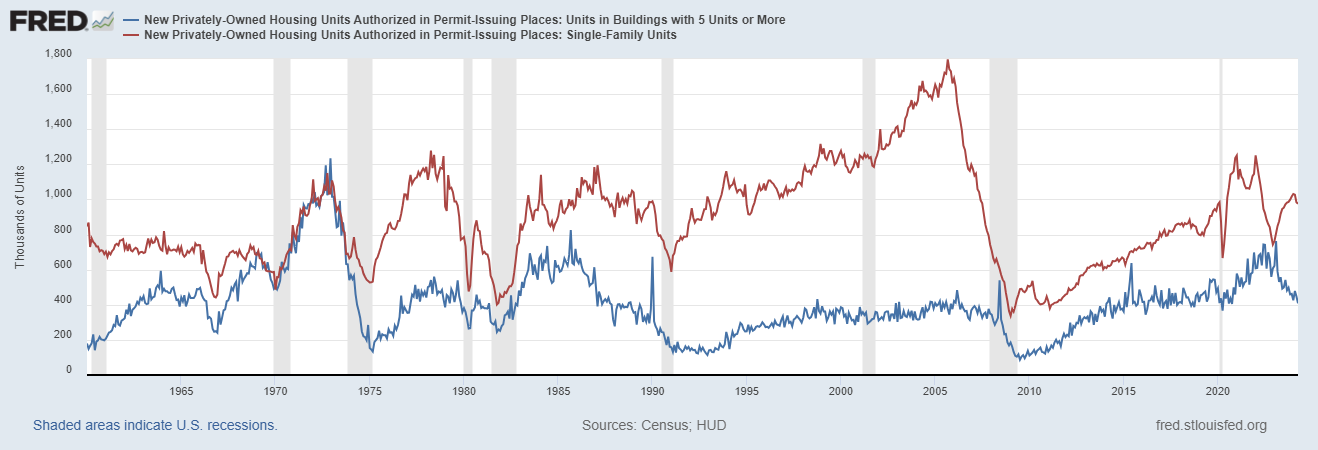

New home sales missed estimates, showing that demand isn’t crashing but not growing much either. However, we need to keep an eye on the housing construction data in this report because it has huge implications for the economic cycle, our recession risk and mortgage rates. As the chart below shows, the housing sector generally poses a future risk to labor if the single-family permits data continues to decline.

When single-family permit demand collapsed in 2022, we still had a healthy backlog of homes that needed to be finished. While that was happening, we also had 5-unit permits expand as well. Well, that isn’t the case anymore, as 5-unit permits are already at COVID-19 recession lows and now we have seen some softness in single-family permits.

