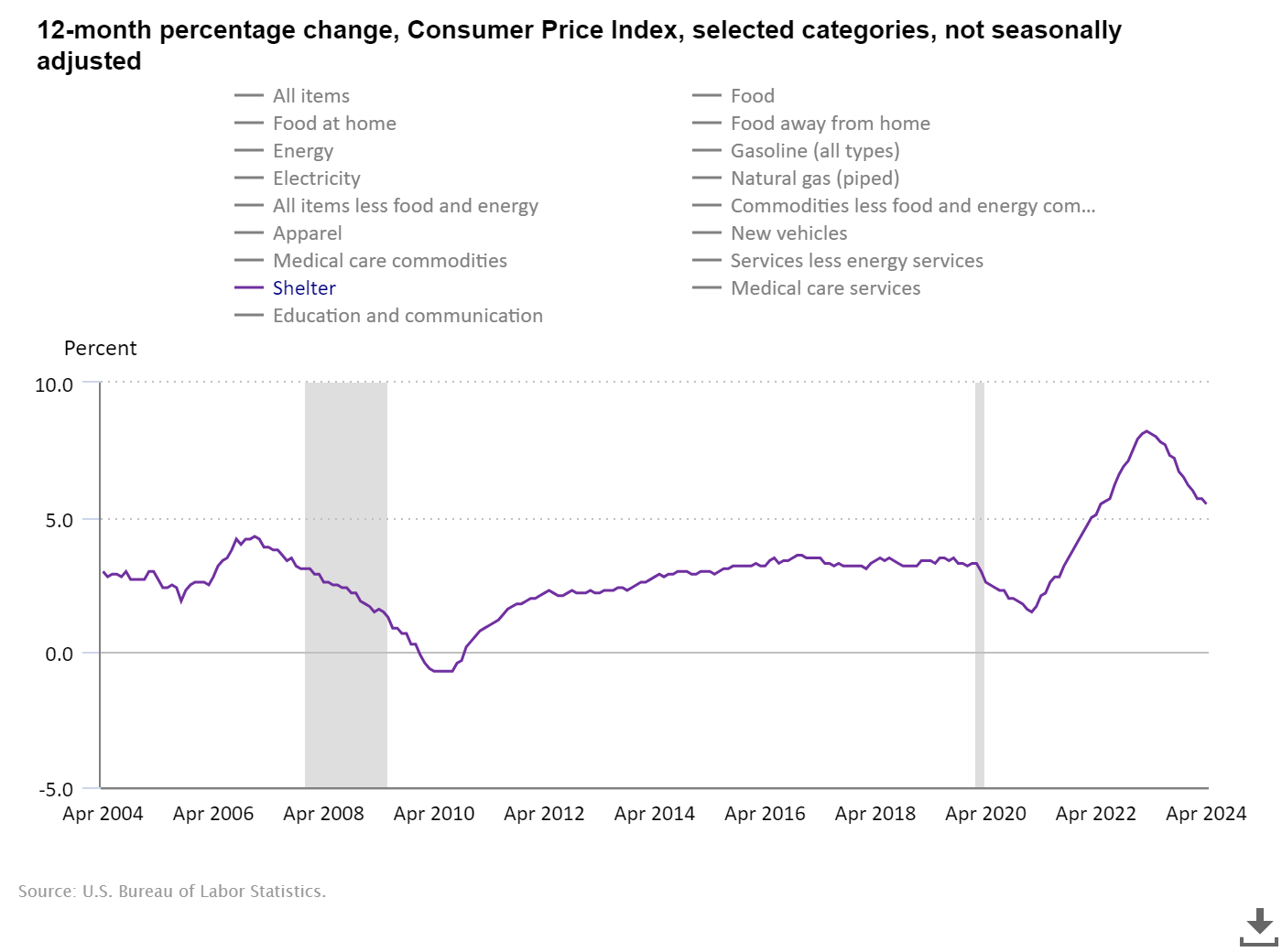

Since shelter inflation is the most significant component of CPI, it matters that this data line goes lower. With housing inflation taking off, we can only have 1970s-style inflation if we have a massive supply shock in other areas.

The Owner’s Equivalence of Rent has caused a lot of chaos this year for Fed members, who were all anticipating this metric would go lower faster. It’s moving in the right direction, but not fast enough.

So why have bond yields gone lower recently: is it the labor data?

Below: One month of data on the 10-year yield, currently at 4.34%

The labor market has been getting softer for some time, but it hasn’t broken yet. With the growth rate of inflation well off the peak growth rate of inflation, the Fed has turned more into a dual-mandate Fed. This means we are in a cat-and-mouse game with the bond market and mortgage rates that have valued labor data over inflation for some time now. I discussed the total labor data to explain why the Fed has become a dual mandate again in this recent HousingWire Daily podcast.

The bond market has headed lower twice since 2022, assuming the economic data was getting weaker, and short-term bond yields have gone lower three times since 2022, assuming more rate cuts are in play. Bond yields have headed back every time because the economy wasn’t breaking. However, if the labor data gets softer, the recent lower yield move makes sense. Once the labor market breaks, the 10-year yield and mortgage rates will go lower, but so far, it’s only getting softer, not breaking.

We have made good progress on the growth rate of inflation since the peak of the data. CPI inflation was running at 9% in 2022 and is at 3.4% today, roughly in line with the average growth rate of CPI inflation since 1914. However, bond yields and mortgage rates are higher today than in some periods with hotter inflation data.

I understand this can be confusing, especially last year when mortgage rates reached 8%. However, if you consider part of the focus was on the economy and the labor markets, then some of the mortgage moves lower and higher make more sense. Remember, for now, labor data is more important to the rate story than inflation.