While the housing market is on the mend — with progress even in the hardest-hit states — the backlog of homes in foreclosure and real-estate owned properties is still clogging the pipeline, analysts claim.

The East Coast is a testament to such findings, where the duration of the foreclosure process is high in large part to judicial foreclosure procedures in states using that process, according to the Federal Reserve Bank of New York’s latest report.

The volume of distressed properties continues to impact housing momentum, and consequently, there is a compelling need for improved public policy on the local and national levels to minimize losses and externalities resulting from foreclosures and REO inventory, explained Diego Aragon, Richard Peach and Joseph Tracy of the NY Fed.

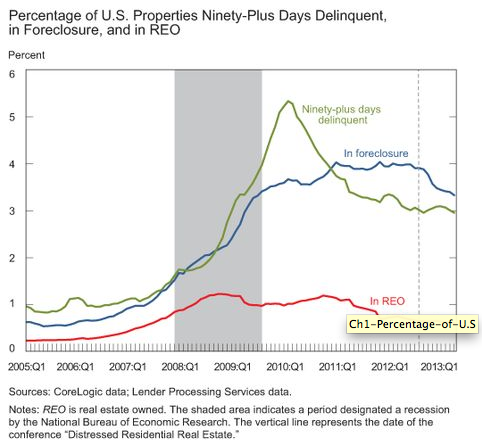

As of March 2013, nearly 3% of all first-lien loans secured by one-to-four-unit residential properties were 90-plus days delinquent, essentially unchanged from the June 2012.

In contrast, the percentage of loans in foreclosure, which leveled off around 4% from 2011 through 2012, declined to 3.5% by early 2013, the report noted.

The decline in the percentage of loans in the foreclosure process was due to a sharp decrease in the number of loans flowing into foreclosure, such that for the past nine months more loans have moved out of foreclosure than moved in.

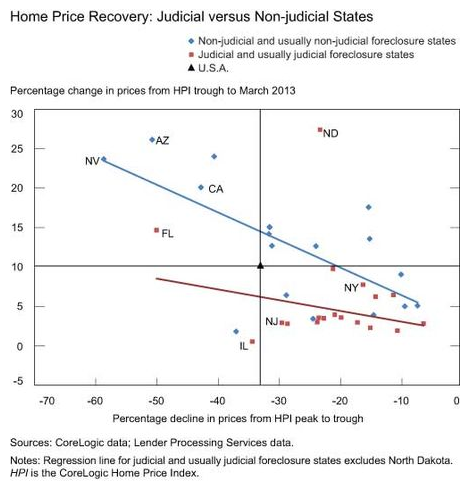

Underlying these national trends is a large disparity in performance between states that have a judicial foreclosure process and those that have a non-judicial foreclosure process.

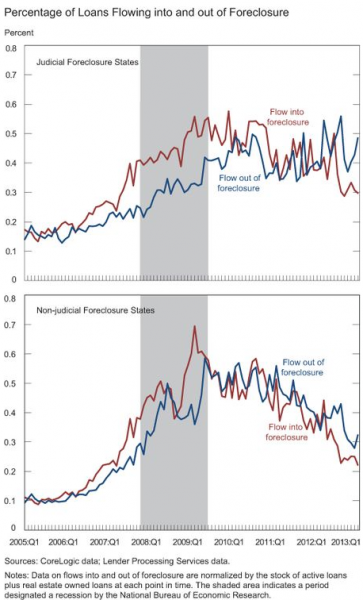

The average number of days that a mortgage is 90-plus days delinquent at the time the foreclosure process is started is roughly comparable in judicial and non-judicial states.

"The key distinction is in the rate of flow out of foreclosure or, alternatively, the average number of days a loan/property remains in the foreclosure process," NY Fed analysts explained.

They added, "It is evident from these data that throughout the crisis, the flow in and flow out remained much closer in the non-judicial states than was the case in the judicial states. This explains why the judicial states continue to have a relatively high stock of loans/properties in foreclosure."

Judicial states maintained higher foreclosure rates in early 2013, indicating the length of a loan remains in the foreclosure process in the judicial states is significantly longer than in the non-judicial states.

For instance, Florida, New Jersey and New York stand out as the most extreme examples of this occurrence, the report stated.

As a result, the large volume of loans in the foreclosure process in the judicial states appears to be impeding a home price recovery in those states.

The judicial foreclosure states have seen a more modest improvement in home prices since the trough for a given peak-to-trough decline in home prices.

"One potential explanation for this relationship is that potential homebuyers in the judicial states recognize that a large number of distressed sales have yet to occur, and this consideration has influenced the prices they are willing to offer for homes currently on the market," the NY Fed analysts concluded.