The future production of housing units at risk

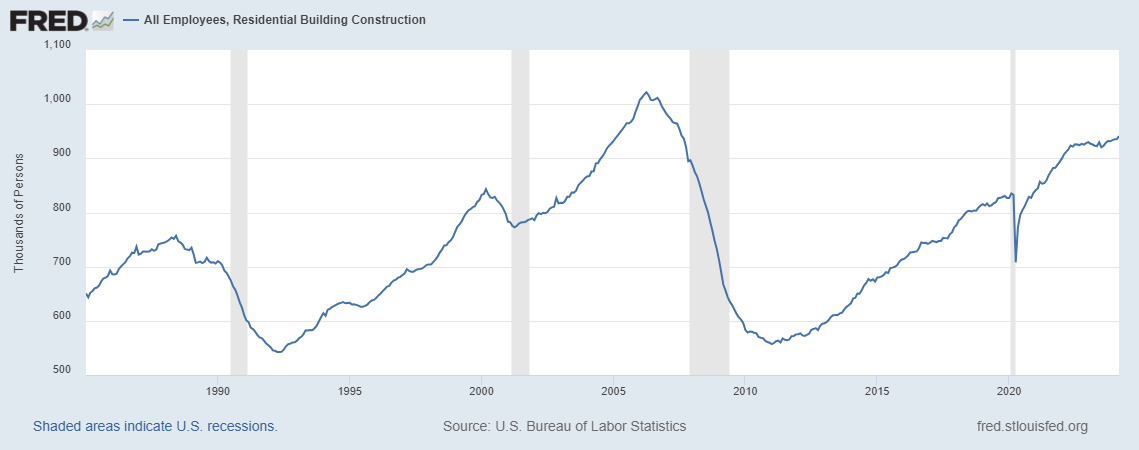

I am bringing this up because economic recessions tend to see residential construction workers lose their jobs first. After all, higher mortgage rates tend to impact housing faster than other sectors. Manufacturing jobs and business investment also tend to get hit with higher rates, but we have massive manufacturing spending now that hides that issue. As you can see in the chart below, residential construction workers aren’t losing their jobs yet.

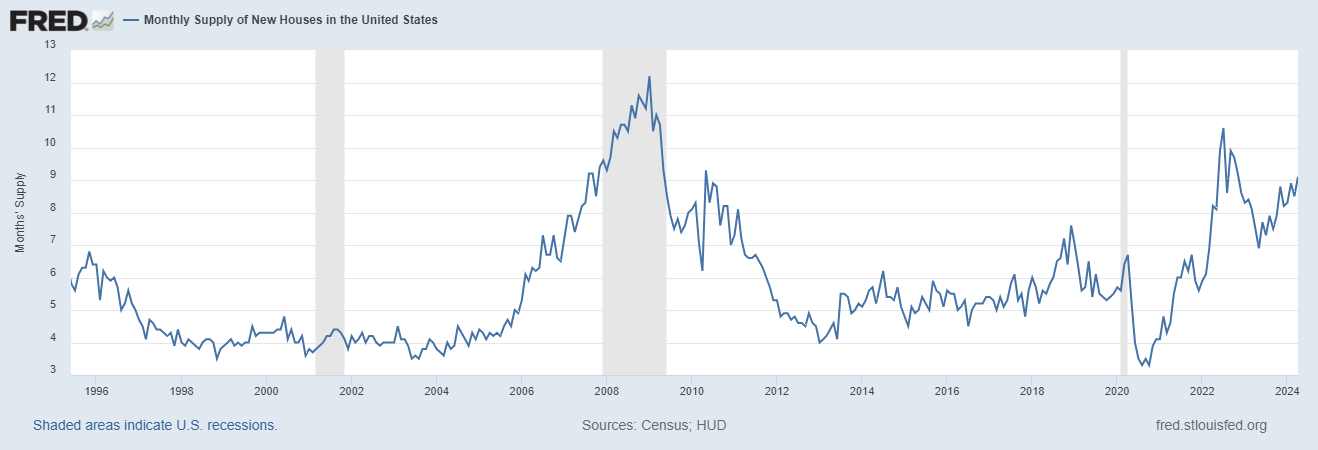

When it comes to the monthly supply of new homes, if the single-family permits and 5-unit permits fall together, construction labor is at risk once the backlog of new homes is completed. So, let’s look at the builders’ monthly supply data.

From Census: For Sale Inventory and Months’ Supply: The seasonally adjusted estimate of new houses for sale at the end of April was 480,000. This represents a supply of 9.1 months at the current sales rate.

While the monthly supply data seems massive, it’s a bit misleading regarding total units available for sale. Today, even with 9.1 months of supply, we only have 98,000 completed new homes for sale. This sector traditionally doesn’t release units completed for sale all at once, as it goes against the business model. Even during the housing bubble crash, the monthly supply data never got to 200,000 homes.

To give you some perspective, this amounts to less than two weeks of new listings of existing homes that come on the market.

I like to break down the monthly supply data into subcategories. People sometimes believe that the monthly supply of new homes means active, completed homes ready to buy, but that isn’t the case. In this report:

- 1.9 months of the supply are homes completed and ready for sale — about 98,000 homes.

