In the game of housing crisis Rochambeau, we play with income, inventory, and policy. Inventory cannot beat inadequate incomes, but better compensation policies can.

The labor market has reached peak disengagement rates, partially driven by historic strikes, resignations, non-participation, and silent quitting. By splitting the workforce into five income groups to view homeownership rates, we lay bare a cause for retreat from an increasingly unfair labor market – a system with four times more losers than winners and the Top 1% jettisoned well beyond the reach of parity. As the architects of individual purchasing power (incomes), corporations must be a part of the solution to create affordable, long-lasting homeownership for everyone.

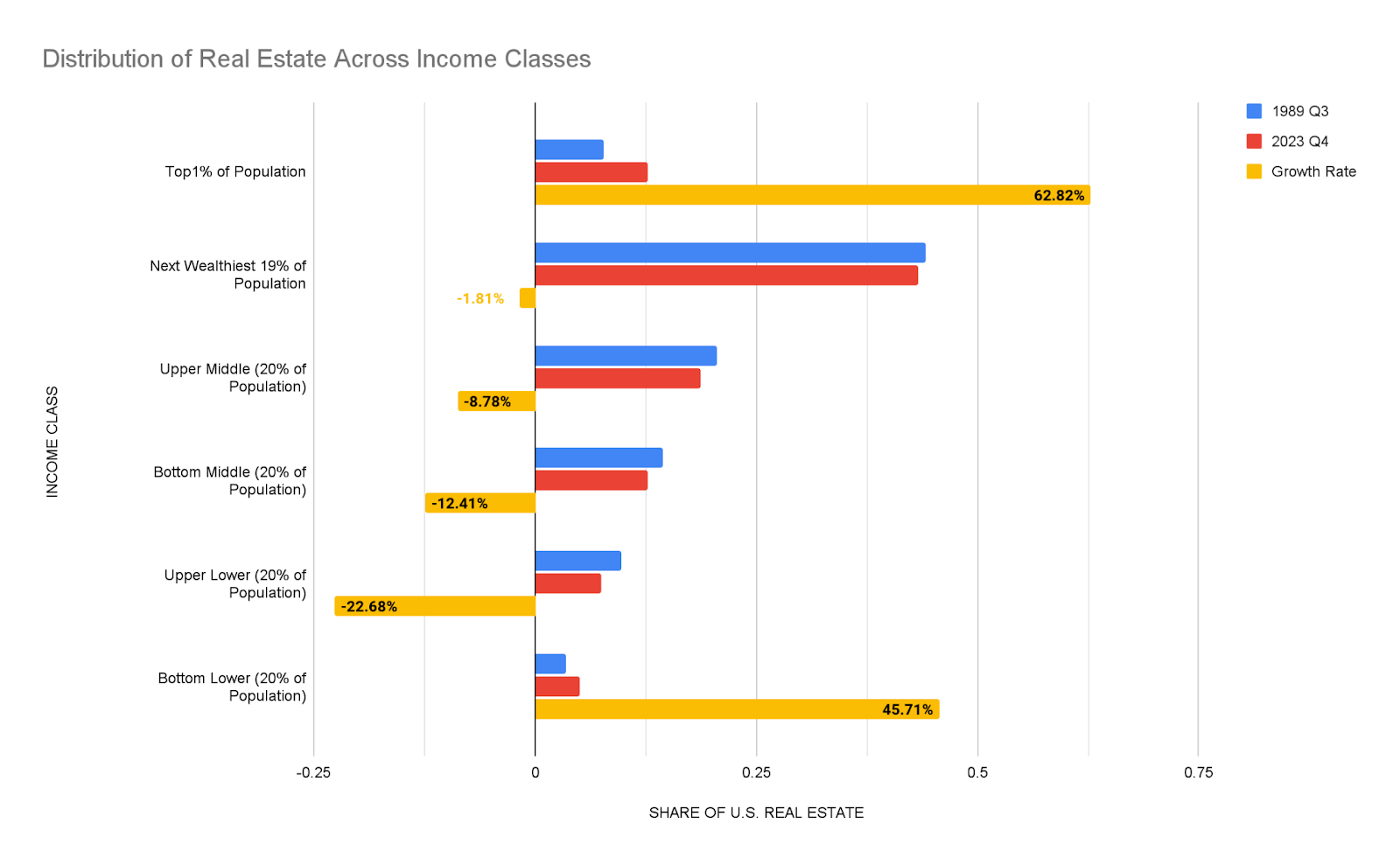

GRAPH 1: The distribution of real estate across the different income segments as a percent of the total real estate market in Q3 1989 and Q4 2023. Data Sources: Board of Governors of the Federal Reserve System

What got us here

In the late 1980s, someone at The Federal Reserve Board got curious about income-real estate relationships and started collecting data (Graph 1). For the past three decades, we watched the Top 1% of incomes increase their share of American property in the U.S. by more than 60% at the expense of middle and lower-income segments. Today

- The richest 1% own more than one in every 10 properties, despite representing only one in 100 Americans.

