Lender and GSE responses to the “lender choice” credit score selection policy announced last year are likely to have significant impacts on the allocation of mortgage credit among credit investors. As analyzed in several studies, including my own, absent a response by the GSEs, there is the potential for adverse selection to raise credit risk for the two housing agencies as lenders rationally select the highest credit score (either FICO® or VantageScore® 4.0) to send to Fannie Mae or Freddie Mac.

The GSEs’ likely response would be to raise loan-level price adjustments (LLPAs) in an effort to mitigate potential adverse selection. We’ve seen this movie before when the GSEs raised LLPAs on investor properties and second homes, with private investors absorbing a large share of these loans. A new best execution pricing analysis suggests a similar fate awaits the GSEs should they raise LLPAs to levels consistent with actuarial pricing of credit risk.

The mechanics of best execution analysis

In maximizing value, a lender will conduct a best execution analysis of all revenue and cost components associated with originating and servicing a mortgage for different dispositions of the loan. In addition to GSE execution, a loan could be sold into a Ginnie Mae securitization, a private label securitization (PLS), or, if the lender is a depository, a portfolio disposition. Finding the all-in highest price among alternatives winds up being the best execution. In the case of GSE-eligible loans, a key driver is the LLPA assigned to the loan by the GSE. Therein lies the link between lender choice and credit allocation.

A recent study by Milliman estimated that LLPAs across credit scores would need to increase from current levels in order to compensate the GSEs for the potential incremental credit risk from adverse selection. While the increase in estimated LLPAs is not as large as the increases in LLPAs made by the GSEs for investor properties or second-home loans, where GSE purchases of those loans fell by 20%, it could nonetheless be material. A key question is, if we were to assume the GSEs raised LLPAs consistent with the Milliman analysis, what impact would it have on credit allocation and risk?

Scenario analysis: Projecting credit shifts

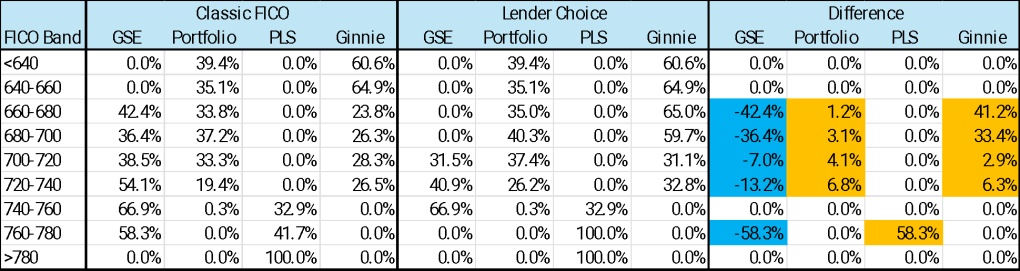

To analyze this, I used a sample of 200,000 recent GSE loans in an industry-standard best execution pricing analysis under multiple scenarios. One scenario examined best execution pricing for a depository where the possible dispositions included a GSE, Ginnie and private-label securities (PLS) securitization as well as portfolio retention. An independent mortgage banker (IMB) best execution was also performed without the portfolio retention option. The analysis was conducted across credit score buckets used in LLPA grids currently under a Classic FICO (current state) and lender choice (future state) scenario.

A summary of the depository results is shown in Table 1 below.

Table 1: Classic FICO® vs lender choice best ex depository disposition

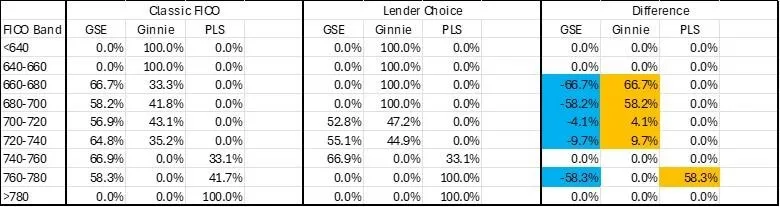

Between the Classic FICO and lender choice scenarios, the GSEs would see a marked shift away from them toward FHA and, to a lesser extent, portfolio lenders in the 660 to 740 credit score range. PLS would wind up being the optimal takeout for credit scores above 760. This is generally consistent with industry expectations that lower credit quality loans are a more likely disposition for FHA and that private capital is a more likely outlet for the highest credit quality loans. Similar results hold for IMBs as shown in Table 2.

Table 2: IMB best execution – Classic FICO® vs lender choice

Market outcomes and the future of credit allocation

Another interesting result is that while the GSEs would experience a decline in volume in this analysis, their estimated loss rates would remain relatively the same, while FHA loss rates could increase by nearly 14% under the lender choice scenario from the baseline Classic FICO scenario. Given that FHA delinquency rates have been on an upward march recently, such an outcome would not bode well either for the Mutual Mortgage Insurance Fund or for mortgage servicers of these loans that would bear higher expenses.

So, what are the likely results and implications from lender choice on credit allocation?

- First, absent other influences, higher LLPAs to address lender choice risk would likely lead to a material reduction in the volume of loans sold to the GSEs. The analysis did not account for other non-pricing factors, such as policy and other operational differences between dispositions, which would tend to lessen the outflow implied by this pricing analysis. However, the analysis suggests that some decline in GSE volume is a reasonable expectation. It is also consistent with what occurred when the GSEs raised LLPAs on second homes and investor properties.

- Consistent with industry expectations, the analysis shows that the Ginnie Mae (FHA) disposition is a better execution for lower credit scores, and PLS is a better execution for the highest credit scores. Higher LLPAs would worsen the GSE execution, further widening the pricing gap between dispositions.

- Depositories would see some pickup in portfolio executions from higher LLPAs, and this would be more pronounced at lower target return levels. Additional increases in portfolio execution would occur if LTV-based risk weights for mortgages are adopted by bank regulatory agencies for determining capital requirements.

- As a result of the impact of higher LLPAs that would lower GSE best ex pricing, some reallocation of credit risk is likely, with FHA taking a greater allocation of that risk than other credit investors.

A primary takeaway from this analysis is that lender choice is likely to impose major effects on the allocation of loans and credit among credit investors, with a great deal of uncertainty in the process. While this analysis provides a structured way of understanding potential relative shifts in loan allocation and risk via an industry-standard best ex pricing framework, much more work is needed to assess the impacts of one of the biggest policy changes to mortgage underwriting in years.

Clifford Rossi is the Principal at Chesapeake Risk Advisors, LLC. Over a 25-year industry career spanning the S&L and 2008 financial crises, Dr. Rossi worked for both Fannie Mae, Freddie Mac as well as some of the largest banks in various C-level risk management positions.

This column does not necessarily reflect the opinion of HousingWire’s editorial department and its owners. To contact the editor responsible for this piece: [email protected].