The Federal Housing Finance Agency announced the results of the stress tests for Fannie Mae and Freddie Mac on Tuesday.

In December, the FHFA announced each of the government-sponsored enterprises would be allowed to hold $3 billion in capital. While this is up from the previous amount of zero, it comes as no surprise with such low capital amounts, that both GSEs failed this year’s stress tests.

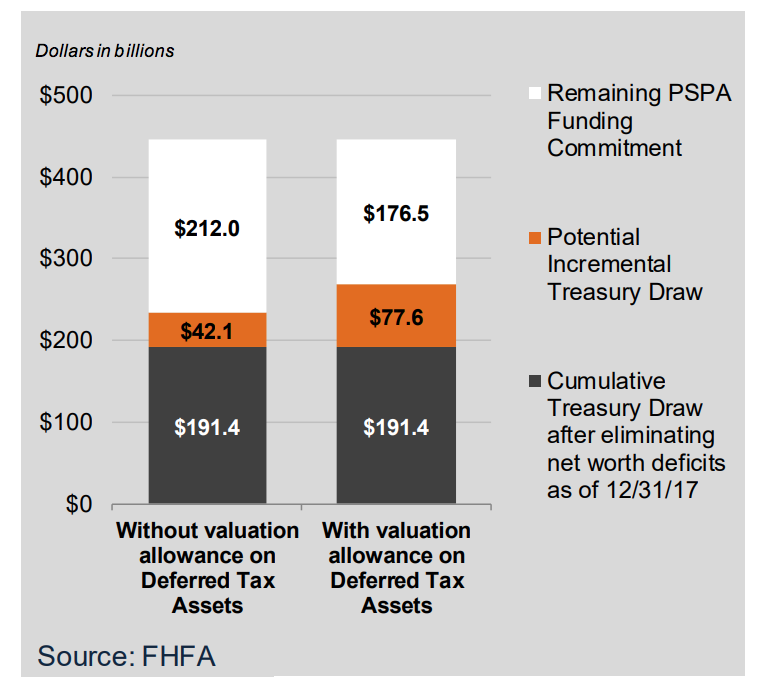

This year’s stress tests show the GSEs would need to draw a combined total of between $42.1 billion and $77.6 billion, depending on the treatment of deferred tax assets, from the U.S. Department of the Treasury.

And while the GSEs would still need a draw, the amount is improved from last year, when they would have needed nearly $100 billion in the case of economic adversity.

The 2018 DFAST Severely Adverse scenario is based upon a severe global recession which is accompanied by a global aversion to long-term fixed income assets.

In prior years, the enterprises applied a standard effective tax rate of 35%, consistent with the prevailing corporate tax rate. For the 2018 DFAST reporting cycle the standard effective tax rate was lowered to 21%, consistent with the current corporate tax rate under the Tax Cuts and Jobs Act signed into law on December 22, 2017.

After the estimated draws the GSEs would need to take out under the stress tests, the remaining funding commitment under the Senior Preferred Stock Purchase Agreements would be $212 billion without establishing valuation allowances on deferred tax assets, or $176.5 billion if both Enterprises established valuation allowances on deferred tax assets, as the chart below shows.

Click to Enlarge

(Source: FHFA)

Important contributors to losses in the Severely Adverse Scenario included the following:

- The provision for credit losses was the largest contributor to comprehensive losses at both enterprises.

- The second largest contributor to comprehensive losses at both enterprises was the global market shock impact on trading securities and available-for-sale securities.

- Comprehensive losses increased in the 2018 DFAST reporting cycle compared to the 2017 DFAST reporting cycle, mostly driven by the increase in provision for credit losses as a result of the more severe decline in home prices included in the 2018 DFAST Severely Adverse scenario.