- The poorest 20% own only 5% of real estate, despite a significant 46% increase from public interventions.

- Those not living at either extreme suffered debilitating losses, with segments at risk of poverty hurt the most, losing almost a quarter of their share.

These dynamics played out where the Top 20% of incomes now hold more than one in every two properties, reducing the remaining 80% of Americans to blood sport over the balance. Drawing on these trends as guides, it becomes evident that new inventory would be impotent in the crisis, slipping into the same unyielding snare of income inequality.

Driving prices up

The striking difference in ownership highlights a winner-take-all system. If several families are interested in one house, the richest family will outbid the others, increasing the home’s value to reflect their untouchable income. The untouchable value becomes the epicenter of a ripple effect that also causes neighboring home prices to increase.

The gain in all property values, thus, mirrors the income growth rate of the wealthiest families. If other families’ salaries do not grow at the same rate, the rising property values will outpace their wages, creating a gap between families and nearby homes. The hole gets filled by institutional and wealthier buyers who rent the houses to losing families, or more affluent families will purchase the property to expand their home size. The gap does not result from wage inequality but rather from wage growth inequality.

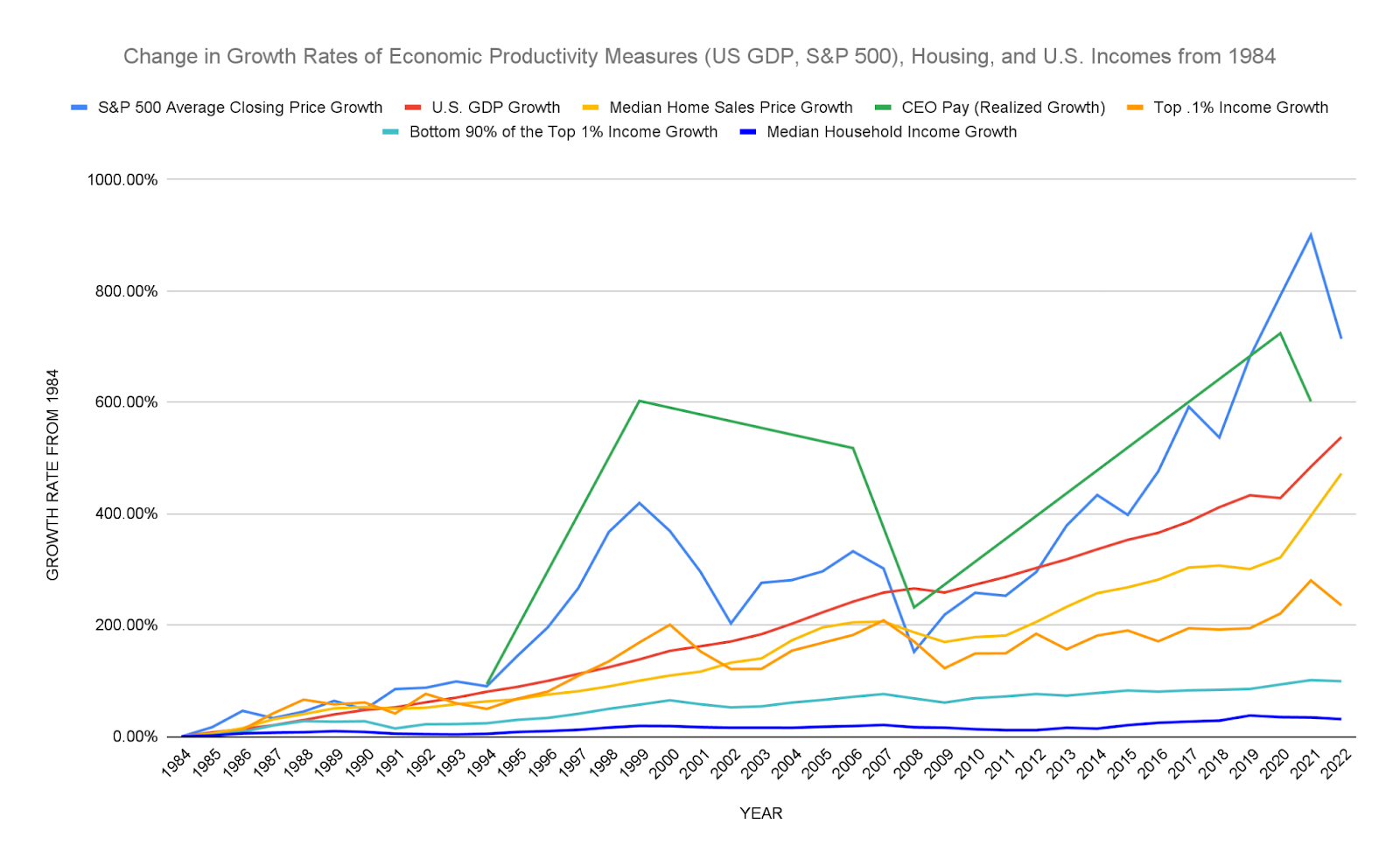

GRAPH 2: The growth rates of home prices, income segments (including CEO pay of the top 350 firms), and economic productivity measures (S&P 500 and US GDP). Data Sources: Adjusted for inflation. Economic Policy Institute 1 and 2, Multpl, The Federal Reserve Economic Data, U.S. Census Bureau, GoBankingRates. CEO Pay uses null values for years where data does not exist.

