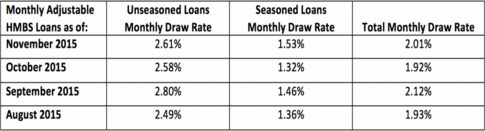

Monthly adjustable Home Equity Conversion Mortgages (HECMs) showed a a steady draw rate of 2.01% in November, up slightly from October, yet consistent with previous months’ rates, according to the latest New View Advisors commentary on Ginnie Mae data.

November’s 2.01% total monthly draw rate is for monthly adjustable HECM mortgage-backed securities, as noted by the third release of New View Advisors’ Reverse Mortgage Draw Index the company introduced in October.

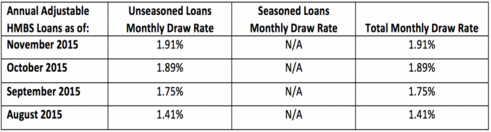

Data also show that Annual Adjustable draw rates for HMBS loans were 1.91% in November, compared to 1.89% in October, which is consistent with and converging to Monthly Adjustable Home Equity Conversion Mortgage (HECM) draw rates, according to New View Advisors’ second installment of its Annual Adjustable Draw Index, which launched earlier this month.

The index value is expressed as a monthly draw rate, equal to the amount of Line of Credit draws taken in any given month, divided by the total Line of credit amount available at the beginning of that month. The index only applies to loans with a Line of Credit feature and does not include fixed monthly Term or Tenure payments.

New View Advisors defines “unseasoned loans” as loans originated no more than two years ago, and “seasoned loans” as loans originated more than two years ago.

“We estimate that existing HECM loans securitzed into HMBS are generating about $205 million in ‘Tails,’ consisting of approximately $96 million in line of credit draws each month in the monthly adjustable segment, $31 million in the annual adjustable product segment, $53 million per month in Mortgage Insurance Premium advances, $10 million in Term/Tenure Draws, and $15 million in excess spread,” writes New View Advisors in its commentary.

The excess spread, or “Servicing Fee Margin,” represents the excess of the HECM loan interest rate over the HMBS interest or “Participation” rate, generally, 0.36% per annum, New View Advisors notes. Meanwhile, the issuer’s net excess is 0.30%, as Ginnie Mae’s HMBS insurance fee is six basis points.

“Because these new Tail issuances generally sell at a premium, HMBS Tails are a crucial component of industry profitability,” writes New View Advisors.

Read the New View Advisors commentary.

Written by Jason Oliva