- 5.3 months of the supply are homes that are still under construction — about 281,000 homes

- 1.9 months of the supply are homes that haven’t been started yet — about 101,000 homes

Now, the 1.9 months of supply of homes at 98,000 is roughly the line in the sand for the builders to start getting cautious about starting on homes that haven’t even dug dirt yet. This is why the rest of the year will be critical: as the builders begin to close on the construction of homes that are under construction, they will be less inclined to issue more permits.

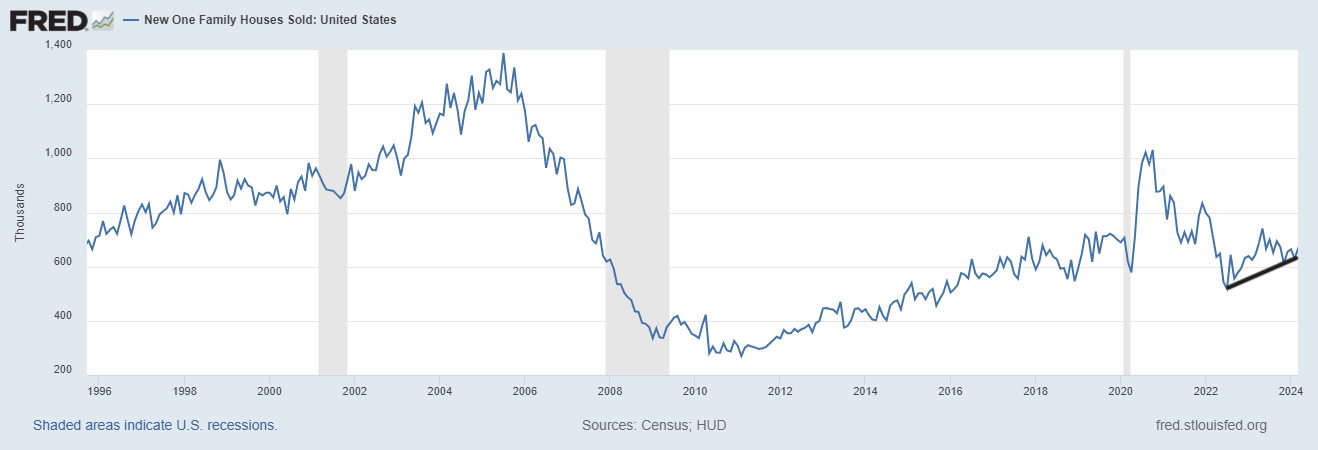

New home sales

From Census: Sales of new single-family houses in April 2024 were at a seasonally adjusted annual rate of 634,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 4.7 percent (±12.0 percent)* below the revised March rate of 665,000 and is 7.7 percent (±13.2 percent)* below the April 2023 estimate of 687,000.

As we see below, new home sales aren’t booming; they’ve been in a slow grind from the lows of 2022. Higher mortgage rates impacted sales growth toward the end of 2023 so only the big builders could work this out with the rate buy down. The question is, how much longer can they do this? With their profit margin capacity, as long as mortgage rates are below 7.25%, they can make some deals to close some homes. However, as we see in the chart below, new home sales haven’t gone anywhere for a while.

The smaller builders don’t have this buy down advantage, and thus, we have seen a decline in homebuilder confidence data. This is why we need to keep a close eye on the housing starts and new home sales data together. For the first time, permits are falling for both data lines, single-family and 5-units, a staple of every pre-recession cycle data run.

We care about construction workers because the Federal Reserve won’t pivot on rates until they see the labor market break, and the bond market will drive mortgage rates lower once they see that construction workers are really losing their jobs. Twice now, the bond market has tried to get ahead of recession data lines, only to have yields and rates go back up when the recession didn’t happen. This is why tracking housing construction data is critical to each economic cycle when considering mortgage rates and possible better future demand for our current housing market.