Executive pay scales feed income growth imbalances, but not because of cash salaries. Nearly all major corporation CEOs, key executives and boards get paid primarily in company stock – a dynamic, take-home slice of the S&P 500, whose growth frequently outperforms even the U.S. GDP (Graph 2). Regular employees receive their pay as fixed cash with fixed raises, and less than a quarter choose to exercise stock options. When they do, it is usually a tiny amount, taxed as income, with no variety in how to exercise them.

In 2010, less than half of eligible Netflix employees opted for stock as part of their compensation, taking a mere 5-7% of their earnings as stock. Employers grant key executives and boards over 60% of their compensation in stock, with CEOs taking the highest rate at about 80%. Netflix stock appreciated 37x in ten years; median salaries grew 1.2x.

By 2024, in addition to owning more than double their share of all real estate, the Top 20% of incomes held 87% of all corporate equities and mutual funds. The Top 1% took almost half of that, owning a whopping 38% of the whole market. Possessing almost the entire corporate equities market, rather than a small stake as a regular employee or retail investor, is the difference between owning a bank and owning a savings account. That difference in buying power flaunts itself in the housing market – leading to untouchable prices.

The housing-compensation loop whirls into a circus of disparities that hit superstar cities where companies like Netflix flourish. Superstars are metros piled high with people who generate ideas and make remarkable contributions to the country’s GDP, like San Jose and New York City. More than half of superstar residents are housing-burdened, meaning housing eats at least 30% of their income (1, 2, 3, 4, 5, and 6). Equity management firm Carta found that most employees do not exercise stock because of cost and financial risk. So, in a supremely ironic twist, the company’s stock is useless to ordinary employees because of the very housing crisis compensation practices created in the first place. The long-term logic of stock cannot beat the immediate crisis of rising housing costs and stagnant wages emptying American bank accounts. Offering stock options under these conditions is as offensive as nobility suggesting cake in a famine.

A government solution

Without employer participation and accountability, the government has taken on the full onus of fixing the housing crisis. But it lacks the resources to tame this behemoth, presenting Americans with affordable housing solutions that are well-intentioned but unsustainable or undesirable.

For example, the California Dream for All program provides first-time homebuyers with their entire downpayment in exchange for a percentage of passive ownership in the home. These “shared equity” agreements are an attractive proposition to first-time homebuyers unable to save under the burden of high rents, high student debt, and stalled wages. Unsurprisingly, California’s initial tranche of capital was committed before the program even started.

The Federal Housing Finance Agency recently launched its first round of shared equity programs through Fannie Mae and Freddie Mac. But they cap how much an investor-lender can benefit from increasing home value. The government simply cannot deliver on the high need or delicate balances, and behind closed doors, many officials are frustrated with employers’ unrelenting role in the crisis. Ultimately, employees cannot participate in remunerative capitalist risks, like buying stock options, until employers clean up their part of the housing crisis.

A way forward

Overhauling Employee-Assisted Housing Programs (EAHPs) is the easiest remedy. In these programs, employers provide cash to employees for down payments and closing costs. But today’s EAHPs treat these benefits as employee income – payroll expenditures, which are essentially company losses. This results in a relatively small benefit for the employee that gets taxed as income, and a few thousand bucks pale when a starter home costs anywhere from $500,000 to $1.4 million. Since EAHPs are expenses, employers are disincentivized to provide anything more to meet surging home prices.

Now that governments have opened shared equity pathways to down payments, they have cleared the way for finance startups to get employers around the payroll pitfall. Shared equity transforms the expenses into investments, so EAHPs become assets, not losses.

HomeFree, a national housing non-profit whose founders recently received the prestigious Joseph Wharton Award from The Wharton School, has drawn plans with Baltimore employers to pilot these startups and volley housing outcomes of participating companies’ employees. Their focus is to rehabilitate and repopulate Baltimore neighborhoods gutted by centuries of systemic racism and then destroyed and abandoned by the 2008 financial crisis.

The underlying framework of American property laws is feudalism – hierarchies, stagnating mobility, debts, and landlords, all observing real estate as the ultimate power. Today’s income and property distributions echo in that pit. Although employer shared equity is relatively new, it gives housing a way forward not seen since mortgages evolved a century ago. It is a strong opening move, foreshadowing policy changes that could deliver the winning Rochambeau play the housing market needs.

This column does not necessarily reflect the opinion of HousingWire’s editorial department and its owners.

To contact the editor responsible for this piece: [email protected]